Table Of Contents

Home Equity Loan Calculator Explained

A home equity loan, also known as a second mortgage, is a type of loan that allows homeowners to borrow against the equity in their property. Equity is the difference between the current market value of the home and the outstanding balance on the mortgage.

Home equity loans provide homeowners with access to a lump sum of money, which they can use for various purposes, such as home improvements, debt consolidation, education expenses, or other major expenses.

One of the key advantages of free home equity loan calculators is its potential for lower interest rates compared to other types of loans, such as personal loans or credit cards. This is because home equity loans are secured by the value of the home, reducing the lender's risk. As a result, homeowners may be able to borrow larger amounts at more favorable interest rates, making home equity loans an attractive financing option for significant expenses.

Additionally, the interest paid on a home equity loan may be tax deductible, depending on the purpose of the loan and the borrower's circumstances. For example, interest on loans used for home improvements may be deductible. In contrast, interest on loans used for other purposes, such as debt consolidation or personal expenses, may not be deductible. It is always advisable for homeowners to consult with a tax advisor to understand the tax implications of a home equity loan.

However, homeowners must consider the risks associated with home equity loans. Since the home secures these loans, failure to repay the loan could result in foreclosure, putting the homeowner's property at risk. Additionally, borrowing against home equity reduces the homeowner's ownership stake in the property. It can increase overall debt levels, so careful consideration and financial planning are essential before taking out a home equity loan.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Formula

The home equity loan can be defined as the variance or difference between the current market value of the property and the outstanding loan balance taken against it. The formula is below:

Home Equity Value = MV - OP

Wherein,

- MV is the Market Value of the home or the property in question

- OP is the outstanding principal balance of the loan that was taken for the property

How to Calculate?

The following steps need are followed to determine home equity calculator payments.

First, determine the outstanding loan balance, which was taken specifically for the property in question.

Now, figure out the value of the property, which is nothing but the current market value of the property.

Now, subtract the value in step 2 from the value in step 1; the resulting figure would be the value of home equity.

Requirements

Let us understand the requirements that must be sorted from the borrower’s end to ensure they can get approved for a loan and calculate using a free home equity loan calculator.

- Sufficient Equity: Lenders typically require homeowners to have a significant amount of equity in their property, often at least 15% to 20% of the home's current market value. The amount of equity available determines the maximum loan amount that can be borrowed against the property.

- Stable Income and Creditworthiness: Homeowners are generally required to demonstrate stable income and a good credit history to qualify for a home equity loan. Lenders assess the borrower's ability to repay the loan based on factors such as employment history, income level, and credit score.

- Loan-to-Value Ratio: Lenders may impose a maximum loan-to-value (LTV) ratio, which limits the amount of the home's value that can be borrowed against. A lower LTV ratio indicates less risk for the lender and may result in more favorable loan terms for the borrower.

- Property Appraisal: Lenders typically require a professional appraisal of the property to determine its current market value. The appraisal helps ensure that the loan amount does not exceed the value of the property and provides security for the lender.

Examples

Let us understand the practicality of the concept through the examples below.

Example #1

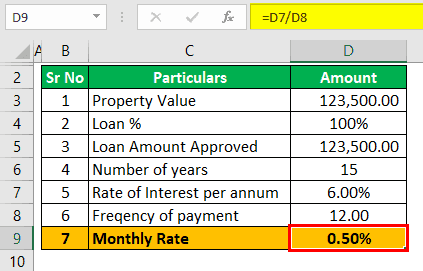

Since he had a good credit score, Mr. Kofi had purchased a house for $123,500 around five years ago, fully financed by the bank. The interest rate was 6%, the mortgage was for 15 years, and the current monthly installment he is paying is $1,042.16. The house measures 1000. Sq ft and the current market price of the property located in the same is $250 per Sq. Ft. Based on the given information, you are required to calculate the value of home equity.

Solution:

- As a first step, we shall calculate the outstanding mortgage balance for the property in question.

