Limited Partners (LP) vs General Partners (GP) in Private equity

Table Of Contents

Difference Between Limited Partners (LP) and General Partners (GP)

Limited Partners (LP) are the ones who have arranged and invested the capital for venture capital fund but are not really concerned about the daily maintenance of a venture capital fund whereas General Partners (GP) are investment professionals who are vested with the responsibility of making decisions with respect to the ventures that are required to be invested.

Many Institutions and High Networth Individuals have plenty of funds in hand on which they wish to earn higher expected returns. Traditional methods do not have the capacity to give them the expected return, so to earn a better return on their investments, they invest in private companies or public companies that have turned Private.

These investor doesn't do such kind of investments directly. They make this investment via a private equity fund.

Table of contents

- Difference Between Limited Partners (LP) and General Partners (GP)

- How does a Private Equity firm work?

- Who are Limited Partners or LP?

- Who are General Partner (GP)?

- How do General Partners or GP earn so much?

- What is the Hurdle Rate?

- What are Escrow and Claw-Back?

- Carry Structures from Around the World

How does a Private Equity firm work?

To understand the concept of Limited Partners (LP) & General partners (GP), it is necessary to know how the PE works.

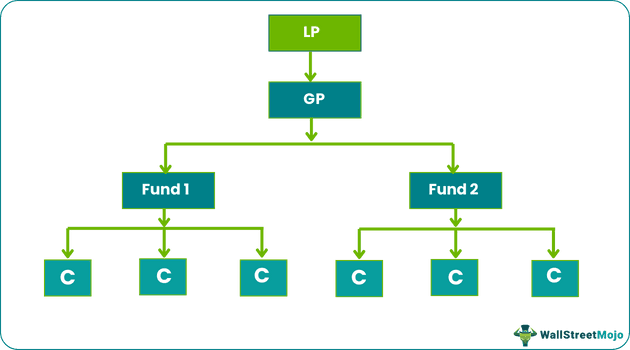

When a PE firm is established, it will have Investors who have invested their money. Each PE firm would have more than one fund.

E.g., Carlyle, which is a world-renowned PE firm, has several funds under management. These include Global Energy and Power, Asia Buyout, Europe Technology, Carlyle Power Partners, etc.

The life of a PE fund can be as long as ten years. Generally, in those ten years, 15-25 different types of investments are done by Private equity funds. In most cases, one particular investment won't exceed more than 10% of the total commitments of the fund.

The investors who have invested in the fund would be known as Limited Partners (LP), and the PE firm would be known as General Partner (GP). So basically, the structure of a PE firm looks like this.

Who are Limited Partners or LP?

The external investors in PE funds are known as limited partners (LP). It is so as their total liability is limited to the extent of capital invested

source: forentis.com

Not everyone can invest in a PE Firm. Generally, investors having an ability to put $250,000 or more are allowed to invest in PE Firm. Hence LP generally would have investors such as Pension Funds, Labor Unions, Insurance companies, Universities Endowments, large wealthy families or Individuals, Foundations, etc. Private vs. public pension funds, university endowments, and foundations account for 70% of the money in the top 100 private-equity firms while the remaining 30% is with HNWI, Insurance & bank Companies.

Does that mean that commoners cannot invest in funds at all? Well, things have started to change now. Traditional private equity managers, such as KKR, now offer opportunities to invest at a much lower amount than just $10,000.

Canada Pension Plan Investment Board, Teacher Retirement System of Texas, Washington state investment board, and Virginia Retirement Board are few examples of large investors (limited partners) worldwide who have invested in Private equity funds.

So LP would commit capital to a private equity firm and demands a return for it. Private equity has performed far better than the public markets in the past.

As per the available data, From April 1986 to December 2015, Cambridge Associates' US Private Equity Index gave its investors 13.4 percent annually net of fees, with a standard deviation of 9.4 percent. It was the longest period for which data is available currently, while the Russell 3000 Index returned 9.9 percent annually over the same period, with a standard deviation of 16.7 percent (including dividends).

source: Bloomberg.com

Limited Partners just invest their money; they aren't involved with fund management. The management is carried out by the General Partner.

Who are General Partner (GP)?

If a fund is created, then obliviously, you need a person to manage it. It is done by a General Partner (GP). All the decisions for the PE fund are made by GP. They are also in charge of managing the fund's portfolio, which will contain all of the fund's investments.

source: forentis.com

The General Partner is paid either by way of a management fee, or it can be by way of compensation. A management fee is nothing but a percentage of the total amount of the fund's capital. This percentage is fixed and not flexible. Generally, this fee range from 1% to 2% annually of the capital committed.

For example, if Assets under management are 100bn, then a 2% management fee would be $2bn. These fees are utilized for admin purposes and cover expenses such as salaries, deal fees paid to investment banks, consultants, travel exp, etc.

source: forentis.com

How do General Partners or GP earn so much?

A GP like Henry Kravis of KKR and Stephen Schwarzman of Blackstone has made a windfall half-billion dollars in a single year.

The answer is the returns distribution waterfall.

Apart from their salaries, General Partner also earns carried interest or carry. It is thus a % of the profits that fund gains on investments. For example, if a company is bought for $100bn and sold for $300 billion, the profit is $200 billion. Carried interest would be based on this $200 bn.

The other name used for carried interest is performance fee. Carried interest or performance fee is a fee charged based on the total amount of profits that have been earned by the fund. In other words, the performance fee is the share of the fund's net profits, which is to be paid to the General Partner.

source: forentis.com

So in the above example, it would be ($200 bn x 20% that is $40bn), and the rest will go to the investor.

Thus, Performance fee also refers to the General Partner being carried by investors because they receive a share in profits, which is unequal to the capital commitment to the fund. A GP will only commit 1-5% of the capital of the fund, but they get to keep 20% of the profit.

