Table Of Contents

Impairment Meaning

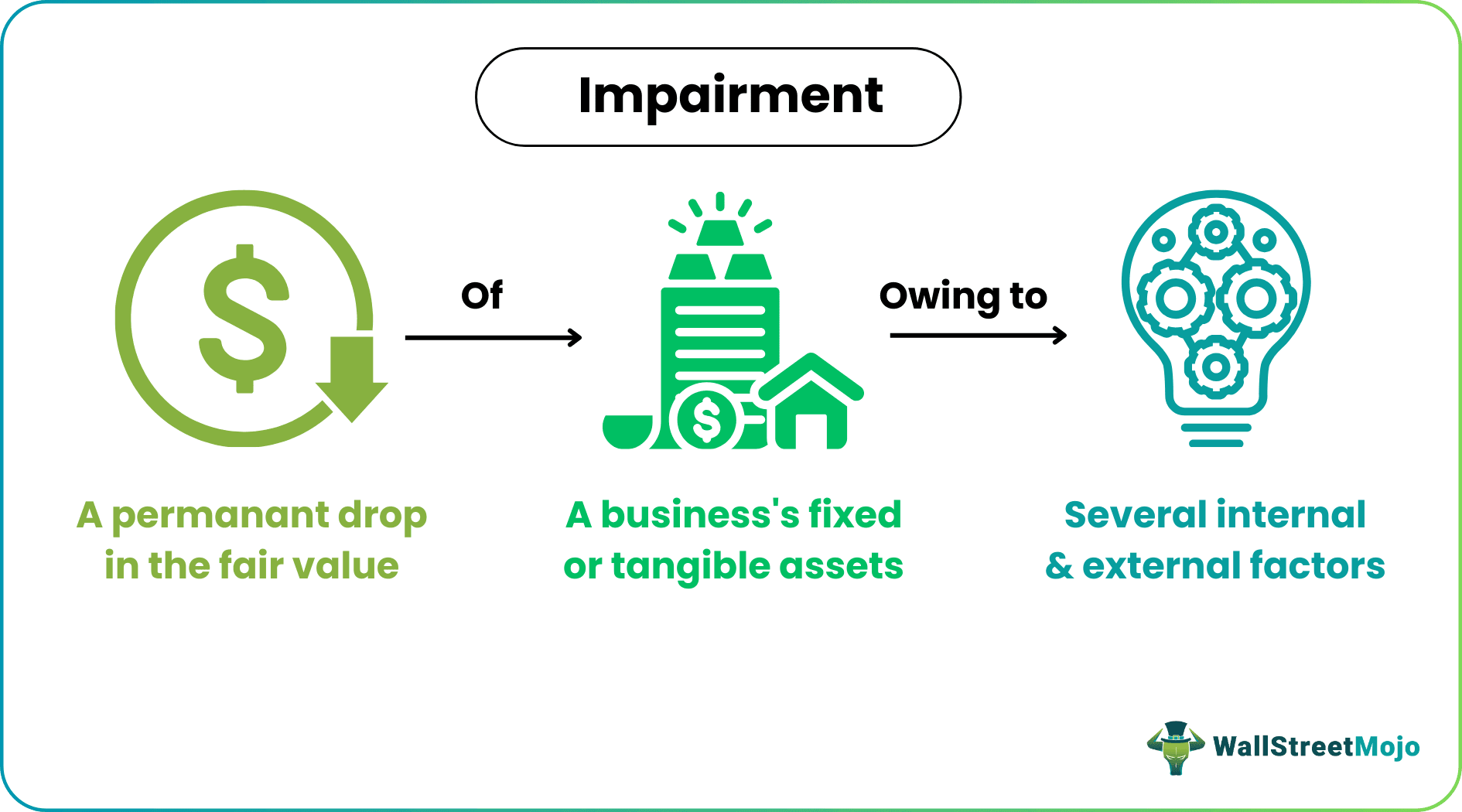

Impairment refers to the permanent decrease in the fair value of a company's intangible or fixed assets due to multiple factors, such as increased competition, physical damage, etc. It helps organizations evaluate their assets periodically, ensuring that they do not overstate the total value of the assets.

Accounting for the impairment of assets is crucial for companies because it offers an accurate picture of a business's financial position. When assets are impaired, a company's balance sheet must reflect the current value, not the historical cost. This gives investors a clear idea of the organization's actual worth. Impairment exists when an asset's carrying value exceeds its fair value.

Table of contents

- Impairment Meaning

- The impairment definition refers to a permanent fall in an asset's value. The asset may be an intangible asset or a fixed one.

- The decrease typically happens due to internal and external factors, like a change in the legal climate, increased competition, physical damage to the asset, etc.

- Impairment of assets from time to time prevents overstatement of the total value of assets on the balance sheet.

- There are various impairment benefits. For example, it alerts a company's investors and creditors of any potential risk associated with the business. Moreover, it helps investors and analysts assess a company's management.

