Table Of Contents

Incurred Cost Meaning

Incurred cost in accrual accounting refers to the expense of the company when an asset is consumed, which the company becomes liable for and may include direct, indirect, production, and operating expenses incurred for running the company's business operations. It also includes all the prior period expenses, i.e., costs incurred before the company came into existence. Incurred Costs are an expense for the company and are recorded on the debit side of the profit & loss account.

Table of contents

- Incurred Cost Meaning

- Every company needs to plan its expenses most conservatively since they are the lifeline of the business and are required to be paid on time.

- A thorough analysis of the company's cost structure will help the management make some strategic decisions that will impact the company's growth story.

- For a company to analyze cost structure, it needs to consider both cash and no-cash expenditures to arrive at the correct cost for the product.

- Since the company's selling price depends upon the cost incurred, many companies try their best to keep the cost low by not allocating expenses that are not that relevant to making the finished product. Instead, only relevant expenses are considered as “Cost Incurred” for the product to keep the selling price at the lowest.

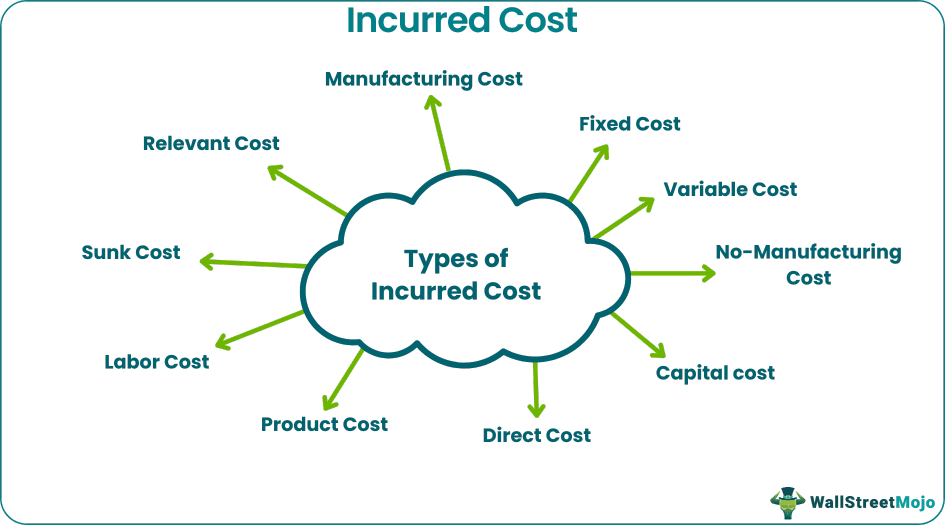

Top 10 Types of Incurred Cost

- Manufacturing Cost refers to the cost incurred to convert raw materials into finished goods. They are used in direct materials, direct labor, and direct expenses, which form part of the cost of goods sold and are debited to the trading account in the financial statement.

- No-Manufacturing Cost: It refers to all the costs incurred, which are not manufacturing in nature, i.e., it includes operating, admin, and selling expenses.

- Fixed Cost: Fixed cost refers to the company's fixed expenses to run the business. It includes rent, salaries, and other expenses that are payable monthly.

- Variable Cost: Variable Cost refers to the cost incurred for the product to be sold in the open market.

- Capital cost refers to the cost incurred for buying a capital asset.

- Direct Cost: Direct Cost refers to the cost incurred to convert raw materials into finished goods and is directly related to the company's finished product.

- Product Cost: Product Cost refers to the cost incurred to make the product saleable. The entire cost of the product is done by considering all the necessary expenses incurred to make the finished product saleable in the market.

- Labor Cost: It refers to the cost incurred on the employees of the company or the laborers to keep the work going

- Sunk Cost: It refers to the historical cost incurred by the company and does not make any difference in the decision-making.

- Relevant Cost: It refers to the cost incurred, which is relevant in the company's decision-making.

Examples of Cost Incurred

Below are some examples of the cost incurred by the company.

- Rentals: It refers to the amount the company spends at the beginning of the year to reap the benefits for the full year. Rent per month = Total Rent Paid / 12.

- Telephone: It refers to the telephone expense paid by the company. Even if the bill has not been generated, it is a cost incurred and must be booked as an expense in the Profit & Loss Account.

- Supplies: It refers to the purchase of raw materials for the company to make the finished Goods. Even if it is not paid immediately, it is an expense for the Company and must be recognized as a liability on the Balance Sheet.

- Depreciation: Depreciation refers to the benefits gained from using the Asset over the period. Even if it is a non-cash Expenditure, it must be booked as an expense in the Income Statement.

- Salaries: It refers to the fixed expense paid to the company's employees or the labor workforce to keep the business operation running.

- Sundry Expenses: These are miscellaneous expenses incurred by the company daily and form a part of the cost structure.

Advantages

Below are some of the advantages.

- It helps the company to run its business operations smoothly since all the direct and indirect costs need to be paid on a timely basis.

- It helps the management know the exact requirement of the company to remain in the business by analyzing the cost structure.

- It helps the management prepare a detailed business plan for the future since they are already aware of the cost and the cost structure of the product, thus giving them the benefit of projecting the cost for the company in the coming years.

Disadvantages

- A higher cost structure in the early stages of the company may result in a greater liquidity crisis due to excessive costing.

- Some costs are non-cash in nature and hence do not impact the actual costing.

Conclusion

The cost incurred by the company right from its early stages plays a crucial role in its long-term survival. Generally, the companies in their early stages incur more costs than the established ones since they are new in the market, and there is a need to build the necessary infrastructure and invest in the right human capital to excel in the business.

Recommended Articles

This article has been a guide to "Incurred Cost" and its meaning. Here we discuss the top 10 costs incurred by the company along with examples and explanations. You can learn more about financing from the following articles –