Carried Interest Example

Let's understand this more through an example

Say a PE firm called AYZ firm raises a $900mn fund, of this $860 mn, came from Limited Partners, and the remaining $40M coming from the General Partner. So GP contributed only 5% to the fund.

The GP, after receiving funds, would invest all of the capital in acquiring companies. A few years pass by; they exit all their portfolio companies for a $2B total. The LPs get $ 860Mn back first — that's returning their capital. That leaves $1.14 B left, and it's divided up 80 / 20 between LPs and GP. So the LPs get $ 912M, and the GP gets $228M. So the GP invested $40M at the start but got back $200M in profits. GP thus made a 5x return in this fund.

Sometimes carried interest is in the form of equity.

When carried interest is in the form of equity, then interest in a fund would be paid to GP as shares. The interest is in the form of equity is based on each Limited Partner's capital contribution, with a certain percentage of these shares allocated to the General Partner as carrying. Generally, this percentage is 20%. Carry shares mostly have a multi-year vesting period that tracks investments made.

Equity carry is divided between the senior executives working at the private equity firm. There are many flavors of carried interest, so making an exact comparison of two different carry packages is often difficult.

Performance fees motivate private equity firms to generate higher returns. The fees so charged are such that they align the interests of the general partner and its LPs.

What is the Hurdle Rate?

Many PE firms allow the performance fee post Hurdle rate. So the General Partner will receive the carry that is performance fee only when the fund is able to make profits above a certain hurdle rate.

Thus, the Hurdle rate is the minimum return that needs to be achieved before the profit is shared as per the agreement under carried interest.

- Funds have a hurdle rate of return so that a fund gives a performance fee to GP only after it has made a minimum pre-agreed profit.

- So a hurdle rate of 15% means that the private equity fund needs to achieve a return of at least 15% before the profits are shared according to the carried interest arrangement.

- In the PE industry, the most prevalent fee structure is commonly referred to as a "2 and 20," whereby a management fee of 2% is charged on assets under management or total committed capital. A 20% performance fee is assessed on fund profits.

- To understand these, let's see take this example if the limited partners get a preferred return of 10%, and the partnership delivers a 25% return, the GP would get 20% of the 15% incremental return delivered.

- In the absence of reaching the hurdle return, private equity managers will not receive a share of the profit (carried interest).

- Profits for the hurdle rate are calculated for the performance as a whole. That is for the whole amount invested, which can be 5-10 deals in a year and not on a deal to deal basis.

Why is this hurdle rate kept?

When a limited partner invests in private return, he is taking higher risk than the risk he would have taken by investing in normal markets or an equity index. The risk is higher than the market risk, so they demand a hurdle rate before sharing profits with the General Partner.

When are funds structured with Floor?

Some funds are structured with a "floor." In this type of set up carried interest would be allocated only when the net profits surpass the hurdle rate. This type of arrangement does not have the provision wherein GP can later catch-up, and hence it is strongly opposed by General Partners.

Is this Performance fee only for GP?

Interestingly, not many private equity teams get full money on their carry. It is so as retired partners also often are entitled to the share of carrying. This sharing is done as PE funds buy retiring partner's share in a fund at the time of retirement. This arrangement is active for a certain period of time post their retirement. Private equity firms may pay a significant amount of carry depending upon the situation. So if there is a spin-out of the firm or owned by a parent company or if the firm has minority shareholders, then the payment is as high as 10-50%.

What are Escrow and Claw-Back?

- Many limited partners demand to have an escrow and "clawback" arrangements. The reason they do so is to ensure that any early overpayments are returned if the funds underperform overall.

- For example, if the limited partners are expecting a 15% annual return, and the fund only returns 10% over a period of time. In this scenario, a portion of the carry paid to the general partner would be returned to cover the deficiency.

- This clawback provision, when is added to the other risks undertaken by the general partner, leads to PE industry justification that carried interest is not a salary; instead, it is an at-risk return on investment that is only payable only when the requisite level of performance is achieved.

- However, claw-backs are difficult to enforce. The difficulty arises when carry recipients are gone from the firm or when they have suffered any major financial setbacks.

- For example, they lost all of their carries because of one wrong investment that subsequently gave huge losses or when they used their carry to pay for a settlement.

Carry Structures from Around the World

- In research done, it was found out that generally, Limited Partners based in the US are more, where returns are often more outsized than in other countries. In the US, carry is based on a deal-by-deal basis with the escrow and claw-back provisions in force.

- On the other hand, Europe generally follows a whole-of-fund approach. Here the managing partners get their share of the profits simply after the investors have been paid capital and returns on drawn-down capital. Sometimes, carry is disallowed by some European investors for certain terms of the fund, such as 5 years.

- In Australia, Private equity is dominated by a few limited partners who tend to push for conservative carry terms. It is quite similar to the European model. In Australia, those funds who have a history of profitable performance, which is also consistent, can negotiate favorable carry terms, unlike others.

- When it comes to Asia- Pacific region, most of them have the GP clawback mechanism requiring the GP to return at the end of the life of the fund any excess carried interest it may have received as mentioned above.

General partners are the backbone of a PE fund. They are able to command better terms & capital commitment when they deliver good returns or when markets are enjoying the bull run. At the same time, Limited partners command better terms when the markets are unfavorable or in the bearish phase, like in 2008-2009 that post-financial crisis.

Post-2008-2009, the mechanics of PE funds have changed. As per the trends, LPs have started preferring reduced GP relationships. They have started eliminating non-performing GPs.

So given a future where we would see a significant preference on GP concentration and reduction in the overall number of funded GPs, the LP/GP power dynamic is expected to shift toward a selected number of "performing" GPs who would be able to command attractive fees and terms.