Table Of Contents

What Is A Free Cash Flow (FCF)?

Free Cash Flow (FCF) is the cash flow to the firm or equity after all the debt and other obligations are paid off. It measures how much cash a company generates after accounting for its required working capital and capital expenditures (CapEx).

FCF is different from cash flow, which indicates the total inflow of cash from different business activities. While the cash flow is the revenue generated by a company, free cash flow is the amount that helps evaluate its current value.

Key Takeaways

- Free Cash Flow (FCF) represents the cash available to a company after satisfying its debt and other obligations.

- It accounts for working capital and capital expenditures (CapEx) to determine the company's remaining cash.

- Two types of FCF are Free Cash Flow to the Firm (FCFF) and Free Cash Flow to Equity (FCFE).

- FCF enables Discounted Cash Flow analysis, providing a valuation framework for determining the value of the firm or its common equity.

- It considers the time value of money and provides insights into the company's intrinsic worth.

Free Cash Flow Explained

It is a measurement of a company's financial performance and health. The more FCF a company has, the better it is. It is an economic term that truly determines what is available to distribute among the company's security holders. So, FCF can be a tremendously useful measure for understanding the true profitability of any business. It is harder to manipulate, and it can tell a much better story of a company than more commonly used metrics like profit after tax.

FCF is a portion of cash that remains in the hands of a company after paying all its capital expenditures like purchasing new machinery, equipment, land & building, etc. and satisfying all its working capital needs like accounts payables. Therefore, FCF is calculated from the cash flow statement of the company. A business that generates a significant amount of cash after an assured interval is considered the best business than other similar businesses. Since you have to pay all your routine bills like salary, rent, and office expenses in cash, you cannot bear it from your net income. Thus, its business's ability to generate some money matters to stakeholders, especially those who are warier about the liquidity of the company than its profitability like business suppliers. Therefore a company with sound working capital management provides strong and sustainable liquid signals, and FCF is on top.

Hence, in corporate finance, most projects are selected based on their timing of cash inflows and outflows rather than their net income. Because the income statement includes all cash and non-cash expenditures like depreciation and amortization, these non-cash expenditures are not the actual outflow of money for that particular period.

To gain the best industry knowledge regarding Financial Modeling and Valuation, dive into the course of WallStreetMojo and become an expert in collection, analysis and projection of valuable financial data of companies across sectors. This course will help candidates navigate through the complex financial jargons and arrive at robust and reliable projections for the future through self-paced learning.

Video Explanation Of Cash Flow

Types

FCF is of two types: Free Cash Flow To Firm and Free Cash Flow To Equity.

#1 - Free Cash Flow to the Firm (FCFF)

FCFF means the ability of the business to generate cash, netting all its capital expenditures. One can calculate the FCFF by using cash flow from operations or by using the company's net income. The formulas to calculate Free Cash Flow to the Firm (FCFF): -

To learn more about FCFF, you may look at this detailed article FCFF

#2 - Free Cash Flow To Equity (FCFE)

FCFE is a cash flow available for equity shareholders of the company. The amount shows how much cash can be distributed to the company's equity shareholders as dividends or stock buybacks after all expenses, reinvestments, and debt repayments are taken care of. The FCFE is also called the levered free cash flow. The formula to calculate free cash flow to equity is: -

To learn more about free cash flow to equity, you may look at this detailed article Free Cash flow to Equity

Formula

Below is the simple free cash flow formula: -

How To Calculate?

Below is the series of steps to help understand the FCF calculation using examples:

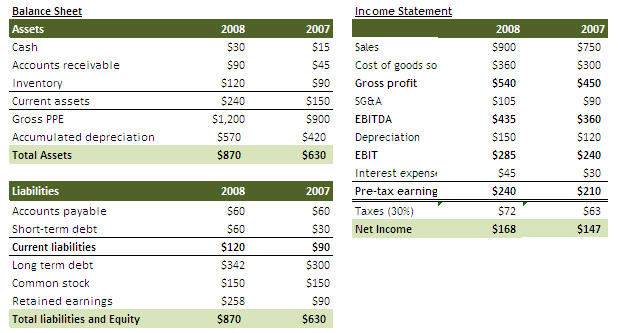

Calculate FCF for the year of 2008

Step 1 - Cash Flow from Operations

Cash flow from operations is the total of net income and non-cash expenses like depreciation and amortization. Please note this change in the working capital could be positive or negative.

