Table Of Contents

What Is Income Tax Accounting?

Income tax accounting is required to recognize the income tax payable in the books of account and determine the current period's tax expenses. It has to be paid before or after the end of the financial year and recognized in the books of account accordingly.

There is a difference between value recognized in the financial statements for financial reporting and value recognized for tax purposes. However, this item is crucial during preparation of the profit and loss account. The concept is governed by Internal Revenue Code, specifying the rules that companies should follow while accounting for taxes and filing returns.

Table of contents

Income Tax Accounting Explained

The concept of Income Tax accounting involves following certain methods and steps that will help in recording the income tax to be paid by the entity in books of accounts. The main purpose of this procedure is to have a proper tracking system that will record the funds moving in and out related to income tax.

There are certain rules and guidelines to be followed regarding the income tax accounting treatment, which includes all foreign and domestic taxes. The current tax, which is for the current period is recorded as a liability to the amount that is unpaid. This amount as per the income tax accounting standard is the one that the entity has to pay to the tax authority, as per the applicable tax rates and laws.

In the accounting field, accounting for income tax occupies a significant position. It is useful and is done with the aim of getting a clear and precise valuation of the business. Every company should be able to align its operating strategy with the tax liabilities and make changes to reduce the liabilities accordingly. Proper accounting for tax on income earned will provide transparency and flexibility to the capital structure and keep more funds available for other useful purpose.

This concept also allows corporates to regulate the cash flow or control and minimise that tax to be paid. It is necessary to track and regulate the timing of tax payment so that funds remain for a longer time within the business. Overall, all the above can be achieved if the accounting for income taxes are done.

Key Terms Used

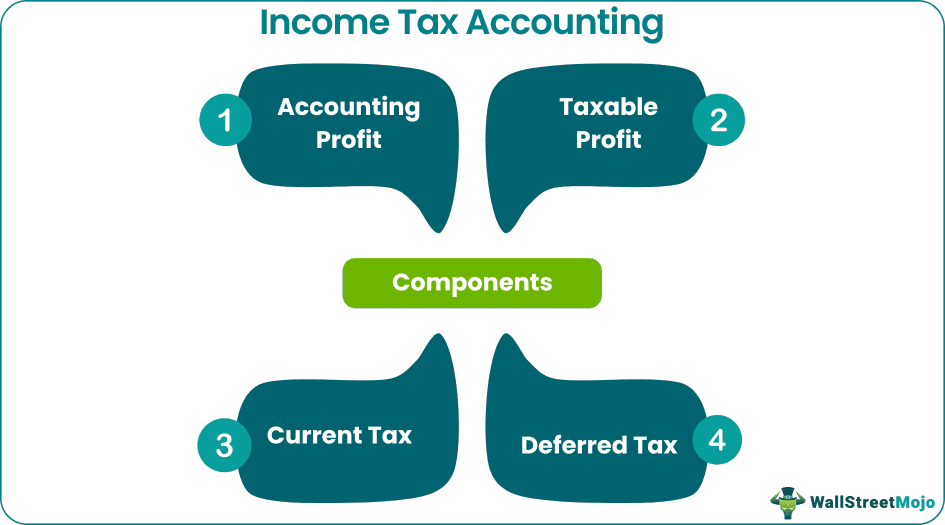

Understanding the income tax accounting standard, first, we need to understand the meaning of the below components:-

- Accounting Profit - Accounting profit means profit, shown in the profit & loss statement after considering all the income and expenses but before tax.

- Taxable Profit - Taxable profit means profit, which is arrived at as per tax laws and on which tax needs to be paid as per tax law.

- Current Tax - The current tax is the tax payable or paid on taxable profit as per the applicable tax rate of the current year during income tax accounting entry.

- Deferred Tax - Deferred tax is a tax that arises due to timing differences. Temporary / Timing differences are the differences between the carrying amounts of assets and liabilities in the financial statement and the number of Assets and liabilities attributed to the tax base.

Example

If we purchase one asset worth $1000 at the beginning of the year and the Depreciation rate as per financial reporting purpose is 10% and as per tax law is 20%, and profit before depreciation and tax is $ 500.

- Accounting profit will be ($500 – Depreciation as per accounting ($1000*10% = $100) i.e. $400.

- Taxable Profit will be ($500 – Depreciation as per tax ($1000*20% = $200)) i.e. $300

- Current Tax will be payable on $300 *Tax Rate.

