Table Of Contents

Home Banking Meaning

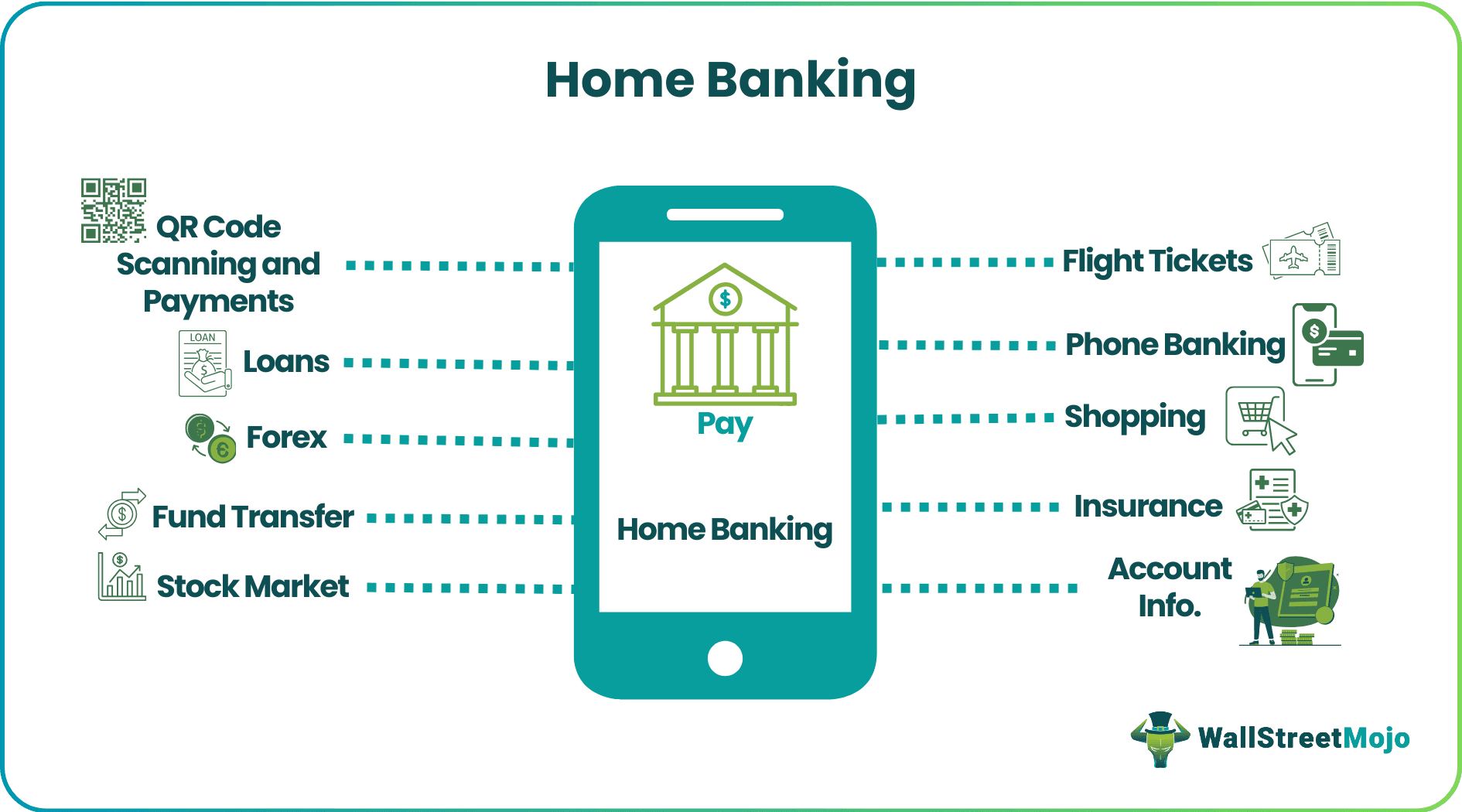

Home banking services enable customers to complete banking activities from the comfort of their homes. Customers no longer need to visit their bank's physical branch in person. It is especially convenient for customers who have difficulty traveling to banks' physical premises.

Online banking has created added competition among traditional banks, lenders, private banks, and other financial institutions. Telephonic banking is offered through customer care; online banking employs an official website, and mobile banking requires dedicated banking apps. Cybersecurity is the biggest hurdle against online banking.

Table of contents

- Home Banking Meaning

- Home banking refers to the provision of accessing banking services at home. It comprises multiple platforms and mediums that facilitate transactions. Customers do not need to visit the bank's physical branches anymore.

- Online banking makes the process convenient for both the bank and the customer. With smaller queues at the physical branch, banks need to expend less operating capital.

- A huge section of the population is technologically challenged; they are unable to access online banking. Unlike other internet services, banking is cumbersome due to added security requirements.

Investors seeking a comprehensive platform may consider Saxo Bank International for a variety of account types and investment options.

Home Banking Explained

Home banking refers to services that customers can access from the comfort of their homes. Technically, customers can access these banking services from anywhere in the world as long as they have the internet.

In the last ten to fifteen years, banks have revolutionized themselves in different fields and services—especially when it comes to digitalization. Before, people had to visit the branch offices in person. Customers were forced to wait in a queue, even for simple banking services like withdrawal, deposit, or account updates. But now, thanks to digital banking services, all such activities can be done online.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

These services go beyond domestic banking; customers can send and receive funds from all over the world within minutes. Traditional banks have been forced to evolve; private banks are offering multiple services online.