Impairment In Accounting Explained

The impairment definition refers to a permanent fall in the value of a company's fixed or intangible asset for various reasons. If an asset's fair value drops and becomes lower than the book value, it becomes impaired per GAAP or the Generally Accepted Accounting Principles. For instance, if an infrastructure company's outdoor equipment gets damaged owing to a natural disaster, the assets' fair value will decrease significantly and fall below the book value.

When testing assets for impairment, businesses periodically compare the assets' overall cash flow, profit, and other benefits with their current book value. Companies write off the difference if an asset's book value exceeds the asset's future cash flow or other benefits. As a result, its value reduces on the balance sheet. Businesses can record instances of impairment from time to time to ensure they maintain accurate balance sheets.

Indicators

Businesses must evaluate the external and internal environment and look for the factors to determine when they should impair their assets. First, let us look at the internal and external indicators.

#1 - Internal Indicators

- Physical damage to an asset.

- Failure on the part of a company to bring in the post-merger synergy benefits.

- Economic underperformance.

- An asset lacks proper maintenance.

- Discontinued plans or restructuring of different operations involving an asset.

- An asset held for disposal.

#2 - External Indicators

- Drastic changes in the legal climate.

- Significant changes in the economic environment.

- A drop in an asset's market price.

- An asset's carrying amount is higher than the company's market capitalization.

- A technology change.

- Swelled up interest rates.

If companies can spot these signs in the middle of a financial year, they must test for impairment as soon as possible.

Examples

Let us look at a few impairment examples to understand the concept better.

Example #1

Suppose Tires And Automotive, a retailer of automotive servicing equipment, purchased new stock worth $150,000 in the last financial year. The value of the equipment decreased by $50,000 since the day of purchase, owing to depreciation. Per the company's latest balance sheet, the equipment's book value was $100,000. An earthquake hit the city, and the company's warehouse was seriously affected. Hence, Tires And Automotive decided to test the assets for impairment.

The business estimated the damaged equipment's value at $50,000. David, the organization's owner, decided to write off the impairment loss to avoid overstatement on the balance sheet.

Example #2

Ten years ago, BuildSmarter, a manufacturing company in Omaha, Nebraska, purchased a building at a historical cost of $180,000. According to the organization's latest balance sheet, this building's book value is $100,000. This means the accumulated depreciation stands at $80,000.

A tornado caused significant damage to the budling. As a result, BuildSmarter decided to test the asset for impairment. After evaluating the damages, the company determined the building's actual worth was $50,000. Hence, the managers decided to write down the asset value to prevent overstatement on the balance sheet. They made a debit entry to the 'Loss from Impairment' account. It appeared on the company's income statement as a net income reduction; the amount was $50,000 (book value – current fair value). A credit entry of $50,000 was also made to the building's asset account.

Benefits

Let us look at some noteworthy impairment benefits.

#1 - Helps Analysts And Investors

Impairment of assets provides analysts and investors multiple ways to evaluate an organization's decision-making track record and management. For example, this enables them to identify whether the managers responsible for writing down or writing off assets failed to make the right decisions owing to the abrupt drop in the value of an asset.

#2 - Alerts Creditors And Investors Of Potential Risks

An abrupt drop in the value of any asset informs companies' investors and creditors regarding business practices. If an organization writes off a lot of its assets to compensate for impairment losses, it is a common signal of poor business practices.

#3 - Improves Business Management

If businesses utilize impairment judiciously, they can turn the potential limitations from asset utilization into benefits and get investors' support.

Impairment vs Depreciation vs Amortization

If individuals do not clearly understand depreciation, impairment, and amortization, they are likely to prepare inaccurate financial statements. To eliminate any confusion regarding their meanings, they must understand their differences. Hence, let us look at the distinct features of these concepts.

| Impairment | Depreciation | Amortization |

|---|---|---|

| It is a permanent reduction in an asset's fair value. | An accounting technique involves distributing an asset's cost over its useful life. | This accounting technique involves periodically lowering an asset's book value over a certain duration. |

| This applies to both fixed and tangible assets. | It applies to fixed assets only. | Businesses use this accounting technique for only intangible assets. |

| It is not recurring in nature, unlike amortization and depreciation. | Depreciation is recurring in nature. | Like depreciation, amortization is recurring in nature. |

| Businesses can compute it by deducting an asset's fair market value and depreciation from the historical cost. | Businesses can compute depreciation using the straight line and written-down value methods. | Generally, businesses use the straight-line method to calculate amortization. |

Frequently Asked Questions (FAQs)

Businesses record this loss as an operating expense on their income statements. Hence, individuals can find impairment charges under the operating expense section of a corporate income statement.

According to federal income tax rules, businesses cannot claim tax deductions against impairment losses to reduce their income tax liability.

Impairments charges or losses are non-cash expenses; companies add them back into cash from operations. Therefore, such an expense could only change a business's cash flow in the case of a tax impact. However, that does not happen. This is because businesses cannot claim any tax benefit against such losses.

They record the loss as an expense on their income statement and simultaneously reduce the impaired asset's value on the balance sheet to ensure that the asset values are not overstated.

Recommended Articles

This has been a guide to Impairment and its meaning. We explain it with examples, indicators, comparison with depreciation and amortization, and benefits. You can learn more about finance from the following articles –