Table Of Contents

How Does A Grantor Trust Work?

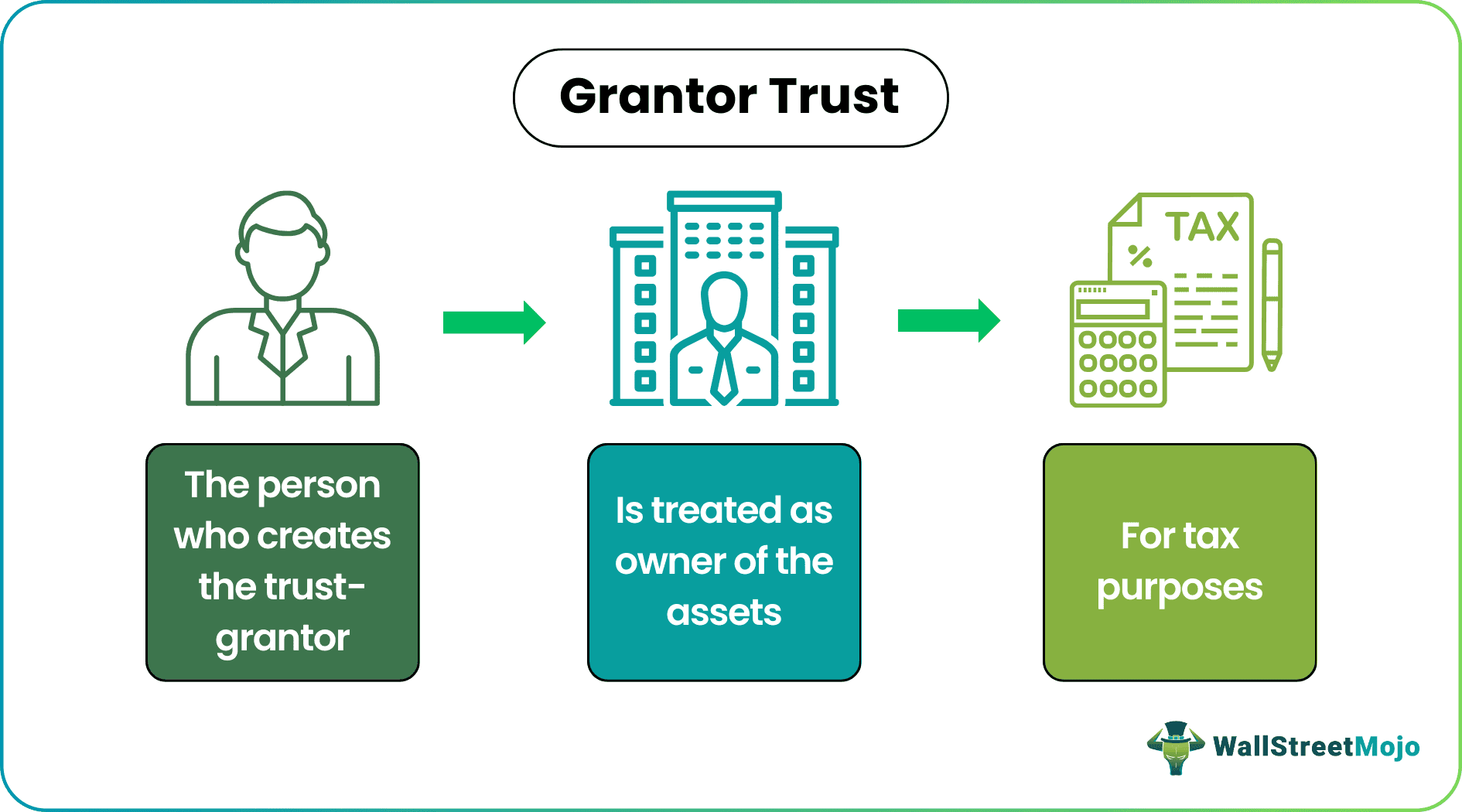

Grantor trust refers to a trust where the trust maker is treated as the owner of the trust assets for tax purposes. In addition, these are revocable (possibility of turning void) in nature. Therefore, foreign grantor trusts have a trustor who retains specific control or benefits over the trust's assets like domestic grantor trusts.

Moreover, it is vital in transferring assets to the beneficiaries. Thus, these grantor trust beneficiaries are entitled to receive income, principal, or other distributions from the trust according to the terms and conditions outlined in the trust document.

Here's a detail of how a grantor trust agreement works:

- Creation and funding of the trust: The process begins with the trustor creating a trust document. Later, the owner funds the trust. They typically transfer assets into the trust, including cash, real estate, investments, or other property.

- Grantor's control: These often serve as the initial trustee of the trust, retaining control over the trust's assets and management during their lifetime.

- Taxation: Taxing these trusts adds a heavy weight to the trust maker. The IRS (Internal Revenue Service) has defined specific trust rules. According to them, the tax will be imposed on the beneficiary rather than the trust for any income earned.

- Probate avoidance: Avoiding the probate process is one of the main goals of this trust. The trust's assets are dispersed to the named beneficiaries without going through the probate process after the grantor dies.

- Beneficiaries: The trust document designates the beneficiaries entitled to receive the trust's assets and income.

- Privacy: These trusts offer privacy because the details of the trust, including its assets and beneficiaries, are generally not made public, unlike the probate process, which becomes part of the public record.