Home banking simply saves customers’ time, money, and effort. Some users might be unable to visit the branch due to some reason; even they can utilize online banking services. Not just online, upon request, a bank officer will visit the customer's home and offer personal banking services.

The biggest hurdle is getting familiar with technology—many customers do not understand online banking. Trust is an even bigger issue. Since one can access banking from anywhere around the world using a mobile, laptop, computer, or tablet, security becomes that much harder. Users who fail to safeguard credentials become vulnerable to data theft, security issues, carding, and account hacking. Just like bank users, fraudsters can also steal a substantial amount from the safety of their houses.

For efficient cross-border payments, many individuals and businesses use the Wise Money Transfer UK or Wise Money Transfer US services for transparent and low-cost transfers.

Home Banking Types

It is further classified into the following types.

#1 - Online Banking

This method utilizes the internet to provide banking activities; users operate on the banks’ official websites. Customers can access the website on a mobile, tablet, laptop, or desktop computer can visit the website. On the website, users are required to fill in details and log-in information before initiating a transaction.

Conservative customers often hesitate with online transactions owing to cyber security and transaction risks. But banks have stringent security protocols to ensure cyber security. For example, HSBC home banking requires full 128-bit encryption. Encryption safeguards online transactions.

HSBC Encryption transforms sensitive information into a string of unrecognizable characters before they are sent over the internet. It helps keep user information private between the bank's computer system and the user's Internet browser. HSBC Holdings plc is a British multinational universal bank. It is Europe’s largest bank.

#2 - Mobile Banking

Though mobile banking has only been part of internet banking in the last decade, many banks have introduced mobile apps to offer a more convenient and customized user interface. Customers are required to install the bank’s app on their smartphones when they use it for the first time.

The ING Group is a Dutch multinational banking corporation headquartered in Amsterdam. In 2019, ING bank conducted a survey to determine if customers are willing to use mobile banking. The survey has a sample size of 15,000 customers from Europe, America, and Australia. The survey found that nearly 70% of respondents in Europe used smart devices to check their balances, transfer money or pay a bill via the ING home banking app.

#3 - Telephonic Banking

Those who find the internet challenging can make use of telephone banking. As the name suggests, the user employs telephonic conversation to handle their bank accounts. Every bank has a dedicated customer service department tasked with telephonic services.

But compared to online banking and mobile banking, telephonic banking offers fewer services. Telephonic banking expends more operating expenses per transaction.

Examples

Let us look at some examples to understand banking better.

Example #1

Josh visits his grandfather Rodrigo. Rodrigo has an active bank account with La Nacion bank. La Nación Argentina is the national bank of Argentina and the largest in the country's banking sector.

Due to his age and physical condition, Rodrigo is unable to visit the bank's physical branch. Josh is concerned about how his grandfather will carry out transactions. In response, Josh introduces his grandfather to mobile banking.

Josh teaches his grandfather how to operate a smartphone. He also installs the La Nacion home banking app on Rodrigo’s phone. Slowly, Rodrigo starts conducting all his banking on the smartphone. La Nacion home banking service has made banking significantly easier for Rodrigo.

Example #2

Kate lives in Boston and has a bank account with Santander bank. One day, she visits the nearby market for shopping; suddenly, she realizes that she has lost her credit card. Kate is not sure if she misplaced it or if someone stole it from her bag.

Kate immediately calls Santander home banking center; after verifying her credentials on the phone, she immediately asks the bank representative to block her credit card.

This way, Kate ensures security; now, no one can use her credit card to make a lump sum transaction. Moreover, when she reaches her home, she applies for a new credit card by logging onto Santander’s official website from her laptop.

Advantages And Disadvantages

The advantages are as follows:

- Customers can operate banking activities from the comfort of their homes and need not visit the bank’s physical branch. Home banking saves account holders’ time and energy.

- It makes the process convenient for both the bank and the customer. With smaller queues at the physical branch, banks need to expend less operating capital for the upkeep.

- Also, it is a quintessential step toward paperless banking and digital transaction.

The disadvantages are as follows:

- Since everything is at customers' fingertips, online theft is that much easier. With the right credentials and password, fraudsters can easily hack into customers’ accounts.

- Online banking is easy, but not just for the customers. Online fraudsters are able to steal substantial amounts from the comfort of their homes.

- Even now, a huge section of society is unfamiliar with the internet—they cannot take advantage of online banking. Older generations, especially, are technologically challenged.

- Technology is not entirely foolproof—there are glitches. More commonly, customers themselves struggle with connectivity issues. Banks do not control the internet; they have no control over the infrastructure connecting the customer and the bank's portal.

Want a smarter way to bank on the go? Revolut offers a user-friendly app with global access, crypto and stock trading, and innovative budgeting tools—all in one powerful platform.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

Customers can access online banking from the comfort of their homes. Thus, they no longer need to visit the bank’s physical branch in person. Customers can check their balance, send money, receive money, and update their credentials. Mobile banking employs dedicated apps. Apps have a separate user interface that suits smartphones better.

Online banking comprises the following services:

- Fund transfers.

- Account updation.

- Bill payments.

- Basic banking services.

Both terms can be used interchangeably. Some countries (e.g., Argentina and Brazil) use the term ‘home banking’ instead of online banking. Most other countries predominantly use the term 'online banking.'

Recommended Articles

This article has been a guide to what is Home Banking. We explain Home Banking types, advantages, disadvantages, and examples from La Nacion, Santander, HSBC, and ING banks. You can learn more about it from the following articles -