Table Of Contents

What is Factory Overhead?

Factory Overhead, also known as manufacturing overhead, comprises all indirect expenses incurred by the business in the regular running of a factory's operations. It doesn’t include the direct cost incurred by way of labor and material costs.

Explanation

- These are all indirect costs, they can’t be attributed to a particular product or service directly and include expenses like depreciation, factory rent expenses of factory, electricity, property expenses, supervision expenses, etc.

- These expenses are allocated using various methods, which can be based on the amount of time spent as a percentage to direct material cost or direct labor cost or prime cost, to name a few. Due to the Indirect nature of such expenses, absorbing these expenses requires judgment and allocation skills on the part of the organization to provide a clear picture of expenses incurred.

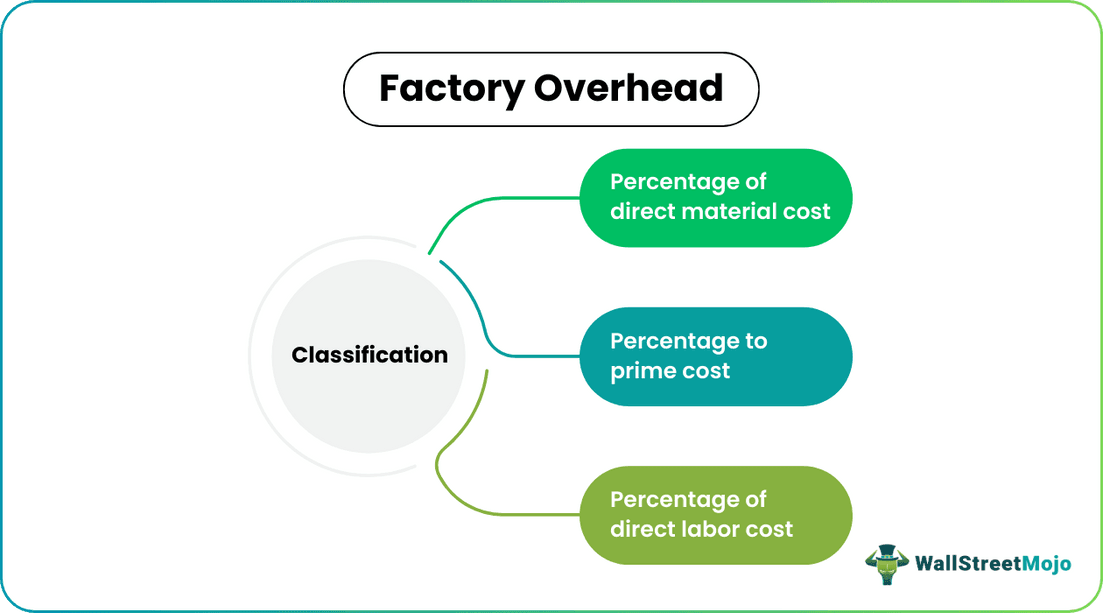

Classification of Factory Overhead

These overheads are incurred on account of meeting the regular functioning of the factory and keeping the administrative expenses incurred regularly associated with the working of the factory. Therefore, it can be classified in several ways. Some of the most popular classification techniques are enumerated below:

#1 - Percentage of Direct Material Cost

It is the simplest and the most popular method in those cases where the factory overhead cost is substantial to the total cost. Under this, the overhead rate is determined, and expenses are absorbed as per the rate.

Overhead Rate = (Direct Material Cost / Factory Overheads) * 100

#2 - Percentage to Prime Cost

Another technique to classify Factory overhead is to compute it as a percentage of the prime cost (direct material cost, direct labor cost, and direct expenses cost).

#3 - Percentage to Direct Labor Cost

Under this, it is classified as a percentage of the direct labor cost incurred by the business. However, the method lacks recognition of time devoted to work by skilled and unskilled workers, leading to biased results.

Examples of Factory Overhead

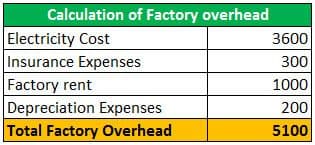

ABC International is into manufacturing oh sports shoes. The company manufactures customized sports shoes based on customer requirements. Recently ABC International has decided to quote for a tender comprising 10000 sports shoes for the LIFA brand based out of Norway.

ABC International has furnished the following cost expected to incur in the manufacturing of 10000 shoes:

ABC International charges a 20% gross margin on direct costs and a 10% margin on factory overheads. Therefore, based on the same, the price at which ABC International will quote for manufacturing 10000 shoes is as follows:

Calculate the total manufacturing overhead:

Calculate the selling price per unit:

Thus ABC International should quote $3.33 to LIFA Brand for manufacturing 10000 sports shoes.

How does the Business account for Factory Overhead?

- The allocation of factory overheads is quite challenging but, at the same time, crucial in a manufacturing setup. The cost involved is substantial and proper apportionment necessitates correct allocation to derive the real profitability of the respective departments.

- These are firstly collected from all departments/divisions. Then these are bifurcated into those which can be allocated and those which cannot be assigned. After that, based on classification, as discussed above, overheads are accounted for in each division/department. Based on this, an overhead rate is determined. It is used for budgeting purposes and comparisons over the period to determine under or over absorption.

Advantages

- It enables the business to determine true profitability by considering indirect expenses incurred by the business.

- By determining this, a business can analyze and make peer comparisons to see how their competitors are faring in and whether such expenses are more than their competitors and accordingly take remedial actions to control them.

Disadvantages

- These are indirect costs, and it is difficult to control them, unlike direct costs, as they don`t directly link with the output and, in some cases, are difficult to allocate.

- The allocation of factory overhead is a cumbersome process, and there is no single method that is entirely objective. Due to this limitation, such overhead sometimes leads to the wrong estimation of production cost or service rendering.

- Another big drawback is that allocation is generally based on machine or labor hours. However, it has been observed that not all factory overhead is linked to these factors; expenses like rent and insurance taxes are not much affected by these factors.

Conclusion

- Factory Overhead is a significant expense incurred by the business, especially in manufacturing setup. It involves all indirect expenses that cannot be directly attributable to any particular job or work is undertaken.

- However, their importance is equal to direct expenses and needs to be accounted for with utmost care. Another critical factor is the general nature of these expenses. Most of these are fixed or semi-variable, unlike direct costs, mostly variable. As such, business needs to understand these factory overheads holistically and keep a tab on them as these are most difficult to control and also, at the same time, pivotal to the success of a business.