Although financial literacy is a part of financial capability, they differ as follows:

Table Of Contents

Financial Capability Definition

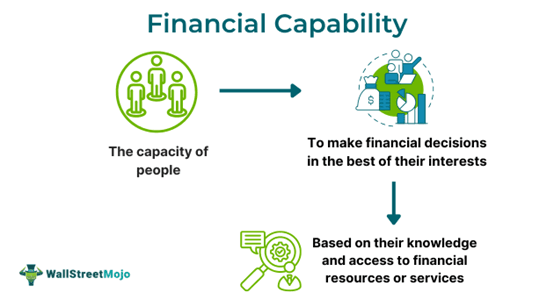

Financial Capability refers to an individual's internal potential to ensure financial inclusion in the prevailing environmental and socioeconomic conditions. It focuses on nurturing consumer abilities, knowledge, skills, attitudes, and behavior to help them learn, manage resources effectively, and access financial services to fulfill their requirements.

Building financial capability is vital for people's well-being and success in achieving financial freedom and accumulating wealth in the long run. Financial discipline and consumers' accessibility to financial systems can change the destiny of these individuals and their families by spreading awareness on effective money management, debt reduction, budgeting, savings, and investments.

Key Takeaways

- Financial capability is a field of consumer finance that concentrates on raising the financial literacy among a nation's population and their access to financial services and resources in a given social, economic, and environmental scenario.

- It emphasizes on developing the financial knowledge, attitude, behavior, abilities, and skills of the consumers to ensure financial inclusion.

- Background factors, attitudes, normative influences, skills and knowledge, and perceived behavioral control are some key contributors to such internal potential.

- Such efforts are essential for future financial planning, resilience, money management, wealth creation, financial security, and the nation's overall economic stability.

Financial Capability Explained

Financial capability program forms part of consumer finance that emphasizes the financial resilience of consumers in the current environmental and socioeconomic scenario. It aims to offer them both financial literacy and access by fostering knowledge, abilities, behavior, skills, and attitudes for greater financial inclusion. It aims to promote the financial health and well-being of the individuals living in a country while inculcating a fine sense of money management in them. It ensures not only a disciplined financial approach where no current financial needs are overlooked but also a secured future after retirement.

This internal capacity of consumers to handle their personal finances becomes even more essential during tough times like divorce, medical conditions, joblessness, or raising a baby. When citizens become financially independent, the nation witnesses a more stable economy. However, governments are more focused on enhancing financial literacy among GenZ to make the youth of the nation financially aware and resilient.

Some of the characteristics of a financially capable individual are as follows:

- Believes in future planning and savings

- Effectively handles everyday expenses

- Values every penny

- Invests money for long-term

- Keeps aside emergency funds for unforeseen events

- Sensibly uses credit while avoiding debts

- Makes financial decisions confidently

Factors

There are following five broad categories, drawn from the Theory of Planned Behavior (TPB), into which the various determinants affecting the consumers' financial capabilities fall:

- Background Factors: Financial literacy, which is the core of financial capability, can be achieved through higher education, such as a college degree, parental education, parents' financial habits and behavior, gender, urban living, and employment.

- Normative Influence: Another critical group of factors is the normative impacts, such as social pressure and the influence of friends, family, spouse, financial mentors, and society on financial decisions.

- Attitudes: Consumer attitudes toward money matters. These include materialism, a short-term approach, financial disregard, and other negative perspectives, which can disrupt financial inclusion goals. However, zeal for self-actualization and wealth-building can serve as positive milestones in this journey.

- Perceived Behavioral Control: Consumer behaviors such as self-confidence, optimism, and determination to change their financial situation can help them attain financial discipline.

- Skills and Knowledge: Consumers' basic research and numeracy skills can help them plan their budgets, savings, investments, and debts. Moreover, setting financial goals for the future and post-retirement planning can also strengthen consumers' financial capacity.

Examples

The financial capacity model has developed over the years and transfers from generation to generation. For a deeper understanding of this phenomenon, let us explore the following instances:

Example #1

Suppose Mr. and Mrs. Maxwell are graduates of Science and Commerce, respectively. Both are financially literate and have strong knowledge of investments, budgeting, savings, and debt management. They believe in investing 25% of their income in their future financial goals and contributing 10% of it towards their retirement savings plan. They have also passed on their financial knowledge, behavior, abilities, skills, and attitudes to their children. Thus, the whole family believes in financial empowerment and inclusion, which ensures the enhancement of their financial capabilities at every stage and generation.

