Table Of Contents

What Is Income Tax Expense?

Income tax is a type of expense that is to be paid by every person or organization on the income earned by them in each financial year as per the norms prescribed in the income tax laws. It results in cash outflow as income tax liability is paid out through bank transfers to the income tax department.

All companies and individuals with a taxable income are liable to pay taxes. For companies, this translates into an expense on their income statements and takes away a significant part of their profits. It poses a great disadvantage to the stockholders of the company. Since income tax is to be paid only if there is taxable income, companies try to further minimize their taxable income by under-reporting profits or showing excessive losses.

Table of contents

Income Tax Expense Explained

The corporate income tax expense is a component that features on the income statement under the heading of 'other expenses.' it is a type of liability on the business or an individual. It is a tax levied by the government on a business's earnings and an individual's income. Income tax is considered an expense for the business or individual because there is an outflow of cash due to tax payout. After the taxable income is determined, the business or individual is liable to pay income tax on that income.

- The tax liabilities are determined through income tax returns filed by businesses and individuals alike. The government uses this tax money for funding the provision of public goods like roads, bridges, basic healthcare, etc. In most countries, a separate agency or institution is set up to collect taxes on income.

- After the necessary deductions, exemptions, and tax credits, the final taxable income is calculated for each individual. For instance, individuals are liable to pay individual income tax on their salaries or wages. Similarly, businesses are obligated to pay income tax on their annual earnings after deducting operating expenses.

Further, given the accounting methods, income reported for tax purposes sometimes varies from income reported for financial purposes.

It leads to complexities in calculating income tax expense on income statement for the company. Hence, analysts or other stakeholders should be very careful while assessing a company's performance to get around these complexities in determining the income tax.

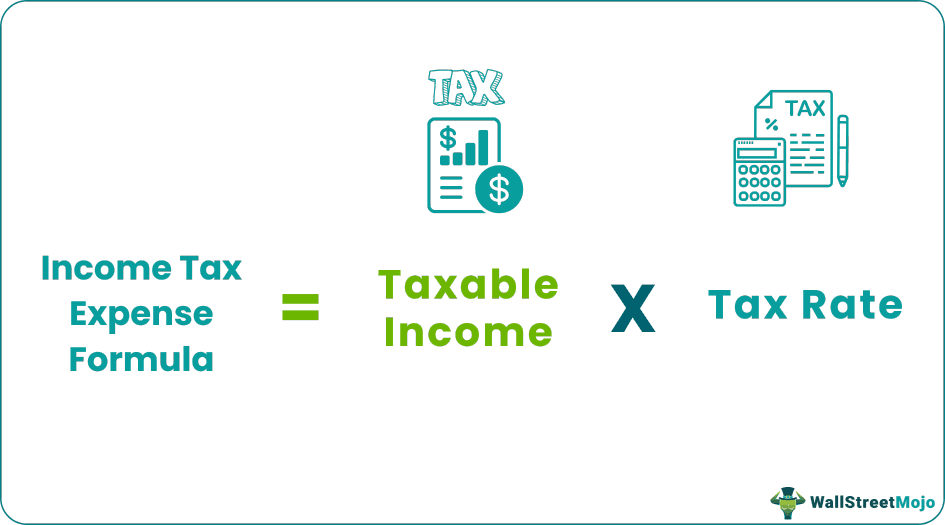

Formula

The standard formula for income tax expense on income statement is as follows:

Income Tax Expense Formula = Taxable Income * Tax Rate

Additionally, income tax is arrived at by showing only the tax expenses that occurred during a particular period when they were incurred and not during the period when they were paid.

How To Calculate?

Income tax is calculated for a business entity or individual over a particular period, usually over the financial year. This formula used to calculate income tax expense is simply the tax rate multiplied by the taxable income of the business or individual. Firstly, the taxable income of the individual and taxable earnings of the business entity is to be determined. It is a complex process since different sources of income are taxed differently.

For example, a company has to pay one kind of tax on the salaries it pays to employees – payroll tax, then another tax on purchasing any assets – sales tax. Further, there are taxes levied at the state or the national level as well. Hence, the correct tax rate should be determined, as this will ultimately affect the company's income tax expense. It can be done with the help of accounting standards like Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standard (IFRS).

Revenue vs Income Explained in Video

How To Record?