Types

Let us look at the types of these trusts that currently exist in the market:

#1 - Revocable Living Trust

These are among the primary or most common types of trusts. Here, they control and manage the trust assets. However, they still have the right to revoke the trust anytime they wish.

#2 - Qualified Personal Residence Trust (QPRT)

QPRT is a widespread trust that helps the trustor transfer the primary or secondary estate to the trust without taxes. A qualified personal residence trust is a savior when a large estate is involved.

#3 - Grantor Retained Annuity Trust (GRAT)

In GRAT, the settlor can take advantage of these trust rules. Here, they can easily withdraw income from the trust. The trustee receives an annuity payment once the assets are transferred to the trust. In the end, the rest of the assets are given to beneficiaries. The grantor temporarily freezes the asset's value. As a result, there is no addition to asset value, which offers minimal estate to beneficiaries.

#4 - Intentionally Defective Grantor Trust (IDGT)

It is a form of irrevocable trust that appoints the trustor as the owner of the trust temporarily. The intention is to gain some income tax benefits. However, the grantor will still pay the estate taxes.

Examples

Let us look at some examples of these trusts for a better understanding of the concept:

Example #1

Let's say, John, a successful business owner, decided to establish these trusts to simplify the eventual transfer of his assets to his children while maintaining control over them during his lifetime. Therefore, he created "The John Smith Revocable Living Trust." In the trust agreement, John identified himself as the trust maker and trustee, retaining the authority to amend, revoke, and manage the trust assets. He transferred his primary residence, investment accounts, and a family vacation property into the trust, specifying his children as primary beneficiaries.

Moreover, the trust document outlined that income from his investments should be distributed to him during his lifetime, with the principal to be distributed to his children upon his passing. By setting up this trust, John aimed to avoid probate, protect his family's privacy, and facilitate the seamless transition of his wealth to the next generation while maintaining control and flexibility during his lifetime.

Example #2

According to recent IRS guidelines (Rev. Rul. 2023-2), property acquired from a decedent retained in a grantor trust after the grantor's death is not eligible for a basis adjustment under Section 1014.

Depending on the details and circumstances, the trustor's estate may or may not include the trust assets. There are two categories of trusts for this decision:

- Traditional grantor trusts are those included in the grantor's estate for estate tax purposes.

- Occasionally referred to as intentionally flawed grantor trusts (IDGTs), grantor trusts that are not a part of the grantor's estate.

Benefits

These trusts provide various benefits to the grantor as well as the beneficiary. Let us look at them:

#1 - Changing The Terms Or Beneficiaries

These trusts get an opportunity to change the name of the beneficiary. As a result, if an individual wants to appoint another person as heir, they can do it quickly.

#2 - Tax Protection

In contrast to other institutions, these trusts have a significant tax advantage. Here, the tax rate for the trust is the same as individual rates. For instance, if the trust earns income, the rate applicable will be the same as the grantor's rate. As a result, it provides a certain level of protection to the trust.

#3 - Incapacity Planning

These often include provisions for managing assets if the grantor becomes incapacitated due to illness or disability.

#4 - Power To Change Or Revoke

They provide a lot of flexibility to the trustees. They can change their status from revocable to irrevocable or vice versa. Here, the trustee can destroy the trust only if the grantor is mentally incompetent to make decisions. Likewise, if they change their status to irrevocable, the taxation method also changes. At that point, the trust must report its income and require a separate tax identification number.

Grantor Trust vs Non-Grantor Trust

Although grantor and non-grantor trusts involve the management of assets, they have distinctions. So, let us look at the differences between them for a better understanding:

| Aspect | Grantor Trust | Non-Grantor Trust |

|---|---|---|

| Meaning | It refers to a trust involving a grantor that handles the assets of the individuals. Later, it is passed on to the beneficiary. | A non-grantor trust is a trust that must pay taxes using its TIN (tax identification number). |

| Purpose | To earn tax benefits using the grantor's tax rate on earned income. | The main aim is to impose no control over the grantor. |

| Also known as | Revocable Trust | Irrevocable Trust |

| Trust assets | They can reclaim assets from the trust. | Here, trusts impose no restrictions on the assets. |

| Grantor’s Role | Moreover, the grantor acts on behalf of the trust to manage the assets of the entire entity. | There must be another person appointed as grantor. They cannot be the same. |

| Tax treatment | Furthermore, here, the trust does not need a separate TIN. They can file on the tax rate applicable to the grantor. | It is mandatory to have a TIN and pay taxes in the name of the trust. |

| Impose of Estate tax | In this trust, it is necessary to pay estate tax to the IRS. | Non-grantor trusts do not need to pay estate tax. |

Frequently Asked Questions (FAQs)

Yes, these trusts are considered disregarded entities in the United States for federal income tax purposes. Therefore, this means that, for tax purposes, the trust itself is not a separate taxable entity, and instead, the grantor is treated as the owner of the trust assets. Hence, they do not file a tax return or pay taxes on their earnings.

Yes, it can have two grantors, and this type of trust is commonly referred to as a "joint grantor trust" or "spousal grantor trust." In a joint grantor trust, both individuals contribute assets and are considered grantors for tax purposes.

These trusts are not required to distribute income to beneficiaries. Moreover, these are known for providing flexibility when managing and distributing revenue generated by the trust's assets. Whether or not payment is allocated depends on the terms outlined in the trust document and the preferences of the grantor.

Recommended Articles

This article has been a guide to what is Grantor Trust. Here, we compare it with non-grantor trust and explain its benefits, examples, and types. You may also find some useful articles here -