Table Of Contents

Hedge Fund Strategies Explained

Hedge Funds do generate some outstanding compounded annual returns. However, these returns depend on your ability to properly apply Hedge Funds Strategies to get those handsome returns for your investors. While most hedge funds use Equity Strategy, others follow Relative Value, Macro Strategy, Event-Driven, etc. You can also master these hedge fund strategies by tracking the markets, investing, and learning continuously.

Hedge Funds Video Explanation

Types

The list of most common hedge fund strategies is given below:

- Long/Short Equity Strategy

- Market Neutral Strategy

- Merger Arbitrage Strategy

- Convertible Arbitrage Strategy

- Capital Structure Arbitrage Strategy

- Fixed-Income Arbitrage Strategy

- Event-Driven Strategy

- Global Macro Strategy

- Short Only Strategy

Let us discuss each of them in detail.

#1 - Long/Short Equity Strategy

- In this type of Hedge Fund Strategy, the Investment manager maintains long and short positions in equity and equity derivatives.

- Thus, the fund manager will purchase the stocks they feel are undervalued and Sell those who are overvalued.

- A wide variety of techniques are employed to arrive at an investment decision. It includes both quantitative and fundamental methods.

- Such a hedge fund strategy can be broadly diversified or narrowly focused on specific sectors.

- It can range broadly in terms of exposure, leverage, holding period, concentrations of market capitalization[, and valuations.

- The fund goes long and short in two competing companies in the same industry.

- But most managers do not hedge their entire long market value with short positions.

#2 - Market Neutral Strategy

- By contrast, in market-neutral strategies, hedge funds target zero net-market exposure, which means that shorts and longs have equal market value.

- In such a case, the managers generate their full return from stock selection.

- This strategy has a lower risk than the first strategy that we discussed, but at the same time, the expected returns are also lower.

#3 - Merger Arbitrage Strategy

- In such a hedge fund strategy, the stocks of two merging companies are simultaneously bought and sold to create a riskless profit.

- This particular hedge fund strategy looks at the risk that the merger deal will not close on time, or at all.

- Because of this small uncertainty, this is what happens:

- The target company’s stock will sell at a discount to the price that the combined entity will have when the merger is done.

- This difference is the arbitrageur’s profit.

- The merger arbitrageurs being approved and the time it will take to close the deal.

#4 - Convertible Arbitrage

- Hybrid securities including a combination of a bond with an equity option.

- A convertible arbitrage hedge fund typically includes long convertible bonds and short a proportion of the shares into which they convert.

- In simple terms, it includes a long position on bonds and short positions on common stock or shares.

- It attempts to exploit profits when there is a pricing error made in the conversion factor i.e.; it aims to capitalize on mispricing between a convertible bond and its underlying stock.

- If the convertible bond is cheap or if it is undervalued relative to the underlying stock, the arbitrageur will take a long position in the convertible bond and a short part in the stock.

- Conversely, if the convertible bond is overpriced relative to the underlying stock, the arbitrageur will take a short position in the convertible bond and a long position.

- In such a strategy, managers try to maintain a delta-neutral position so that the bond and stock positions offset each other as the market fluctuates.

- Delta Neutral Position - Strategy or Position due to which the value of the Portfolio remains unchanged when small changes occur in the importance of the underlying security.

- Convertible arbitrage generally thrives on volatility.

- The same is that the more the shares bounce, the more opportunities arise to adjust the delta-neutral hedge and book trading profits.

#5 - Capital Structure Arbitrage

- It is a strategy in which a firm’s undervalued security is bought, and its overvalued security is sold.

- Its objective is to profit from the pricing inefficiency in the issuing firm’s capital structure.

- It is a strategy used by many directional, quantitative, and market neutral credit hedge funds.

- It includes going long in one security in a company’s capital structure while at the same time going short in another security in that same company’s capital structure.

- For example, long the subordinate bonds and short the senior bonds, long equity, and short CDS.

#6 - Fixed-Income Arbitrage

- This particular Hedge fund strategy makes a profit from arbitrage opportunities in interest rate securities.

- Here opposing positions are assumed to take advantage of small price inconsistencies, limiting interest rate risk. The most common type of fixed-income arbitrage is swap-spread arbitrage.

- In swap-spread arbitrage, opposing long and short positions are taken in a swap and a Treasury bond.

- Point to note is that such strategies provide relatively small returns and can cause huge losses sometimes.

- Hence this particular Hedge Fund strategy is referred to as ‘Picking up nickels in front of a steamroller!’

#7 - Event-Driven

- In such a strategy, the investment Managers maintain positions in companies that are involved in mergers, restructuring, tender offers, shareholder buybacks, debt exchanges, security issuance, or other capital structure adjustments.

