How Fintech Startups Are Disrupting Traditional Banking

Table Of Contents

Introduction

Over these decades, technological advancements have accelerated daily business operations and streamlined the related processes effectively, especially in the banking and financial services sector. They have transformed and shifted from the traditional methods to the digital age in no time. Imagine no waiting time, long queues, endless paperwork, or high fees. With an online application and a single click, you can open your account and access services as and when required. All thanks to the fintech startups coming up with tech-savvy features for ruling this space. One of the key enablers of this transformation is a Fintech Software Development Company, which builds secure, scalable, and user-friendly digital solutions for financial institutions. These companies play a crucial role in developing next-gen banking applications, AI-powered fraud detection systems, and seamless payment gateways that enhance customer experiences.

You are free to use this image on your website, templates, etc.. Please provide us with an attribution link.

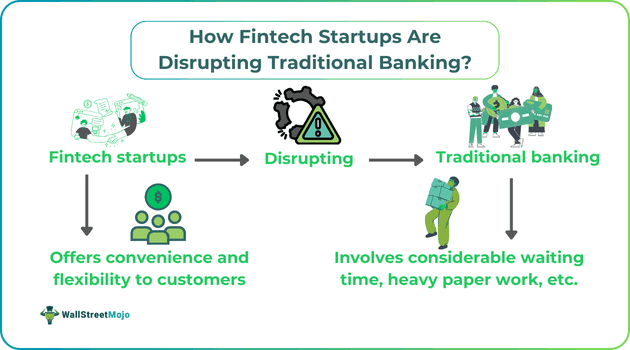

Fintech startups have revolutionized the way of managing finances, offering convenience, and transforming the age-old techniques of servicing customers. But ever wondered how they have been gradually disrupting the traditional banking sector over these years? Keep reading to explore how the rise of fintech startups has affected the traditional banking system.

Key Takeaways

- Fintech startups are a hybrid model of traditional banks and technological solutions. They harness the potential of both models and cater to customer needs.

- Technologies like AI, blockchain, IoS, security, and cloud solutions have contributed to its growth.

- Other potential key drivers for its growth include digital adoption, neobanks, AI and decentralized solutions, changing customer demands, increasing fintech investments, and the COVID-19 pandemic.

- Many banks like Silvergate Capital, Signature Bank, JPMorgan Chase, and Citi Group have already incorporated fintech solutions into their existing space.

The Rise Of Fintech Startups

Fintech startups are companies that harness the power of technology to provide financial services or products or revolutionize the traditional products already offered. Technically speaking, when some enthusiasts combine financial services with technology, this combo is referred to as financial technology or Fintech. Today, around 29,955 fintech startups are operating globally, and it has been the fastest-growing space, with projected growth of $917.17 billion by 2032 and a compounded annual growth rate (CAGR) of 16.82%.

The revolution of fintech 1.0 started in the 19th century when electronic fund transfer systems like telegraph and Morse code were used to deliver financial services. Slowly, this advancement allowed popular banks like Barclays to develop automated teller machines (ATMs) for easy fund access. In the 1970s, the well-known digital stock index NASDAQ and a communication protocol for large-volume cross-border payments were introduced through the Society For Worldwide Interbank Financial Telecommunications (SWIFT). Since then, fintech innovation kept rising, paving the way for online banking and business operations in the 1980s. However, exploring the real timeline of digital banking started in the 1990s with the entry of PayPal in 1998. This move had already hinted towards the rising graph of fintech startups and everything going digital.

At this moment, the internet era had already begun. Every possible business was leveraging online banking systems. However, the unexpected turmoil of the 2008 financial crisis signaled a new regulatory mode for financial institutions. That is when the Fintech 3.0 version drove the lost trust in banks with the birth of Bitcoin, Artificial Intelligence (AI), and neobanks. Also, this era was a boon for many startups to rise, not just finance but others as well. Nevertheless, the McKinsey report also suggests that the revenues of the fintech industry will grow thrice more than the traditional banks between 2023 and 2028. Flevy and Invensis Technologies are a few firms that have leveraged technology to streamline documentation and accounting processes.

Key Drivers Of Fintech Growth

Growth never happens alone. There are supporting actors that drive the performance throughout the years. In the case of fintech startups, some key factors have contributed to their growth. Let us look at them:

#1 - Digital adoption

Digital innovation in finance has created a new mode of connectivity, accessibility, and flexibility for customers. In this online realm, everyone has stepped into the digital space and made it a part of their lifestyle. Most customers are turning tech-savvy, definitely surging the demand for digital banking services. For example, you can easily open your account and complete the Know Your Customer (KYC) formalities without visiting the bank. Additionally, it has also boosted financial literacy among customers.

#2 - Neobanks

A proving factor for fintech growth is neobanks that own no physical branch but collaborate with well-established banks to provide digitalized services to customers. The best part is, you have synergies of both entities together.

#3 - AI and decentralized banking

Since the 2008 financial crisis, customers developed huge trust issues in the financial system. Hence, banks and major fintech firms started deploying blockchain and decentralized solutions for improved decision-making and customer experiences.

#4 - Changing customer’s needs and expectations

Evolving lifestyles and busy schedules have forced financial institutions to change their products and services. People expect to enjoy online services and banks seriously implement ways to fully meet customer needs. As a result, in today’s times, many fintech and insurtech companies have streamlined their operations online.

