What Is An Extrinsic Value?

The option’s extrinsic value is one of the components of the option’s total value due to time value and the impact of volatility of the underlying asset. This part of the option value does not consider the intrinsic value that accounts for the difference between the spot price and the exercise price of the underlying security.

Calculating extrinsic value may not always be easy because of the variation in calculating the volatility input of the option pricing methodology. However, if we use the option’s market price to back-calculate the volatility, such volatility is known as implied volatility.

- Extrinsic value, constituting part of an option’s total worth, is influenced by time and the underlying asset’s volatility. It excludes intrinsic value, which is the disparity between the underlying security’s spot and exercise prices.

- Calculating an option’s extrinsic value presents challenges due to varied volatility inputs in pricing methods. Implied volatility is reverse-engineered from market prices.

- Estimating extrinsic value is intricate since predicting implied volatility accurately requires knowledge of market price and cannot be determined in advance.

Extrinsic Value Explained

Extrinsic value is that concept used in investing and finance which describes the portion of the option’s price which can be attributed to the factors that are not a part of the intrinsic value.

In case of an option trading, it gives the holder of the option the risght but not the obligation to purchase or sell an underlying asset at a particular price, which is called the strike price and within a particular date, called expiration date, where the intrinsic value is the difference between the current and strike price.

But the extrinsic value of an option explains the factors like the volatility of the market, time until expiration date, the demand level of the option and interest rates. We understand that the option’s extrinsic value is one of the components of the option’s total value, existing due to time value and the impact of volatility of the underlying asset.

Thus, it can be said that this extrinsic value psychology explains the additional premium that the investors will pay in the hope that the option value will increase before expiration.

It is essential to note that this value will slowly diminish and ultimately become zero on the expiration date. On that day only the intrinsic value determines the option value.

Implied volatility can only be calculated if we know the market price and, therefore, can’t be predicted accurately, making the predictability of extrinsic value extremely difficult.

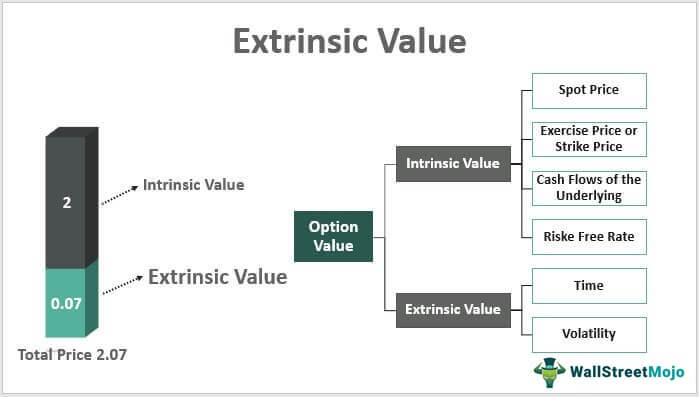

Components

The following hierarchy shows the contributors to the option value and the factors affecting these components:

- Intrinsic value is impacted by the spot price at the time of maturity, the exercise price of the option, cash flows of the underlying, and the risk-free rate used for discounting

- This is affected by the time to maturity or the expiry of the option and the volatility of the underlying

Factors

Let us analyze various factors that affect this extrinsic value psychology in the case of options trading.

- Time value, also known as the time value of decay, represented by the options greek ‘theta’ and therefore also known as theta decay, exists because the option buyer believes that in the given time to maturity, the price of the underlying might become favorable and therefore, it is believed that longer the time to expiry, greater is the time value.

- And as the time to expiry keeps reducing, this value keeps on decaying. At the time of expiry, this value is equal to zero, which is why it is known as the time value of decay.

- Volatility (option greek: ‘vega’) of the underlying has a direct relationship with the extrinsic value because the buyer buys it to hedge himself. If he believes that the underlying value is not too volatile, he would never be willing to pay the price of purchasing the option.

- Therefore, if the underlying is highly volatile, the buyer can benefit from it as options have unilateral risk. If the option is in the money, it will be exercised, while if it is out of the money, it will not. So higher the volatility of the underlying asset, the higher the risk for hedgers, and the higher the extrinsic value leading to higher option value.

- The interest rate also affects the extrinsic value because it affects the cost of carrying the underlying asset. If the interest rate is high, it leads to high cost of holding the asset, which ultimately affects this value.

- The demand or supply also affects the option price. High demand leads to increase in buyer’s competition, thus affecting the price and the extrinsic value.

Having explained the factors and their relationship with the extrinsic value, we still need to understand that measuring the extrinsic value of an option is not easy. At times, there are different option values from various analysts because of their difference in opinion about the volatility measure.

Example

Let us understand the concept with the help of some examples.

