Part of our Cost Classifications guide

What Are Implicit Costs?

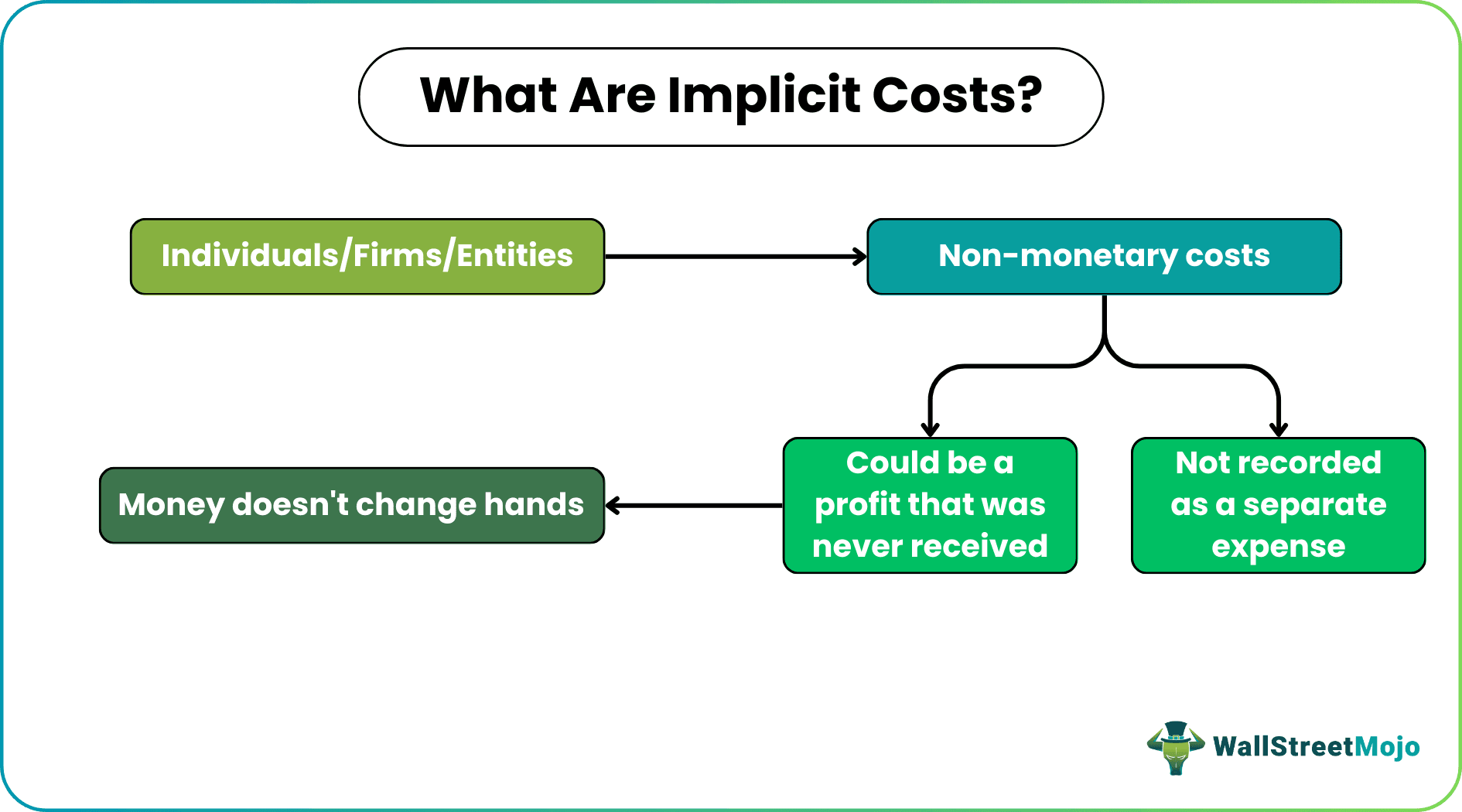

Implicit costs refer to the costs that the companies bear without having to show them as an expense from their side. This happens as these do not have any individual existence and could be any money that firms have missed out on, for making some kind of payments, even before they receive them.

As these earnings are never recorded as an inflow, their records as cash outflow are also never found in the financial statements. These monetary sources never change hands and are never transacted. They are used even before the recipients can count them in. Hence, they become implicit costs.

- Implicit costs are expenses off records. These are borne by the companies through internally available resources rather than utilizing the funds recorded in the financial statements.

- These costs are neither recorded nor reported, given the non-monetary transactions involved where no change of hands occurs.