Example #2

A crypto news report published on April 19, 2024, emphasized cryptocurrency education. It specified that the number of Americans investing in cryptocurrencies has surged to 93 million, making financial education necessary for citizens. The report mentioned some of the sources working to enhance the financial capabilities of not only Americans but also citizens around the world.

For instance, Sparrow Finance is actively promoting Bitcoins among women through community engagement. Similarly, Coinbase has launched an advertising campaign to explain complex crypto concepts to a broader audience. Meanwhile, BlackRock has created a series of educational videos on Bitcoin literacy.

Internationally, initiatives like Bitget's Blockchain4Youth project conduct educational events for students, and Tether's partnership in the Middle East fosters understanding of digital assets among financial institutions. However, many challenges remain, including the fast pace of the crypto industry evolution and confidence and knowledge issues that block the widespread adoption and use of these digital currencies.

How To Measure?

There are multiple ways in which the financial capabilities of a nation can be assessed. The most popular among them is conducting surveys and gathering data for further analysis and assessment. However, the most talked-about tool that currently helps gauge financial capabilities is the Financial Capability Barometer (FCB). It keeps a check on whether:

- Policymakers promote financial literacy;

- Policy implementors tailor the initiatives of financial awareness;

- National Strategy for Financial Education (NSFE) Steering Committees analyze the financial capacities and track progress; and

- The public is capable of monitoring the NSFE efforts and holding such institutions accountable for their actions.

The FCB is a comprehensive framework that comprises different aspects, such as thematic areas, survey methodology, competency matrix, and scoring modules. Although this model was primarily designed for Armenia, it can be modified to be more adaptable to the NSFEs of other nations.

There are seven critical thematic areas considered by organizations like the World Bank and OECD/INFE for ensuring greater financial literacy:

- Budget Management

- Economic Impact

- Savings and Long-term Planning

- Shopping Around

- Debt Management

- Rights Protection, and

- Safety

Moreover, a Financial Capability Competency Matrix can effectively demonstrate the required knowledge, attitudes, skills, and behaviors for every thematic area, serving as the basis of the financial capability survey.

Importance

A solid financial capacity can not only benefit the consumers but also the nation. Let us see some of its significant contributions:

- Future Financial Planning: A financially aware individual can plan their future financial requirements and goals efficiently, whether it is retirement, further education, owning a house, marriage, emergency needs, or any other potential expenses.

- Financial Security: An effective money management practice provides a sense of financial protection for any expense, whether sudden or planned, thus reducing people's financial stress.

- Reduced Debt: Individuals like students or low-income groups need not rely upon student loans, payday loans, credit cards, personal loans, or any other borrowing methods to fulfill their financial needs when they have well-organized finances.

- Wealth Creation: The financial capability theory further helps to build wealth in the long run, providing financial freedom to consumers when they retire from their jobs.

- Informed Investment Decisions: This is the backbone of sensible investment decision-making when choosing assets like equities, bonds, mutual funds, retirement plans, etc., based on individuals' risk, return, and investment objectives.

- Positive Economic Impact: When consumers become financially literate and explore different financial services to improve their living standards, the overall economy progresses due to greater financial inclusion.

Financial Capability vs Financial Literacy

| Basis | Financial Capability | Financial Literacy |

|---|---|---|

| 1. Definition | Financial capability is the art of knowing and applying financial concepts in real life to achieve financial inclusion and informed decision-making. | Financial literacy is the theoretical learning of different financial fundamentals, such as budgeting, investing, saving, and debt management. |

| 2. Objective | Secure financial literacy and accessibility by bringing such knowledge, skills, abilities, behavior, and attitude into actions | Gain knowledge on financial services, products, or fundamentals |

| 3. Emphasizes On | Financial health of the consumers by developing financial abilities, knowledge, skills, attitude, and behavior | Understanding of savings, budgeting, debt management, and investing |

| 4. Scope | Broader scope, covering the learning and implementation of financial fundamentals in real life | Limited to the know-how of theoretical financial concepts |

| 5. Examples | Consistently investing in retirement plans and mutual funds for future financial security and wealth accumulation. | Know about different types of investments like equities, bonds, mutual funds, ETFs, and retirement plans. |

Frequently Asked Questions (FAQs)

1

What does a financial capability worker do?

2

What is financial capability month?

3