Table Of Contents

What Is The Full Form of SLR?

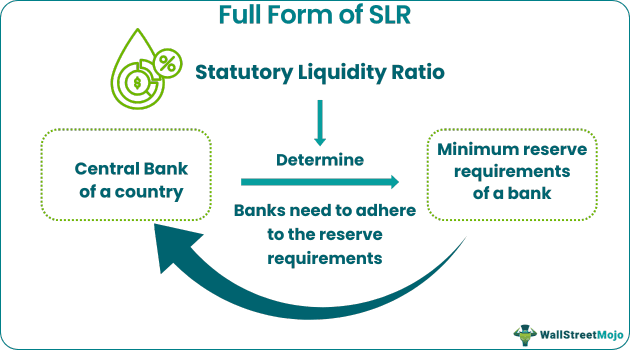

The full form of SLR is the Statutory Liquidity Ratio. It is the ratio of the bank’s liquid assets to the net demand and time liabilities it owes. The liquid assets are cash, gold, and other marketable securities. The statutory liquidity ratio is the rational basis on which the Central Bank determines the minimum reserve requirements a bank aligned under it should meet.

The term statutory means that the bank is legally and mandatorily required to adhere to the Central Bank’s reserve requirements. The ratio ensures that the bank can service the demands of the deposit holders if the holder liquidates the deposits that it had given to the commercial bank. If commercial banks fail to comply with the Statutory Liquidity Ratio, they have to bear fines and penalties for not complying as imposed by the central banks.

Table of contents

Full Form Of SLR Explained

The full form of SLR in banking is Statutory Liquidity Ratio. As per the regulations of the central bank of a country, it is mandatory for the banks to keep a certain part of their own assets aside and not lending them out. Such assets can be in the form of liquid assets, government securities, cash, etc.

It is a very important tool that central banks use while playing the role of financial regulator to ensure that the financial system of the country is stable. It also prevents sudden and unusual credit expansion in the system.

The full form of SLR in banking, which is Statutory Liquidity Ratio has to be maintained by all the commercial banks reporting to the central banks. The central banks regularly review the country's economic situation and modify the statutory liquidity ratio accordingly. If the Central Bank raises the SLR, it means that the Central Bank wants the commercial bank to limit the availability of the bank limit.

Thus, in the above manner, the banks face a restriction on their ability to lend out funds to borrowers, be it corporates, small businesses, or individuals. The rules ensure that the financial system does not have excess funds that may lead to a fall in the price of goods and services, resulting in instability. Thus, the flow of cash is well regulated to ensure solvency and a stable financial system.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Objectives

The following are some of the objectives of the concept, in details.

- The central bank mandates commercial banks to maintain demand deposits and liquid assets in the independent vault.

- The ratio helps in establishing the monetary policy for the nation.

- The Central Bank establishes this ratio between 40 percent for the upper cap and 23 percent for the lower cap.

- The ratio is instrumental in restricting the commercial banks from liquidating their assets beyond a specified threshold.

- If the ratio is unset or established, the banks or the financial institutions may resort to over-liquidating assets and could, in turn, jeopardize their financial health.

- The SLR ratio helps in establishing and controlling the bank credit. The Central Bank would modify the ratio when there is a marked change in inflation.

- When there is a rise in inflation, the bank raises the SLR ratio, which in turn, restricts the bank credit.

- When there is a recession in the economy, the bank reduces the SLR ratio, which raises the bank's credit.

CRR Vs SLR Explanation in Video

Components

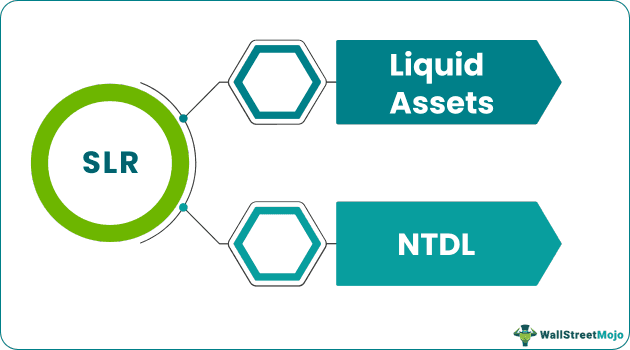

The statutory ratio has two broad components, namely: -

#1 - Liquid Asset

These assets can liquidate within 1 to 2 days into cash. Such assets normally consist of cash equivalents, gold, treasury bills, government bonds, and marketable securities.

#2 - Net Time and Demand Liabilities

These are deposits that the banks or financial institutions accept from the banks. The banks are liable to pay such entities on demand. The NTDL comprises demand drafts, overdue fixed deposits, demand drafts, and saving deposits, along with time deposits having varying maturities. The depositors of the time deposits cannot liquidate their deposits until they reach maturity. If such deposits are liquidated before maturity, the bank levies penalties on such withdrawals on the deposit holders.

How Does SLR Work?

The following are the basic steps of maintaining the ratio in the banks. Let us study the same in detail.