#8 - Global Macro

- This hedge fund strategy aims to profit from massive economic and political changes in various countries by focusing on bets on interest rates, sovereign bonds, and currencies.

- Investment managers analyze the economic variables and what impact they will have on the markets. Based on that, they develop investment strategies.

- Managers analyze how macroeconomic trends will affect interest rates, currencies, commodities, or equities worldwide and take positions in the asset class that is most sensitive in their views.

- A variety of techniques like systematic analysis, quantitative and fundamental approaches, long and short-term holding periods are applied in such cases.

- Managers usually prefer highly liquid instruments like futures and currency forwards for implementing this strategy.

#9 - Short Only

- Short sellingthat includes selling the shares that are anticipated to fall in value.

- To successfully implement this strategy, the fund managers have to write financial statements, talk to the suppliers or competitors to dig for any signs of trouble for that particular company.

Examples

Let us consider the following examples to understand different hedge fund strategies:

Example 1 (Long/Short Equity Strategy)

- If Tata Motors looks cheap relative to Hyundai, a trader might buy $100,000 worth of Tata Motors and short an equal value of Hyundai shares. The net market exposure is zero in such a case.

- But if Tata Motors does outperform Hyundai, the investor will make money no matter what happens to the overall market.

- Suppose Hyundai rises 20%, and Tata Motors rises 27%; the trader sells Tata Motors for $127,000, covers the Hyundai short for $120,000, and pockets $7,000.

- If Hyundai falls 30% and Tata Motors falls 23%, he sells Tata Motors for $77,000, covers the Hyundai short for $70,000, and still pockets $7,000.

- If the trader is wrong and Hyundai outperforms Tata Motors, however, he will lose money.

Example 2 (Market Neutral Strategy)

- A fund manager may go long in the ten biotech stocks expected to outperform and short the ten biotech stocks that may underperform.

- Therefore, in such a case, the gains and losses will offset each other despite how the actual market does.

- So even if the sector moves in any direction, the gain on the long stock is offset by a loss on the short.

Example 3 (Merger Arbitrage Strategy)

Consider these two companies– ABC Co. and XYZ Co.

- Suppose ABC Co is trading at $20 per share when XYZ Co. comes along and bids $30 per share, a 25% premium.

- The stock of ABC will jump up but will soon settle at some price, which is higher than $20 and less than $30 until the takeover deal is closed.

- Let’s say that the deal is expected to close at $30, and ABC stock is trading at $27.

- To seize this price-gap opportunity, a risk arbitrage would purchase ABC at $28, pay a commission, hold on to the shares, and eventually sell them for the agreed $30 acquisition price once the merger is closed.

- Thus the arbitrageur makes a profit of $2 per share, or a 4% gain, less the trading fees.

Example 4 (Convertible Arbitrage)

- Visions Co. decides to issue a 1-year bond that has a 5% coupon rate. So on the first day of trading, it has a par value of $1,000, and if you held it to maturity (1 year), you would have collected $50 of interest.

- The bond is convertible to 50 shares of Vision’s common shares whenever the bondholder desires to get them converted. The stock price at that time was $20.

- If Vision’s stock price rises to $25, the convertible bondholder could exercise their conversion privilege. They can now receive 50 shares of Vision’s stock.

- Fifty shares at $25 are worth $1250. So if the convertible bondholder bought the bond at issue ($1000), they have now made a profit of $250. If they decide that they want to sell the bond, they could command $1250 for the bond.

- But what if the stock price drops to $15? The conversion comes to $750 ($15 *50). If this happens, you could never exercise your right to convert to common shares. You can then collect the coupon payments and your original principal at maturity.

Example 5 (Capital Structure Arbitrage)

An example could be - A news of a particular company performing poorly.

In such a case, both its bond and stock prices are likely to fall heavily. But the stock price will fall by a greater degree for several reasons like:

- Stockholders are at a greater risk of losing out if the company is liquidated because of the priority claim of the bondholders.

- Dividends are likely to be reduced.

- The market for stocks is usually more liquid as it reacts to news more dramatically.

- Whereas on the other hand, annual bond payments are fixed.

- An intelligent fund manager will take advantage of the fact that the stocks will become comparatively much cheaper than the bonds.

Example 6 (Fixed-Income Arbitrage)

A Hedge fund has taken the following position: Long 1,000 2-year Municipal Bonds at $200.

- 1,000 x $200 = $200,000 of risk (unhedged)

- The Municipal bonds payout 6% annual interest rate – or 3% semi.

- Duration is two years, so you receive the principal after two years.

After your first year, the amount that you have made, assuming that you choose to reinvest the interest in a different asset, will be:

$200,000 x .06 = $12,000

After two years, you will have made $12000*2= $24,000.