- Deferred Tax will arise on temporary difference, i.e., the difference between depreciation as per accounting and depreciation as per tax. In the above example, the deferred tax will arise at $100.

Income Tax Types Explained in Video

Journal Entry

Here are the step by step guide regarding the income tax accounting entry that are used for recording the transactions related to the same.

1. Provision of Income-tax – Provision of income tax recorded in books of account by debiting Profit & Loss a/c, which will show under liability in the Balance Sheet.

2. Advance Income tax payment – Advance income tax will show under Assets in the Balance Sheet.

Deferred Tax Assets And Deferred Tax Liabilities

Deferred tax is of two types - Deferred tax Assets and Deferred tax liabilities.

#1 - Deferred Tax Assets (DTA) - DTA arises when book profit is lesser than the profit calculated per tax. We understand this with the below example. E.g., X Ltd. Has a profit as per the Profit & Loss statement is $5000 before giving the effect of depreciation and the depreciation rate is 20% per financial reporting purpose and 10% per income tax purpose.

- Profit as per Financial Statement – $5000 – ($5000 *20%) =$ 4,000

- Profit as per Tax Purpose – $5000 – ($5000 *10%) = $4,500

Since Tax profit is more than the book profit; therefore, we have to pay more tax now, and less tax in future and due to this DTA will arise, and DTA will be ($4,500 – $4,000) *Tax Rate

#2 - Deferred Tax Liabilities (DTL) - DTL arises when book profit is more than profit calculated as per tax. We understand this with the below example.

E.g., X Ltd. has a profit of $5,000 after considering the interest receivable of $500, but as per income tax, interest is taxable when it is received.

- Profit as per Financial Statement – $5000

- Profit as per Tax Purpose – $5000 – $500 = 4,500

Since the Tax profit is lesser than the book profit, we have to pay less tax now and more tax in the future, and due to this, DTL will arise, and DTL will be ($5000 – $4000) * Tax Rate.

Recognition of Deferred Tax

Deferred tax assets will recognize in books of account by crediting the profit & loss a/c, and deferred tax liabilities will recognize by debiting the profit & loss a/c

Journal Entries are as follows:

Advantage

Let us study some of the advantages of the concept of income tax accounting treatment, as given in the points below.

- If a business entity is doing tax accounting, it helps them to file the tax return.

- It saves the time of a business entity for doing the calculation when filing a tax return.

- A business entity can do tax planning.

- By maintaining only one accounting system, you can save the cost of human resources and cost of accounting software.

- It also ensures that the business complies with the regulatory and the legal requirements that it should follow regarding the operation. This helps in avoiding any legal and regulatory issues or any penalty.

- The process ensures that the business runs in a transparent manner. The business needs to inform the stakeholders regarding its income or profits, the tax liability and liquidity available to meet them.

- Future tax planning can be done because the business can identify the funds moving out of business in the form of taxes and change its strategies accordingly to retain more funds within the business.

Disadvantages

Some disadvantages of the concept are given below.

- Only a small business entity can maintain only tax accounting.

- It will not give the correct picture of operational cost and benefit.

- Companies that must get their accounts audited. The process is not complete and they can’t follow only the income tax accounting method.

- The financial statements and data shown to the stakeholders only has value if they are properly audited.

- It is a complex process, and the complexity increases if the business is spread globally because different counties may follow different procedures for accounting. This requires proper coordination between branches and subsidiaries to present the financial data in a way that is easily understood by the stakeholders.

- Any change in laws and rules related to taxation will have to be implemented to reflect the tax position clearly. However, entities often have to record for any uncertainty regarding tax payments.

- There is always a risk for failure to follow the rules and adhere to the legal aspects of accounting because of their complexity or tendency for personal gains. This leads to legal issues and penalty.

Thus, we see that there are a lot of benefits as well as challenges in the entire process. But even then, it is important to strictly follow the laws and standards related to the accounting for income tax, to ensure transparency and reliability of the books of accounts.

After reading the above, we understood that there is a difference between accounting profit and taxable profit. Before arriving at a profit as per income tax, we have to understand provisions under income tax and calculate taxable profit. Suppose an entity follows a tax accounting system at the end of the year. In that case, they need not be required to calculate taxable profit, but this is limited only to those organizations on which companies Act is not applicable and need not be required to maintain books of Accounts as per accounting standard.

Recommended Articles

This has been a guide to what is Income Tax Accounting. We explain it with the key terms used with example, journal entries, advantages & disadvantages. You can learn more about accounting from the following articles –