- As we have mentioned in the introduction, an option value has two components, intrinsic and extrinsic. When the investor purchases the option, the exercise price is either equal to or lower (higher) than the current spot price of the underlying for a call (put) option. This implies that the intrinsic value is 0. In the case of a call (put) option, the option has a positive payoff when the spot price at maturity is greater (lower) than the exercise price.

- Even with a 0 intrinsic value, the investor pays the premium to purchase the option. So, the entire premium is due to the extrinsic value.

- For example, if the exercise price for a call option is $100, and the Spot price of the underlying is either $100 or less, the payoff is 0. Let’s suppose that during the time of the option, the spot price becomes 110. The payoff is 110-100 = $10, and lets us say there are three months to expiry. We feel that the underlying can go up to $120, so the option price will be higher than the current payoff of 10, maybe $15, this addition of $5 is due to extrinsic value philosophy, more precisely, time value if volatility is constant.

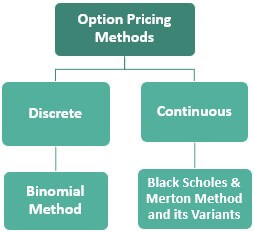

Option Pricing Methods

Based on the lengths of the interim periods from the time of purchase of the option till the time of maturity, there are two popular methods used for option pricing, the binomial method, when the periods are discrete such as two years, and the BSM method and its variants such as the Black method, when the desired pricing is continuous.

The price arrived at in any of these methods encompasses both the intrinsic and extrinsic value ethics of the option. If the market price is even higher than this price, then there can be two reasons for this:

- Either there is an arbitrage opportunity.

- Or the estimates of volatility are amiss. At times we back-calculate the volatility from the option’s current market price, which is known as the implied volatility. In contrast, there is another method for volatility calculation known as the historical method.

Assumptions of the Black Scholes Model

We need to also look at a few assumptions of the BSM because some of these are very simplistic as compared to a real-world scenario:

- We assume that the volatility of the underlying is known and constant

- The risk-free rate is known and constant

- The underlying has no cash flows

- There are no transaction cost or taxes

However, these assumptions do not always hold in the real world; therefore, the BSM model requires adjustments to incorporate such variance. Such adjustments vary from analyst to analyst, and therefore there might be a possibility that the price calculated from these methods may vary from the current market price.

We need to understand from this that it is not always the case that the market price – intrinsic value = extrinsic value, and here is the difference between the terms price and value of the option. Price may refer to the market price, the value may refer to the calculated price from one of these models, and premium may refer to the amount paid when purchasing the option.

The formula for BSM for calculation of a call option price is below for understanding:

Source: Wikipedia.org

- Without going into too much depth, we only should understand the points from the perspective of this article.

- The standard deviation is the symbol for volatility, and the T-t is the time till expiry. Therefore the formula suggests that the price calculated using this model incorporates extrinsic value ethics and intrinsic value variables.

Extrinsic Value Vs Intrinsic Value

The above are two important components used for deciding the prices of financial instruments like options. But it is important to identify the differences between them, as follows:

- The former is that part of the option’s value that cannot be attributed to the intrinsic value, which is that part that would remain if the option is exercised immediately.

- The extrinsic value philosophy reflects the volatility, interest rates, time till expiration, etc, whereas the latter reflects the difference between the strike price and the current price of the underlying asset.

- The former shows the additional gain in value and the latter represents the current or the tangible value of the option

- The former gradually diminishes as the option moves closer to the expiry date and the latter is the value that remains on the date of expiration of the option.

Thus, the following are the essential differences between the two financial concepts.

Frequently Asked Questions (FAQs)

1. What is the importance of extrinsic value?

Extrinsic value is vital as it represents the market’s perception of an option’s potential future movement. It captures elements like volatility and time until expiration, impacting an option’s overall value beyond its intrinsic worth. Recognizing extrinsic value helps traders assess risk and make informed decisions, especially when crafting strategies involving time-sensitive market dynamics.

2. What is the difference between intrinsic value and extrinsic value?

Intrinsic value is the inherent worth of an option if exercised immediately, based on the underlying asset’s current price. Extrinsic value, on the other hand, encompasses the remaining option premium beyond intrinsic value, linked to factors like time and volatility. While intrinsic value is fixed, extrinsic value can fluctuate, reflecting market sentiment and expectations.

3. Can extrinsic value be negative?

Yes, extrinsic value can be negative. This occurs when an option’s overall premium is lower than its intrinsic value. The negative extrinsic value indicates that market factors, like low volatility or short time to expiration, have reduced the option’s time value component. Traders should consider negative extrinsic value when evaluating option strategies and potential profit outcomes.

Recommended Articles

This has been a guide to What extrinsic value is & its Definition. Here we discuss the components of extrinsic value and its factors, along with examples. You can learn more about it from the following articles –