Examples of Financial Asset

A Financial Asset, also known as financial instruments or securities, is not a physical asset but is part of the intangible asset of an entity. They derive their value from the contractual claim. It can be readily and easily converted to cash. Some are bank balance, shares, short-term investments, treasury bills, etc.

It is usually represented as a certificate, receipts, or another legal document. Financial assets are often created by or related to the lending of money. They are widely used to finance real estate and the ownership of tangible assets.

List of Financial Assets Examples

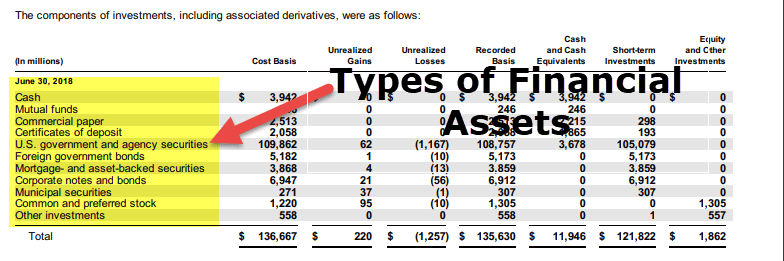

source: Microsoft SEC Filings

Below is the list of Financial Asset Types and examples –

- Cash or cash equivalent like a bank balance,

- Equity instruments of another entity. It is the shareholder/investors’ claim for the company’s ownership.

- Bond: this is a claim upon interest payments and principal in the future. It could be a financial asset for companies like a bank or a liability for companies.

- Loan: In the above example, we have taken a bond as a financial asset. Likewise, loans are treated as a financial asset for companies like banks where the sale of such loans brings assets.

- Insurance: the worth of financial assets pays out if the terms of the contract are met. Like if a company pays a premium for its car and car break downs, then the financial asset will pay off.

- Legal & contractual right so that the entity can receive cash from other entity

- A financial asset like securities for a loan from another entity

- Under favorable conditions, the entity has the right to exchange financial assets or liabilities with other entities. Such rights are financial assets for the entity.

- Any contract that may be settled with equity instruments of the entity,

- Any non-derivative instrument for which the entity is obliged to receive some equity instruments of its entity;

- Any derivative that may be settled for cash or any other financial asset that may be settled for the entity’s equity instrument

Classification of Financial Assets on the Balance Sheet

Based on the major classification of a financial asset, we can have the following examples of financial assets:

- Financial Asset at Fair Value through Profit or Loss: These include financial assets that an entity holds for trading purposes or are recognized at fair value through profit or loss.

- Held to Maturity Securities: Investments in debt instruments held till maturity date irrespective of changes in market prices or the entity’s financial position or performance fall under this category.

- Loans and Receivables: These include financial assets with fixed or determinable payments. They are not quoted in an active trading market.

- Available for sale: The entity can keep any financial asset in this category that does not fall in the above three categories. For example, an entity could classify some of its investments in debt and equity instruments as available-for-sale financial assets.

should be classified as loans and receivables if it is not held for trading. Further, the entity can classify it as at fair value through profit and loss or available for sale if they decide to do so. For example, an investment in shares with a certain price and if it is not held for trading should be classified as an available-for-sale financial asset.

Debt security should be classified as loans and receivables if it is not quoted in an active market and is not held for trading.

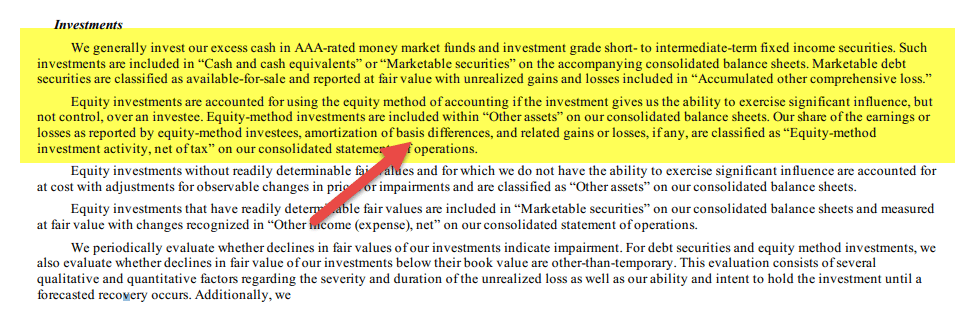

Financial Assets Examples as per US GAAP

Generally, the Accepted Accounting Principles format is followed in most US-based companies. However, their pattern of representation, valuation, and impairment is different from other reporting methods.

source: Amazon.com SEC Filing

Following are some examples of financial assets under GAAP:

- Compound Financial Instruments: Compound financial instruments like convertible bonds are not split into debt and equity components.

- Equity Investments: Under GAAP, equity investments are measured at FV-NI (changes in fair value are recognized in Net Income). However, a measurement alternative is available for equity investments that neither have readily determinable fair values nor qualify for the net asset value (NAV).

- Loans and Other Receivables: Under US GAAP, an incurred loss is the impairment model for loans and other receivables. These loans and receivables are presented in the balance sheet.

- Derivative: Under GAAP, a derivative instrument must

- Have one or more underlying asset, and one or more notional amounts or payment provisions,

- Not require any initial net investment, and

- Be able to be settled net.

- Hedging Instrument: A hedging instrument’s time value can be excluded from the effectiveness assessment.

- Public Business Entities: It shall use the exit price notion when measuring the fair value of financial instruments for disclosure purposes.

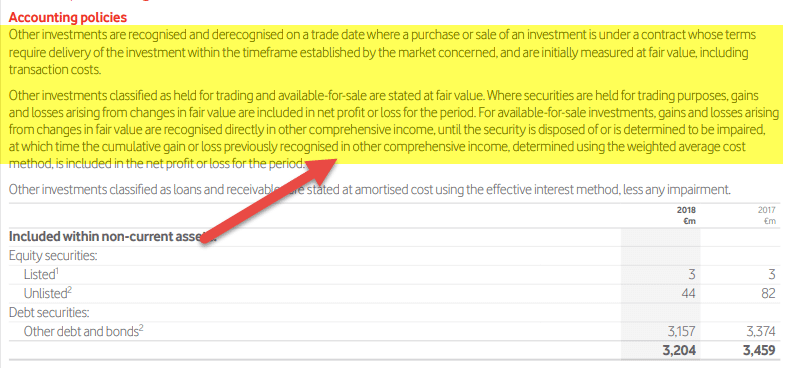

Financial Assets Examples as per IFRS

The International Financial Reporting Standards format is majorly followed in most UK-based companies. However, their pattern of representation, valuation, and impairment is different from other reporting methods.

source: Vodafone Annual Report

Based on the major classification of a financial asset, the following are some examples of financial assets under IFRS:

- Compound Financial Instruments: Compound financial instruments must be split into debt and equity components.

- Equity investments: Equity investments are measured at FV-NI (changes in fair value are recognized in Net Income);

However, an irrevocable FV-OCI election is available for non-derivative equity investments that are not held for trading. FV-OCI means changes in fair value are recognized in Other Comprehensive Income.

- Under IFRS, there is a single impairment model for debt instruments recorded at amortized cost or FV-OCI, including loans and debt securities.

- Derivative: Derivative are measured at fair value, whereas value changes are recognized in profit or loss unless it has elected for hedging.

- Hedging Instruments: The effectiveness assessment can exclude a hedging instrument’s time value, and foreign currency basis spread.

Recommended Articles

This article has been a guide to Financial Assets Examples. Here we discuss the classification of financial assets and US GAAP & UK IFRS examples. You can learn more about financing from the following articles –