Table Of Contents

What is Fund Accounting?

Fund accounting is a method used by non-profit organizations and governments for the accountability of funds or grants received from individuals, grant authorities, governments or other organizations, etc. who has imposed restriction or conditions on the utilization of the funds from the grants (condition could be implemented on full funds or part of the funds as per the donor).

It provides accountability of the recorded funds and transactions against it with the statutory obligations applicable to the entities and helps the auditors by providing traceability towards the different funds or grants received from the donors and the transaction or expenditure incurred by the management against those funds.

Fund Accounting Explained

Fund accounting jobs involve separating accountability for the general-purpose fund and specific-purpose fund, enabling the traceability of the amount. It tracks the expenditure that incurs out of funds and if the usage is in such a field was against those funds (conditions provided by donor).

The process is used to evaluate the financial condition of the entity & to show reliable financial information regarding the entity for financial reporting. It provides a justified basis for the expenditure incurred against the specific purpose grant received for any capital projects.

In the case of non-profit organizations (NPO) & governments, the financial reporting rules and requirements are different from those of other organizations as these entities are not profit-oriented. Hence the main focus is to track and validate the various uses of the funds available to the entity. The NPOs receive two types of funds, one is the grant with no restriction for its use, and the other is with some limitation to the usage of the funds. Therefore, it is used for the accountability of these funds.

Hence, it provides the bifurcation in the treatment of both types of grants and provides traceability to the usage of funds having donor-specific restrictions or conditions.

Characteristics

Fund accounting, particularly nonprofit fund accounting, provides essential accounting methods for non-profit organizations and governments to record their funds and grants received from other parties (any grant – general purpose or specific purpose grant). Besides the fund accounting meaning, the features, too, need to be explored. Some of them have been listed below:

- Non-profit organizations or government organizations use it. It records resources received from a donor for a specific purpose. There can be two types of funds one is restricted, and the other is unrestricted. The restricted fund is used for a particular purpose, but unrestricted funds can be used for any purpose or general purpose.

- The non-profit organization uses the same standard as a profit organization uses. Still, terms are different in non-profit organizations. Instead of preparing a profit and loss account, NPO makes payment and receipt accounts, revenue and expenses account and balance sheets.

- Payment and receipt account- All the Amount receipts in an organization, would be accounted for on the receipt side, and all the payments done will be shown on the payment side.

- Revenue and expenses account- Non-profit organization prepares revenue and expenditure accounts to show the use of funds they have received and the allocation of the fund. If income received is more than expenses incurred, then it is called an excess, and if expenses are more than income, then it is called a deficit.

- A balance sheet of a statement of financial position - the balance sheet of the non-profit organization is the same as a profit organization. It shows the value of assets and liability of an NPO.

Examples

The examples below provide more clarity to the fund accounting basics, thereby helping to understand its advanced aspects. Let us have a look at them:

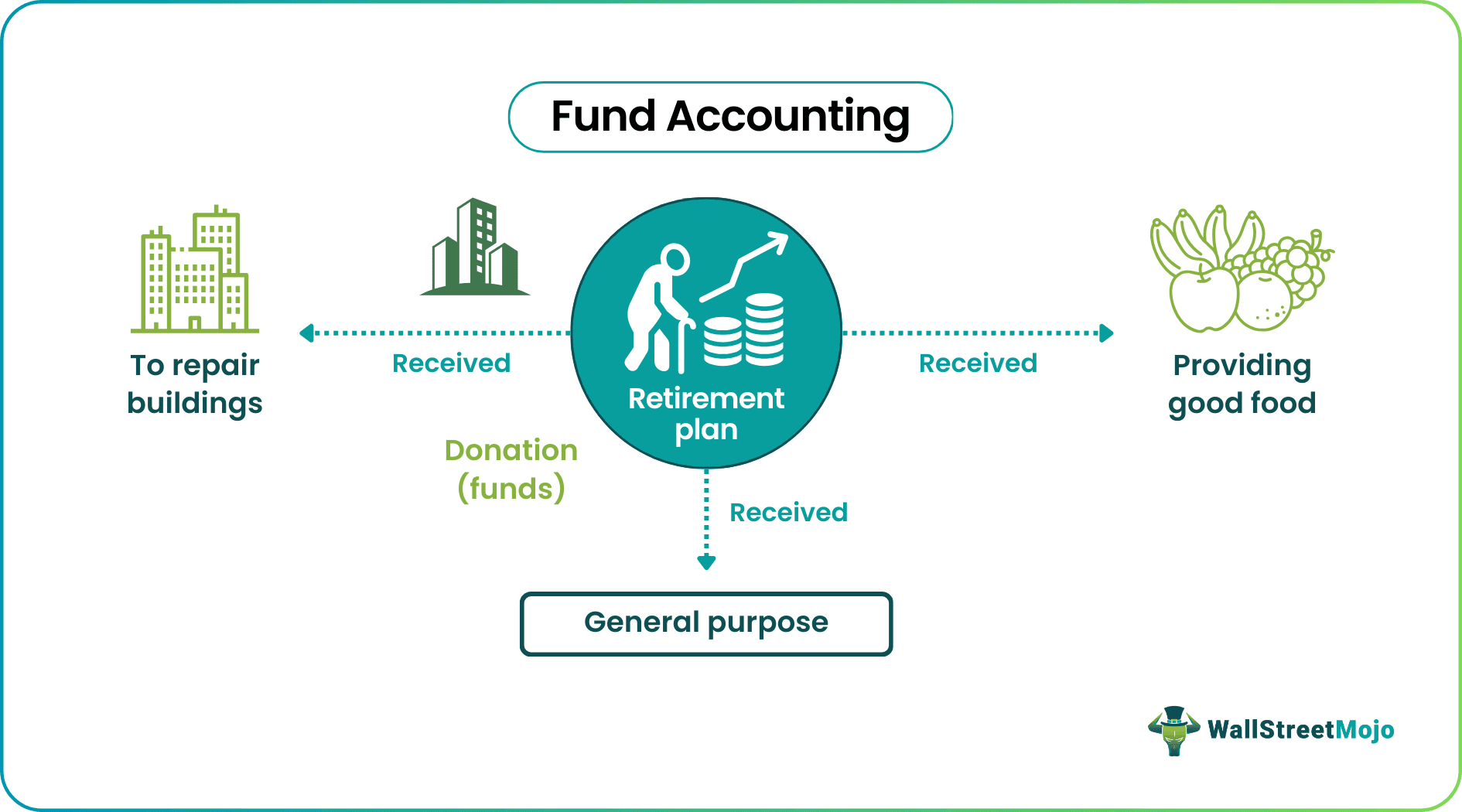

- A school is working as a non-profit organization. It has received a donation for the repair of the building. Also, they received funds from a company to provide good food to students. Schools also received a donation for general-purpose means, not for any specific purpose.

- Now donations for repair will be used only for building repair. Till the expense does not occur, that donation will be kept aside. The donation received for food will be spent for that purpose only. But donations received for general purposes can be used for any purpose, like the salary of teachers, expenses of school, etc.

Advantages

- It separates specific-purpose funds from general-purpose funds.

- It segregated funds depending on the purpose of the fund provided by law or the donor when giving a grant. Dividing funds help in budgeting and projection of funds for future purposes.

- This requires preparing a receipt and payment account showing how much was collected in a year or a specific period and how much was paid in a particular period, and how much amount still remains in a fund.

Disadvantages

- Maintaining the amount in separate funds makes it difficult to separate the amount from the general fund to a specific purpose fund.

- The account doesn’t reflect the actual value of the fund. Sometimes no-profit organizations misappropriated the fund by including the use of cash.

- Sometimes it leads to excess spending but lower control of the fund; mostly, it happens in government organizations.

- The fund accounting does not provide a qualitative analysis of the performance of NPO or government entities. It only focuses on the accounting of the different funds.

- With the increase in types of grants or funds and management of different accountability, the accounting and tracking of the funds eventually become too complicated.

Fund Accounting Vs Non-Fund Accounting

The difference between fund accounting and non fund accounting are:

- Non-profit organizations and the government use fund accounting. It is also used by portfolio businesses and in the investment banking business.

- Non-fund-based accounting does not deal with funds or cash. It deals with bonds, letters of credit, etc.

- In fund accounting, specific funds can be used to receive them. A general-purpose fund can be used for the administration of an organization.

- In a Non-fund organization, the business entity is treated as a separate business.

- The financial statement includes the payment and receipt account, income and expenditure, and balance sheet.

- Financial statements of non-fund accounting include trading account, profit and loss account, and balance sheet.

Recommended Articles

This has been a guide to what is Fund Accounting. Here we explain it with examples, advantages, characteristics, vs non fund accounting, and disadvantages. You can learn more about Financing from the following articles -