But you are at risk the entire time of:

- The municipal bond is not being paid back.

- Not receiving your interest.

So you want to hedge this duration risk.

The Hedge Fund Manager Shorts Interest Rate Swaps for two companies that pay out a 6% annual interest rate (3% semi-annually) and are taxed at 5%.

$200,000 x .06 = $12,000 x (0.95) = $11,400

So for 2 years it will be: $11,400 x 2 = 22,800

Now, if this is what the Manager pays out, then we must subtract this from the interest made on the Municipal Bond: $24,000-$22,800 = $1,200

Thus $1200 is the profit made.

Example 7 (Event-Driven)

One example of an Event-driven strategy is distressed securities.

In this type of strategy, the hedge funds buy the debt of companies in financial distress or have already filed for bankruptcy.

If the company has yet not filed for bankruptcy, the Manager may sell short equity, betting the shares will fall when it does file.

Example 8 (Global Macro)

An excellent example of a Global Macro Strategy is George Soros shorting the pound sterling in 1992. He then took a massive short position of over $10 billion worth of pounds.

He consequently profited from the Bank of England’s reluctance to either raise its interest rates to levels comparable to those of other European Exchange Rate Mechanism countries or to float the currency.

Soros made 1.1 billion on this particular trade.

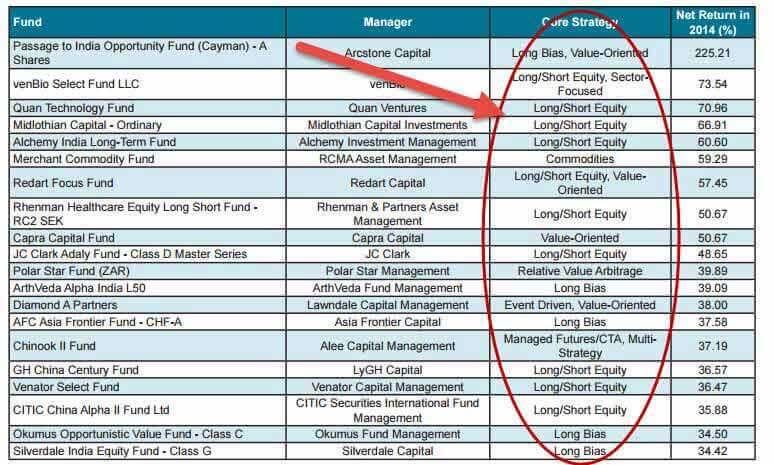

Top Hedge Fund Strategies of 2014

Below are the Top Hedge Funds of 2014 with their respective hedge fund strategies -

source: Prequin

source: Prequin

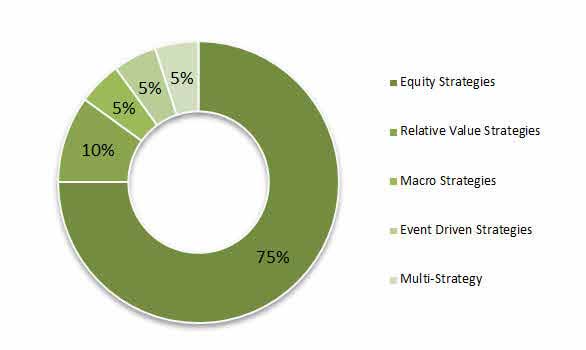

Also, note the hedge funds Strategy distribution of the Top 20 hedge funds compiled by Paquin.

source: Prequin

- Top hedge funds follow Equity Strategy, with 75% of the Top 20 funds tracking the same.

- Relative Value strategy is followed by 10% of the Top 20 Hedge Funds.

- Macro Strategy, Event-Driven, and Multi-Strategy make the remaining 15% of the strategy.

- Also, check out more information about Hedge Fund jobs here.

- Are Hedge Funds different from Investment Banks? - Check this investment banking vs hedge fund.

Frequently Asked Questions (FAQs)

Hedge fund strategies often differ from traditional investment strategies in flexibility, use of leverage, short-selling, and alternative investments. Hedge funds typically have more flexibility in employing various investment techniques and can take advantage of both long and short positions to profit in different market conditions.

Yes, hedge fund strategies can involve higher risks than traditional investment strategies. Hedge funds often employ more complex and sophisticated investment techniques, including leverage, derivatives, and short-selling, which can amplify both potential returns and risks. Additionally, hedge funds may have less regulatory oversight and may operate with less transparency compared to traditional investment vehicles.

Hedge funds are more suitable for sophisticated investors with a higher risk tolerance, a deep understanding of the strategies employed, and the ability to withstand potential losses.

Recommended Articles

A guide to what are Hedge Fund Strategies. Here we explain the types of it along with relevant examples and a list of top strategies. You can learn more about accounting and financing from the following articles –