- Financial intermediaries and market participants govern the financial system of the nation. The central bank is the financial institution or intermediary with exclusive rights to produce and distribute funds across different parts of the nation. They get exclusive rights from the governments of the nation. In India, the Reserve bank of India portrays the role of a Central Bank. Whereas, for the US, the Federal Bank portrays the role.

- Commercial banks operate in different parts of the nation and report to the Central Banks. The Central Bank monitors and supervises the performance of the commercial banks aligned to it. In addition, the Central Bank establishes a statutory liquidity ratio to ensure compliance and performance standards among commercial banks.

- The bank has to hold certain cash and gold percentages to meet the net demand and time-based liabilities. The Central Bank establishes this ratio, and all the commercial banks aligned to it have to comply with the set ratio. If the ratio appreciates, the bank narrows money flow into the economy. The statutory liquidity ratio helps govern the monetary policy and ensures that the commercial banks are solvent.

How To Calculate?

Below is the formula for calculating the Statutory Liquidity Ratio which is the full form of SLR in economics : –

Here,

- A liquid asset represents LA.

- Net time-based and demand liabilities represent NTDL.

Examples

Let us understand the concept with the help of a suitable example.

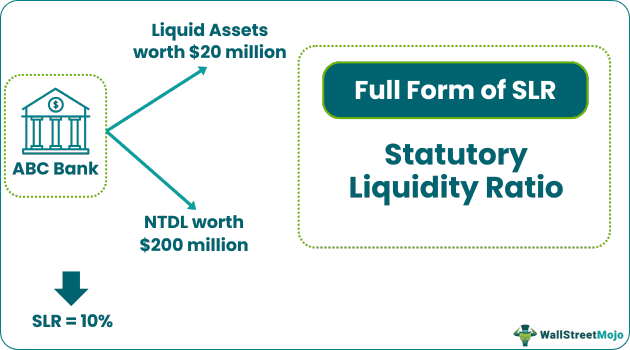

Let us take the example of ABC Bank. The bank holds liquid assets worth $20 million. On the other hand, the bank has NTDL or net time and demands liabilities worth $200 million. Help the management of ABC bank on the determination of the statutory liquidity ratio.

Determine the SLR ratio as displayed below: -

- = $20,000,000 / $200,000,000

- = 20 / 200

- = 1 /10

- = 0.1

Statutory liquidity Ratio = 10 %.

Therefore, the bank has an SLR ratio of 10%.

The above is a simple example of identifying banks' data to calculate it. However, this example explains the concept in a very simplified manner. In contrast, the actual scenario may involve various other complex data and processes used during calculation to implement the same.

Impact

- The impact of SLR is immense as it regulates the flow of funds in the economy and fixes the base rate. The Central Bank below establishes the base rate, in which the commercial banks forbid lending funds to the borrowers. The base rate, therefore, promotes transparency in the lending and borrowing business.

- The Statutory Liquidity Ratio, which is the full form of SLR in economics, ensures that some portion of deposits would always remain safe. One would readily provide it to the deposit holders if they redeem the deposits in the event of failure of the financial system. To ensure the SLR remains competitive, the bank has to report its net time and demand liabilities fortnightly.

- Suppose the commercial banks aligned under the purview of the Central Banks fail to comply with the Statutory Liquidity Ratio. In that case, the commercial bank must pay a fine of three percent annually over and above the bank rate to the Central Bank. Additionally, any defaults on the immediate working day result in a 5 percent penalty on the commercial banks.

Thus, the above are some important impacts that the concept has in the banking system of a country. It can be said that the ratio acts as a guide or reference for the central bank to understand what should be the base rate. To summarise, the banks can use this ratio to decide the part of their liquid asset that they should keep aside. This will ensure the ability to meet short term financial needs and obligations as well as achieve the basic economic objective.

SLR Vs CRR

Both the above are two different ratios that are considered as important part of monetary policy. However, both are different in many ways. Let us try to understand the differences as given below.

- The CRR stands for the cash reserve ratio.

- The cash reserve ratio only focuses on the cash and cash equivalents that the commercial banks maintain with the central banks.

- The statutory liquidity ratio comprises cash, gold, and treasury securities that the commercial bank has to maintain with the central banks.

- The statutory liquidity ratio focuses on the commercial bank’s ability to extend credit to borrowers.

- The Cash Reserve Ratio focuses on the Central Bank's ability to extend credit to commercial banks. Hence, the Central Bank controls the money supply in the commercial banking system with the help of CRR.

- Commercial banks earn interest on liquid assets kept with the Central Bank to comply with the SLR guidelines. In contrast, commercial banks never earn interest on cash reserves maintained with the Central Bank.

- The Cash Reserve Ratio monitors the flow of money in the economy, whereas the Statutory Liquidity Ratio helps commercial banks meet the holders of deposits' demands.

Thus, the above are clear differentiations between the two concepts. It is important to understand them in detail so as to interpret the policies used by policymakers in the country and identify the reasons behind them.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Recommended Articles

This article guide to what is the Full Form Of SLR (Statutory Liquidity Ratio). We explain the objectives, components, how it works & how to calculate. You may refer to the following articles to learn more about finance: -