- Rate of interest applicable on monthly basis = 6.00% / 12 = 0.50%

- The remaining period will be (15 x 12) – (5 x 12), 180 – 60, that is, 120.

We need to calculate the present value of the current outstanding balance, which can be calculated per the below formula:

PV = P x

= $1,042.16 x

= $93,871.24

The outstanding debt on the property is $93,871.24.

Now we need to calculate the property's current market value, which we are given on a per sq ft basis. The value is $250 per sq. ft., and the total sq. ft. of the property is 1,000; hence, the current market value of the property is 1,000 x 250, which is $250,000.

Now, we can use the formula below to calculate the value of home equity

Home Equity Value = MV – OP

= 250,000 – 93,871.24

= 1,56,128.76

Since the value of the property has increased substantially and 1/3rd of the principal repayment is done, the owner is in a good position to repay the loan, and further, the worry of the lender would be less as the property value is more than the loan.

Example #2

Mr. JBL had recently met with a financial crunch and is already repaying the debt on his mortgage property for $1,231.66 when he got a loan for 95%, which was for $147,250, and the rate that was applied on the loan was 8%, and it was taken for 20 years period. He has not paid for ten years and has approached the bank to provide him with additional loans based on his home equity value. He has a requirement of $100,000, and the bank agrees to provide his loan for 85% of the home equity, which would be calculated. The property's value has increased by 30% since he last purchased it. Based on the given information, you are required to calculate whether the funds required by Mr. JBL would be financed fully by the bank or if he needs to resort to unsecured debt for any shortfall.

Solution:

- As a first step, we shall calculate the outstanding mortgage balance for the property in question.

- Rate of interest applicable on monthly basis = 8.00% / 12 = 0.67%

- The remaining period will be (20 x 12) – (10 x 12), which is 240 – 120, which is 120.

We need to calculate the present value of the current outstanding balance, which can be calculated per the below formula:

PV = P x

= $1,231.66 x

= $101,515.08

The outstanding debt on the property is $ 101,515.08.

Now we need to calculate the property's current market value, which we are given in % of the loan. A loan that was borrowed was $147,250, and it was financed by 95%. Therefore the property's value will be $147,250 / 95%, which will be $155,000, and since then, it has increased by 30%. Therefore, the current market value of the property is $155,000 x (1+30%), which is $201,500.

Now we can use the below formula to calculate the value of home equity

Home Equity Value = MV – OP

= 201,500 – 101,515.08

= 99,984.92

- Since the bank will finance only 85% of the home equity, which is 99,984.92 x 85%, that equals $84,987.19.

- There is a shortfall in the funds required by Mr. JBL, and hence Mr. JBL needs to borrow funds from outside as unsecured debt, which is 100,000 – 84,987.19, which is $15,012.81

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Home Equity Loan Calculator Vs HELOC

Let us understand the distinctions between a home equity loan calculator payment and HELOC through the comparison below.

Home Equity Loan

- Provides homeowners with a lump sum of money upfront, typically with a fixed interest rate and fixed monthly payments.

- Borrowers receive the full loan amount at closing and repay the loan over a set term, often ranging from 5 to 30 years.

- Interest is charged on the entire loan amount from the beginning, regardless of whether the funds are used immediately or over time.

- Home equity loans are suitable for one-time expenses or projects requiring a specific amount of funding upfront, such as home renovations or debt consolidation.

Home Equity Line of Credit (HELOC)

- Functions as a revolving line of credit, allowing homeowners to borrow against their home equity as needed, up to a predetermined credit limit.

- Borrowers can access funds as necessary, similar to a credit card, and only pay interest on the amount borrowed.

- Repayment terms vary but typically include a draw period, during which the borrower can access funds, followed by a repayment period, during which the borrower must repay the outstanding balance.

- HELOCs offer flexibility for ongoing expenses or projects with uncertain funding needs, such as home improvements or educational expenses.