Table Of Contents

What Is Internal Failure Cost?

Internal failure cost refers to a type of cost of quality related to product failures discovered by an organization before any product leaves the manufacturing unit or factory. Determining such costs helps companies understand the extent to which the manufactured products meet the set quality standards.

A company incurs such costs internally. In other words, they do not involve any external party, like suppliers and customers. These costs may include the cost of scrap, rework, etc., and they can significantly affect an organization’s profitability by raising the production cost. Organizations must spot and reduce these costs to ensure their product’s reliability and maintain quality.

Table of contents

- Internal failure cost refers to the cost a company incurs when they identify any manufacturing defect before sending products out for delivery. Spotting and minimizing such costs are essential to ensure customer satisfaction and the overall efficiency of the business.

- A popular way to lower this cost includes implementing an effective system concerning quality control

- One key difference between internal failure cost and external failure cost is that an organization incurs the latter to determine the extent of compliance with the set quality standards. That said, businesses incur the former cost when product-related defects arise.

Internal Failure Cost Explained

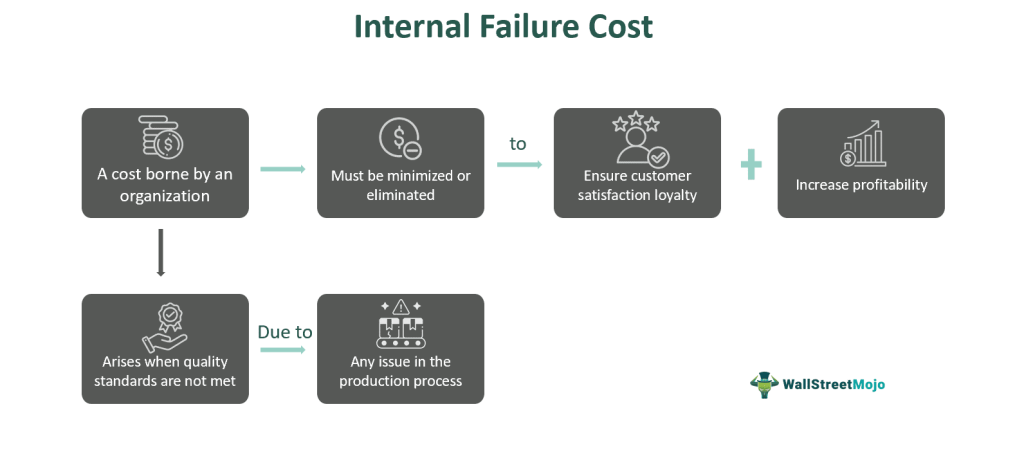

Internal failure cost refers to the cost borne by an organization when its products fail to meet the predetermined quality standard and need repair, replacement, or rework. Businesses must aim to identify and minimize such costs to improve their profits and improve customer satisfaction and loyalty.

Note that a problem at any stage of the production process can lead to an organization incurring such costs. That said, if any defect in products does not exist before they leave the organization’s factory, these costs will not exist.

Given below is a list of such costs that businesses must be able to monitor:

- Rework

- Scrap

- Rework inspection

- Supplier rework

- Scrap disposal

- Downgrading

- Additional material procurement

- Inspection of rework

- Software redesigning

- Variability of product features

- Alteration in selling price, etc.

Organizations efficiently managing such costs can be in a more favorable position to provide top-quality products to their customers while ensuring competitiveness and enhancing operational efficiency.

To understand the concept better, individuals need to be aware of some key causes of the costs mentioned above. Hence, let us look at them.

- Insufficient training of workers

- Ineffective and inefficient quality control processes

- Poor product design

- Lack of standardization of processes

- Poor supplier quality

Examples

Let us look at a few internal failure cost examples to understand the concept better.

Example #1

Suppose Company ABC manufactures laptops. After the production process was complete and all the products in that batch were ready for delivery to customers, it was found that a certain percentage of the products had issues related to the motherboard, and they would not turn on. Hence, the company fixed the problem by repairing or replacing the components entirely.