- Such costs differ from explicit expenses, which are out-of-the-pocket costs that find official entry into a firm’s financial statements.

- Implicit costs do not represent real expenses.

Implicit Costs Explained

Implicit costs in economics involve the expenses that are borne using internal resources of the companies as recorded. As the firms do not record them officially, they become informal expenses. Hence, companies implicitly use the funds to settle financial commitments without recording them as real expenses.

An implicit expense could either be any fund that a company is yet to receive or any internally preserved resource. Though the transaction never occurs, it is still used to handle financial requirements without changing hands. For example, while calculating implicit costs if a firm owns spare land, it can use it to set up a new plant to speed up production. Here, the company uses its internal resource without having to pay for them or receive any rent from others using them. So, the cost becomes an implicit cost.

In short, an amount earned or spent for any required resource, which is internally available, is implicit. Also known as notional cost or implied cost, the implicit costs in economics involve an organization’s calculation of what the business earned if, instead of using the resource in the business activity, it used the same resource for some other purpose. Those other purposes might include renting assets to another party and the rent they would have earned as the opportunity cost.

Implicit Cost Video Explanation

How To Calculate?

Knowing the calculations involved helps us understand the implicit costs definition better. Let us check how to calculate these costs:

If one rents out a fixed asset, it might yield higher returns than what a business could earn by using it for carrying out its business operations. This signifies that a company chooses to be at a loss in terms of economic profit. This shows how unfruitful it is for businesses to use internal resources to fulfill their requirements rather than use them and earn through rent or sale.

When these costs are calculated, they are tough to be figured out or identified on a company’s financial statement. This is because these costs could be both tangible and intangible. Some typical examples of calculating implicit costs would be the time and resources invested in training an employee, depreciation on equipment, etc. However, some could still technically consider depreciation an explicit cost because it represents realistic capital consumption for a resource for which a company records a real expense at on point in time.

Examples

Let us consider the following implicit costs of production examples without and with calculation to understand the concept better:

Example #1

The list of implicit costs that fall under the implicit category includes:

- Payment expected through rents

- Annual earnings from stocks on selling a business

- Time spent on carrying out a business function

- Interviewers taking out time to conduct interviews

Thus, implicit costs of production expenses could be both tangible and intangible.

Example #2

ABC invests $10,000 in certain businesses, intending to earn probable profits worth $5000 in a year. First, however, it has to forego the interest it is likely to earn on the sum to make this profit. Let’s say the firm foregoes a 12% annual interest, which would have yielded $1200 in a year. This $1200 represents the implicit cost of investing the sum elsewhere. Though there is no specific implicit costs formula, the figures are easily identifiable.

The above examples helps us to understand the topic better. They help in identifying the particular type of costs and also show with a hypothetical example, how we can actually calculate the amount from a given case.

Implicit Costs Vs Explicit Costs

While list of implicit costs are neither earned nor paid, explicit costs are the expenses that are formally recorded and involve a change of hands. Some of the major differences between the two costs are as follows:

| Category | Implicit Costs | Explicit Costs |

|---|---|---|

| Transaction | No payment involved | Involves payment |

| Records | Neither recorded, nor reported | Both recorded and reported |

| Includes | No monetary transactions included | Cash outflow |

| Calculates | Economic profit | Both accounting profit and economic profit |

The above chart points out the basic differences between the two financial concepts. It is necessary to be able to differentiate them clearly so that we are able to identify them in a business and deal with it accordingly.

Frequently Asked Questions (FAQs)

Are implicit costs opportunity costs?

These are opportunity costs as they allow firms to use their internally available resources to carry out business functions without explicitly using monetary funds to bear the costs involved. They do not represent real expenses. Still, they are considered opportunity costs for utilizing a company’s assets or resources. For instance, if a company sets up a production plant on its land, by implication, it does not earn any possible rent on the same property and if it could, it would not have used the resources itself.

Are implicit costs direct or indirect?

These costs are categorized as indirect expenses despite being unrecorded, unreported, and unofficial costs. It does not come as a grant or sanction from authorities or used for a particular cost objective and hence, is not identified as a direct cost. Instead, these expenses are associated with a business’s two or more cost objectives, thereby falling under the indirect cost label.

What are implicit costs used for?

It calculates the economic profit by deducting both explicit and implicit costs from total revenues. This gives a better idea of whether the resources were employed profitably enough or could have been employed better.

Recommended Articles

This article has been a guide to what are Implicit Costs. We explain the differences with explicit costs, along with examples & how to calculate it. You may learn more about Corporate Finance with the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.