Therefore, cash flow from Operations = Net Income + Non Cash Expenses +(-) Changes in working capital.

Step 2 - Find the Non Cash Expense

The non-cash expenses include depreciation and amortization. Here, in the income statement, we have only depreciation figures provided. Therefore, we will assume that amortization is zero.

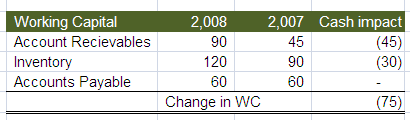

Step 3 - Calculate Changes in working capital

We see from above, changes in working capital = Accounts receivables (2007) – Accounts receivables (2008) + Inventory (2007) – Inventory (2008) + Accounts Payable (2008) – Accounts Payable (2007)

Changes in working capital = 45 – 90 + 90 – 120 + 60 – 60

Changes in working capital = -75.

It means that there has been a cash outflow of -$75 due to changes in working capital.

Here is a snapshot of how the calculations look like within the model and how the data has been populated in the easiest possible way to help candidates understand the process in details.

Step 4 - Find out the Capital Expenditure

Since we are not provided with the cash flow statement, we will use the balance sheet and the income statement to derive these figures. There are two ways to calculate capital expenditure -

Gross PPE Approach -

Capital Expenditure = Change in Gross property plant and equipment (Gross PPE) = Gross PPE (2009) - Gross PPE (2007) = $1200 - $900 = $300

Please note that this is a cash outflow of - $300

Net PPE Approach

CapEx = Change in Net PPE + Depreciation & Amortization = Net PPE 2008 – Net PPE 2007 + Depreciation and Amortization

= (1200-570) - (900-420) + $150 = 630 - 480 + 150 = $300

Please note that this is a cash outflow of - $300

Step 5 - Combine all the above components in FCF Formula

We can combine the individual elements to find a long FCF formula and calculate free cash flow.

The FCF Formula = Net Income + Depreciation and Amortization +(-) Accounts receivables (2007) – Accounts receivables (2008) + Inventory (2007) – Inventory (2008) + Accounts Payable (2008) – Accounts Payable (2007) – (Net PPE 2008 – Net PPE 2007 + Depreciation and Amortization)

So, FCF calculation will be: -

= $168 + $150 – $75 – $300

= -$57.

Importance

A company can expand, develop new products, pay dividends, reduce its debts or seek any possible business opportunities for the time being necessary for its expansion only if it comprises adequate FCF. So, it is often desirable for businesses to hold more FCF to boost the company's growth. However, the reverse of that is not always necessarily true. A company with a low FCF might have made considerable investments in its current capital expenditures, which will benefit the company to grow in the long run.

There are reasons that indicate why free cash flow is important. Some of them have been mentioned below:

- Investors like to invest in several small businesses with steady and predictable growth in their free cash flows. Their probabilities of making a return on their investments will increase with the development of the companies.

- The analysts are more concerned about cash inflows generated by the Company's operating activities as it purely predicts its actual performance. Operating cash flow only includes cash generated by the company's core business. It ignores the influence of abnormal gains or losses/expenditures like liquidating the undertaking of the company or lagging suppliers' payment and many other strategies of similar nature to record cash flow in one period sooner or later.

- FCF can provide a useful Discounted Cash Flow analysis technique that can derive the value of a free cash flow firm or the value of the firm's common equity.

- Many people use FCF as a substitute for earnings when valuing mature businesses. Like price-to-earnings ratios, price-to-free-cash-flow ratios can help value a business. To calculate a price-to-free-cash-flow ratio, one can divide the share price by the free cash flow per share or the market cap of a company divided by its total free cash flow.

- The Free Cash Flow Yield is an overall return evaluation ratio of a stock, determining the FCF per share a company is expected to earn against its market price per share. The ratio is calculated by dividing the FCF per share by the share price.

- Generally, the higher the ratio, the better it is. And many people prefer free cash flow yield as a valuation metric over earnings yield.

In short, FCF is just another metric. It does not tell you everything, nor will it be used for every kind of company. But observing that there is a very big difference between income and FCF will almost certainly make you a better investor.