Table Of Contents

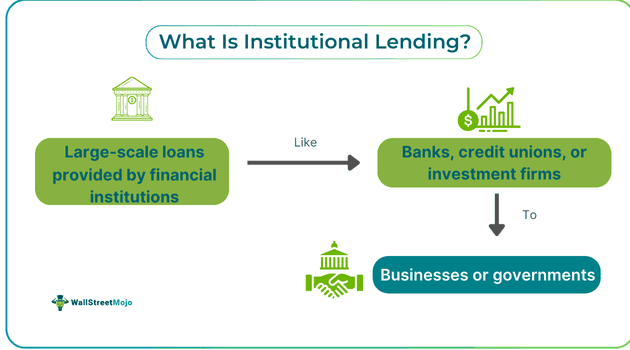

What Is Institutional Lending?

Institutional lending refers to non-federal student loans that educational institutions, colleges, and universities offer. These loans are considered private education loans distributed to students from the college they are enrolled in, but they are vastly different from traditional private lending services.

You are free to use this image on your website, templates, etc.. Please provide us with an attribution link.

Such lending comes with short-term or long-term repayment terms, which typically vary from one college to another. The student is observed as a borrower and is expected to repay the loan with interest over some time. Such lending is generally designed to use the funds for tuition and other educational expenses and fees only.

Key Takeaways

- Institutional lending is loans offered by colleges and universities to their enrolled students for tuition and other educational expenses and fees.

- Short-term loans may have a minimum or no interest rate, but only a small processing fee, but long-term loans can last up to 10 years with an interest rate ranging between 3% to 10%, depending on the school or college.

- In other contexts, institutional lending is also considered a specific type of financing where an established institution offers funds to similar business types.

- These lending solutions are different from traditional loans and do not carry federal loan benefits. Hence, students must read all the terms and conditions before signing.

How Does Institutional Lending Work?

Institutional lending is financing solutions offered by schools, colleges, and universities to students enrolled in them for a particular class or degree. This lending operates like a non-federal student loan, which generally covers all the expenses related to tuition, fees, and other educational costs. Such lending options serve as a secondary borrowing solution for students who are not planning to take private student loans from big banks and well-established financial institutions.

Institutional lending offers both short-term and long-term loans. If it is a short-term loan, the interest rate can be as minimum as 1% depending on the school or college; it may happen that a student will be charged no interest at all but only a small processing fee, but since it is a short-term loan, the student is expected to repay the loan in a few months. In contrast, long-term loans by schools and colleges can be for a wider term period, as large as 10 years, with an interest rate ranging between 3% to 10%. Students should understand that schools or colleges may not require a credit check but have criteria such as minimum GPA, half-time enrollment, and more as part of their lending and selection process.

In the business and finance world, institutional lending has a broader scope and also refers separately to funds offered to small businesses for their growth and expansion. Like every other loan, these come with interest rates, and the borrower must repay within the loan term. Whether it is an unsecured business or institutional lending-based student loan, a borrower must read and understand all the terms and conditions of the loan.

Applications

The applications of institutional lending are –

- It helps students with an interest in studying and acquiring knowledge and education but who need more financial stability.

- It serves as a viable credit option for students who want to avoid taking private student loans.

- Encourage students to apply for institutional loans and offer affordable education with flexible payment options.

- When colleges offer loans, they gain benefits from the interest payments and operate as a credit offering entity.

- In other financing contexts, institutional lending helps businesses have better loan options for different types of business needs and operational investments.

- Institutional lending is a common solution among HFCs, MFIs, and NBFCs to lend onward to their existing borrowers.

- Such companies and corporations are readily interested in institutional lending and offer them forward against property, vehicle, gold, personal, and unsecured loans.

- It can be used and offered to different types of institutional clients across different industries, asset classes, and borrowing needs.

Examples

Below are two examples of institutional lending.

Example #1

Suppose Jennifer decides to pursue a bachelor's degree in journalism. She knows which college she wants to attend but lacks funds. Instead of taking out a traditional private student loan, Jennifer decides to take out institutional loans; she does foolproof research and finds out that her college offers institutional loans.

She filled out the FAFSA form and met with her college's financial aid officer. The officer guided Jennifer through all the details and information, including required documents, loan terms, amount, interest rate, and other payment options. The best part was that Jennifer did not have to go through a credit check.

Jennifer finds this type of lending more helpful than other traditional and federal loan options and takes it. Within the next three years, she repays the loan. Now, this is a simple institutional lending option, but in the real world, many aspects need to be considered.

Example #2

In 2024, FRNT, a Toronto-based institutional capital markets and advisory platform, announced a strategic collaboration with digital asset custodian BitGo. This partnership has led to the launch of a new institutional-only lending platform that offers significant advantages for both lenders and borrowers over existing industry structures. The platform is designed to provide a seamless and secure lending experience, leveraging a tri-party structure with BitGo to mitigate counterparty risk.

The new platform addresses the rising demand for digital asset-backed lending solutions, allowing lenders to confidently lend against assets like Bitcoin (BTC) and Ethereum (ETH) without handling the physical assets. With features such as automated margin calls and 24/7 monitoring, the platform offers a robust solution for institutional clients. Borrowers can access dollar liquidity while maintaining long exposure to their collateralized assets, presenting a secure and efficient opportunity for both sides of the lending equation.

Pros And Cons

The pros of institutional lending are –

- Such lending only sometimes requires a credit check from the student, but again, it depends on the college or university.

- Institutional lending offers low interest rates, easy payment options, and is inexpensive compared to traditional private student loans.

- Depending on the school or college, minimum or no eligibility criteria are required; the whole process can be done smoothly.

- It serves as a good borrowing option for students who are not interested in traditional and private education loans.

The cons of institutional lending are –

- Institutional lending does not offer the same benefits as federal loans.

- Since schools and colleges are approving it, each has its set criteria, and so there is no guarantee of approval.

- Although it is of great help, it may not match the borrowing student'sstudent's needs and requirements.

- Either the school or a hired agency looks after the whole lending process, which can create complications in the lending and approval procedures.