The costs borne by the business to address the issue are the rework costs. After completing the work, the fixed laptops had to undergo another round of testing. For that, the company incurred retesting costs. The costs associated with resolving the issues and doing the retesting were internal failure costs.

Example #2

Spirit AeroSystems reported a loss of $204 million owing to high fuselage rework costs and an increase in labor and supply chain expenses. The organization recorded $49.3 million worth of additional 737 program expenses, which reflected the rework of the aft-pressure bulkhead, thus raising the internal failure costs. In August 2023, the company disclosed that it found defective holes in the 737 aft-pressure bulkheads, which required them to check and fix the components that were undelivered. Spirit AeroSystems needs to minimize such rework costs to improve its bottom line and improve customer loyalty.

How To Reduce?

Businesses can take the following measures to minimize such costs:

- Execute an efficient and effective quality control system

- Focus on employee development and training

- Carry out root cause analysis to identify the reasons behind the issues.

- Ensure efficient management of suppliers to ensure the delivery of top-quality products

- Execute an effective risk management program to spot potential risks.

- Focus on continuous improvement.

Advantages And Disadvantages

Let us look at the benefits and limitations of this kind of cost.

- Spotting it helps organizations ensure early identification of defects. This, in turn, helps businesses minimize replacements for their customers and expensive fixes. As a result, they can save money over the long term.

- Identification and elimination of these costs allow for cost savings via enhanced measures concerning quality control by helping in spotting and addressing issues and defects in the early stages of the production process.

- Businesses can improve their efficiency by determining such costs because fewer resources are necessary to replace and fix defective products before customers get delivery. This also improves customer satisfaction because they get products that fulfill their expectations.

- Tracking and minimizing such internal failure costs in a company prevents external failure costs. The latter costs are usually higher. Moreover, they are more challenging to fix since businesses can only identify them once the products reach customers.

Disadvantages

- It is not always possible to spot all issues before delivery. Hence, businesses often end up overlooking a few problems that result in external failure costs.

- Quality control and assurance procedures might not be that effective, which can lead to such costs rising.

- These costs can result in dissatisfied customers because they do not get products that fulfill their expectations.

- Spotting such costs can be quite expensive as businesses require additional personnel to spot and rectify the issues detected before products leave the manufacturing unit.

- Businesses may not have clearly established quality standards, which can increase such costs.

- If such costs are high, a company can become less competitive in its industry.

Internal Failure Cost vs Appraisal Cost

The table below highlights the main differences between internal failure cost and appraisal cost to help individuals get a clear idea.

| Internal Failure Cost | Appraisal Cost |

|---|---|

| It refers to the cost related to the defects spotted before customers get the products. | Businesses incur appraisal costs to figure out the extent of conformance to the set quality-related requirements. |

| Examples of such a cost can be cost incurred by a business for inspection, training, rework, and scrap. | Examples of appraisal costs include sampling and testing costs, inspection fees, labor and workforce costs for samplers, testers, and inspectors, facility fees, etc. |

Frequently Asked Questions(FAQs)

- Businesses incur costs internal to them before products reach the customer. On the other hand, organizations incur external failure costs after products reach the customers.

- Internal failure costs in a company include rework and scrapping costs. On the other hand, examples of external failure costs include repairs, returns, and warranty claims.

- External failure costs have a direct impact on customer satisfaction, unlike costs arising due to defects before customers get delivery of the product.

Businesses incur prevention costs to prevent the chances of defects arising in products. ON the other hand, the other type of cost is borne by an organization when it spots product-related defects.

Yes, they can impact such costs. This is because organizations may need to spend more funds to ensure the products adhere to the new rules and regulations.

Recommended Articles

This has been a guide to what is Internal Failure Cost. We explain its examples, comparison with appraisal cost, advantages, and how to reduce it. You can learn more about financing from the following articles –