Given below are the steps for recording the corporate income tax expense.

- The first step is to determine the applicable tax rate. This can be determined by keeping track of the applicable rate in that jurisdiction or the company policies.

- The next is to calculate the income on which tax will be charged. This is done by calculating the income as per the income statement, based on the different deductions and adjustments.

- Then comes the tax calculation. As per the prevailing rate, the the company will calculate income tax expense using the formula give in this article above, which will calculate the tax expense.

- Next will be passing the journal entry in the books of accounts as per the double entry system. The entry will be as follows:

- Income Tax Expense A/c Debit

- To Income Tax Payable A/c

- The debit increase the tax expense in the income statement, reducing the profit and the credit shows the liability amount in balance sheet.

- Disclosure has to be made in the financial statement and footnotes which will provide any additional information regarding the same like deferred tax assets or liabilities or any tax credits.

- The final step is the reconciliation that should be done at the end of the accounting period. This is important to find differences between the estimated amount and the amount actually paid.

Thus the above are the steps of recording the expense in the books of accounts.

Example

To understand this further, let us take an example. Here the company's taxable income means net income, which is arrived at after subtracting non-taxable items and other tax deductions. For instance, there is a certain Company, ABC, whose taxable income for the current accounting period is $ 2,000,000, and the tax rate levied is 25%.

Hence, the calculation is as follows,

Income Tax of Company ABC = $ 2,000,000 x 25% = $ 5,00,000

Hence, Company ABC has to undergo an income tax of $ 500,000 in the current accounting period based on the tax rate of 25%.

Further, the income tax is estimated by adding deferred tax liability and income tax payable. Here, deferred tax liability refers to the company's taxes yet to pay. A deferred tax liability may occur due to a difference in the company’s accounting technique and the tax code, which determines taxable income.

Important Points About Income Tax Expense Income Statement

The following are the important points about this tax expense.

#1 - Minimizing Taxable Income

As mentioned above, income tax involves an outflow of cash; hence, it is seen as a liability for the company. Income tax expense is paid out of the operating profits of the entity. It means that if companies didn’t have to pay taxes, that amount of money could be used to distribute as profits among stockholders. Therefore, companies try to minimize their tax expenses because otherwise, they would eat into the profits and make stockholders unhappy.

#2 - Losses And Taxable Income

Income tax is levied on taxable income only. It means there is no tax expense recorded in the income statement. So if a company is running in losses, it has zero taxable income. Further, the company can carry forward its losses to the following years and sometimes even cancel out the future tax liability.

#3 - The Difference In Financial Accounting And Tax Code

Depending on the accounting standards given by GAAP and IFRS, often, the reported income by companies on their income statements differs from the taxable income as determined by the tax code. One reason this may occur is that, on the one hand, as per accounting standards, companies employ the straight-line depreciation method to determine depreciation for that financial year. On the other hand, as per the tax code, they can employ accelerated depreciation to determine the taxable profit. It is where the mismatch between the income tax expense and the tax bill is.

Income Tax Expense Vs Income Tax Payable

Both the above are two different accounting terms that are commonly associated with tax payment related to business. However, there are some basic differences between them as follows.

- The former refers to the amount that the business will identify as the amount of tax that it has to pay as per its profit and los statement related to an accounting period. But the latter refers to the amount of tax that it has to pay to the tax authorities at a point of time.

- The income tax expense account shows the amount of liability related to taxes as per the income earned, but the latter shows the liability that is to be paid, and already incurred.

- The former provides a clearer picture of the profit earned by the business, but the latter shows the amount to be settled with the tax authorities.

- The purpose of the former is to assess and match the tax expense with the revenue, but the purpose of the latter is to assess the liability amount in the balance sheet of the business.

- The income tax expense account is shown in the income statements as expense, which reduces the profit, but the latter appears in the balance sheet as a liability.

- The former is a part of the accounting principles followed in an organization and may not match with the actual time of tax payment, but the latter shows a liability that is to be paid immediately either in instalments or lump sum.

Thus, the above are some differences between the two concepts. However, the amount of the two may not match due to differences in time and tax related rules.

Recommended Articles

This article has been a guide to what is Income Tax Expense. We explain it with formula, how to calculate, differences with income tax payable & example. You can learn more about financing from the following articles –