#5 - Covid-19 pandemic

Covid-19 was a major factor that led to a huge revolution in the finance industry. This pandemic caused a traditional to digital banking transformation. For instance, the rising surge of healthcare services made the insurance companies turn to digital and innovative solutions.

#6 - Increasing investments in fintech space

The global fintech investments rose between 2010 and 2019, staying high at $216.8 billion. Many venture capitalists (VCs), private equity firms, and High net individuals (HNIs) believed in the true power of Fintech and fueled innovation so that startups could scale globally, thereby disrupting the traditional banking system.

How Fintech Startups Disrupt Traditional Banking?

Precisely, the above reasons have been a contributing factor in the rise of these startups. But the need for technological intervention is the system has been the major cause. Most banks adopted a digital approach to bring an online platform to address the customer’s needs. It also comes with a user-friendly interface that makes navigating and locating the services easy. Additionally, to pamper customers, the fintech startup solutions are available 24/7, so you can use them anytime and anywhere. For instance, ATMs, mobile banking, and peer-to-peer payment systems allow seemingly easy deposit, withdrawal, and transfer of funds from one account to another.

Moreover, with AI-powered insights, fintech companies can analyze customer data and safeguard and utilize it for their needs. Here, utilization means using the data to develop future products with a sprinkle of personalization. You do not have to stick to the traditional products, but have one that best suits your requirements.

Here is a glimpse of what experts have to say:

- "Disruption doesn’t spell the end of traditional banking; instead, it marks the dawn of an opportunity for reinvention. The challenges posed by fintech innovations and changing consumer expectations are not threats but catalysts for evolution. By embracing new technologies and rethinking customer-centric strategies, traditional banks can transform themselves into more agile, efficient, and relevant institutions in the modern financial landscape,” - Anupa Rongala, CEO of Invensis Technologies.

- "Fintech startups have revolutionized the lending industry by streamlining processes and expanding accessibility. They’ve demonstrated that creditworthiness goes beyond a simple credit score, incorporating innovative methods to evaluate borrowers and ensure financial inclusion for underserved communities." — David Tang, Founder of Flevy.

Technologies Driving Fintech Disruption

Among all technologies, BASIC holds the responsibility to disrupt the fintech space. It refers to Blockchain, AI, Security, the Internet of Things (IoT) and the Cloud. Think of it as a powerhouse of the industry that has caused a dynamic shift since its origin. In contrast, AI solutions act as a tool for customization purposes. This collected data can be stored in the cloud for product development. Interestingly, with AI, entities can understand their customer’s expectations better and tailor financial products accordingly.

Also, many fintech and insurtech companies have successfully claimed the benefit of AI in fraud detection and automated trade activities. For instance, telematics and IoS devices (using chipboards from providers like FlexiPCB) can track customers’ health and prevent events before occurrence.

Here is a glimpse of what experts have to say:

- "The smartphone has become the new bank branch, revolutionizing how people access and manage their finances. Fintech startups are harnessing their power to redefine financial services, offering seamless, on-the-go solutions that prioritize convenience, accessibility, and user experience." — Paul Posea, Outreach Specialist at Superside.

- "The future of banking lies in collaboration, where fintech agility meets the stability of traditional banks." — Jay Barton, CEO of ASRV.

Challenges Faced By Traditional Banks

Apart from the endless benefits provided by fintech solutions, there are certain challenges faced by this industry. A few of them have been listed below:

- Increasing competition and undue pressure from the already existing fintech startups.

- Banks must adopt digital technologies to retain customers and prevent them from switching to fintech providers.

- Insufficient knowledge of trending technologies or quick adoption can create cybersecurity risks for the banks. Also, customer’s data and funds are at stake.

- A huge flow of funds as an investment in technologies to meet customers' rising expectations.

- There can be regulatory compliance like anti-money laundering (AML) laws to avoid data theft and fraudulent activities from occurring.

Partnerships Between Banks And Fintechs

Today, many traditional banks partner with fintech startups and companies to benefit from synergies. Neobanks are one of the finest examples of this collaboration. As a customer, you can access digital banking services, deposit funds, and various investment incentives through a single bank application. At the backend, the fintech company integrates its solutions on the bank’s platform. It can happen for payment systems, operations, and enhanced application programming interface (API) infrastructure. Fintech companies like Stripe, BitPay, Dodo Payments, Coinbase, and banks like Silvergate Capital, Signature Bank, JPMorgan Chase, and Citi Group are already a part of this collaboration.

A Gartner report suggests that, on average, each bank is found to partner with almost 9.4 fintech companies. Why? This is because they can cater to multiple customers, access new markets, and enhance digital offerings. But more interesting is that 60% of the banks partner with fintechs to create custom solutions that leverage technology to its best potential. It is very similar to apparel brands like ASRV, which integrate technology into their clothes to give customers the best and most comforting experience.

Conclusion

As Matthew Holland, Head of Marketing at FlexiPCB, aptly stated, "Disruption is not the end of traditional banking; it’s an opportunity for reinvention." The rise of fintech companies has created a huge disruption for the entire economy, not just traditional banks. By leveraging technology and providing customized solutions, easy accessibility, and greater convenience, the fintech space has seen a huge surge in its business. All this has been possible with innovative technologies like AI, blockchain, Security, the Internet of Things (IoT) and the Cloud. It has allowed us to rely on the fintech firms and enjoy their financial products and services. Take this guide as a lens to witness this ongoing evolution as the upcoming future holds many more surprises. Stay calm, as the future of Fintech is way more digital.