Table Of Contents

Gross Earning Meaning

Gross earning refers to the total revenue generated by the company from the sale of its goods during a particular accounting period. It is obtained after deducting the cost of the goods sold but before the subtraction of the other expenses, taxes, and the adjustments incurred by the company during that period.

It is different from the company's taxable income, where the net income is calculated by deducting the indirect expenses from the gross earnings. Thus, the value of the gross earnings will never be less than the value of the company's net income.

Gross Earning Explained

The Gross Earning is the income the company generates after deducting the sum of the cost of the goods sold during a period from the total value of the revenue generated during the same period. It shows the performance of the company for the accounting year and the creditors, investors, and other stakeholders of the company to measure and analyze how efficiently and effectively the company can convert sales into income. The gross earnings during an accounting period are reported on the company’s statement of income for that period.

For the firms or companies, the gross earning is the total revenue after the cost of goods sold (COGS, including labor cost, shops’ inventory, manufacturing materials expenses, etc.) is deducted from the total amount generated from the sale of the goods and services. This becomes the money that, thereby helps business deal with the due liabilities.

The gross earnings in the case of an individual is the total income earned for a period before making any adjustments or deduction/taxation on the income. Gross income is the first line of a pay statement, from which the tax and other deductions, including insurance premiums and other expenses are deducted. After the deductions, the net earning is obtained that becomes the bottom line of the pay document. This amount is the usable income of the individual.

Though a gross earning is an important figure to calculate for entities, it does not act as an effective valuation metric to assess the financial status of the firm in the market. This is because there is a chance of COGS involved to be more than expected, thereby reducing the net earning, which is the ultimately usable amount for the companies. In short, net earnings are more reliable figures when it comes to helping the management and investors make better business and investment decisions.

Formula

The formula represents as follows:

Gross Earning = Total Revenue – Cost of Goods Sold

Where,

- Total Revenue = Income which any business entity generates by selling their different goods in the market or by providing their services to its customers during the normal course of the company's operations.

- Cost of Goods Sold = COGS is the sum of all direct costs related to the production of different types of the goods sold by the company and includes the cost of the raw material, cost of the direct labor and cost incurred on the other direct expenses.

Example

Let us consider the instance below to check how to calculate gross earnings of a firm:

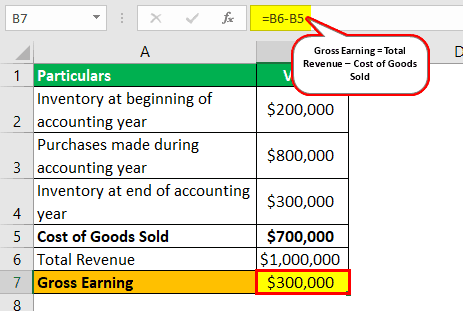

Company A ltd. has the details of the following transactions incurred during the accounting period ending on 31 December 2018.

The company earned a total revenue of $ 1,000,000 during the accounting period ending on 31 December 2018. On 1 January 2018, the company had an entire inventory of $ 200,000, and on 31 December 2018, the total value of its inventory was $ 300,000. Apart from this, the company made the total purchases worth $ 800,000 during the accounting period under consideration. Therefore, calculate the company's gross earnings at the end of the accounting period ending 31 December 2018.

Solution:

We calculate the company's gross earnings by subtracting the total value of the cost of goods sold during the period from the total value of the revenue generated during that period.

In the present case, to calculate the gross earnings of the company at the end of the accounting period ending on 31 December 2018, firstly, the total value of the cost of goods sold will be calculated as follows:

Cost of Goods Sold = $ 200,000 + $ 800,000 – $ 300,000 = $ 700,000

Now the gross earnings of the company for the accounting period ending on 31 December 2018 will be calculated using the below formula:

Gross Earning = Total Revenue – Cost of Goods Sold = $ 1,000,000– $ 700,000 = $ 300,000

Thus in the present case, the Gross earnings of the company A ltd. for the year ending on 31 December 2018 is $ 300,000.

Advantages

Calculating gross earning is one of the most significant steps for a business to be able to the identify the total sales on which the COGS is applied for subtraction for further deductions of due liabilities for obtaining the net earnings. Let us check the different advantages that these incomes offer to firms:

- It shows the company's performance for the accounting year and helps make the inter-company and intra-company comparison of the performance.

- The creditors, and investors, use the gross earnings value of the company and other stakeholders of the company to measure and make an analysis of how efficiently and effectively the company is capable of converting the sales into income.

- It is easy for the companies to calculate the period's gross earnings as it is calculated simply by deducting the cost of the goods sold value from the value of the total revenue generated by the company during the period.

Disadvantages

Besides the benefits, there are demerits of gross earnings, which one must be aware of. Let us have a look at them below:

- The calculation of gross earnings does not help in measuring the company's total profitability. To calculate the total profitability, we subtract all the direct and indirect costs from the revenue generated in the accounting period.

- To calculate the gross earnings, we use the inventory figures of the company. There are chances that the inventory figures are potentially inaccurate as accountants responsible for the inventory valuation might not have considered the adjustments in the inventory for the lost, damaged, or stolen value of the inventory. In that case, the value of the ending inventory will be overstated in the company's books of accounts.

Gross Earning vs Net Earning

Gross and net earnings are two important elements of the financial documents that a firm prepares. However, they differ from each other in multiple aspects. Let us have a look at them below:

- Gross earnings are the total income or revenue of the firm generated from sale of the goods and items. On the contrary, net earning is the real usable earnings of a business.

- The former is calculated by deducting COGS from the total amount obtained from the sales, while the latter is obtained by deducting all due liabilities, including taxes, from the gross earnings.

- Net earnings is used as aa more effective valuation metrics than the gross earnings. This is because the net revenue helps businesses know the actual income they are left with after they take care of all their additional expenses, taxes, etc. as this amount stays with the business and could be used for growth purposes further.