Table Of Contents

Evergreen Loan Meaning

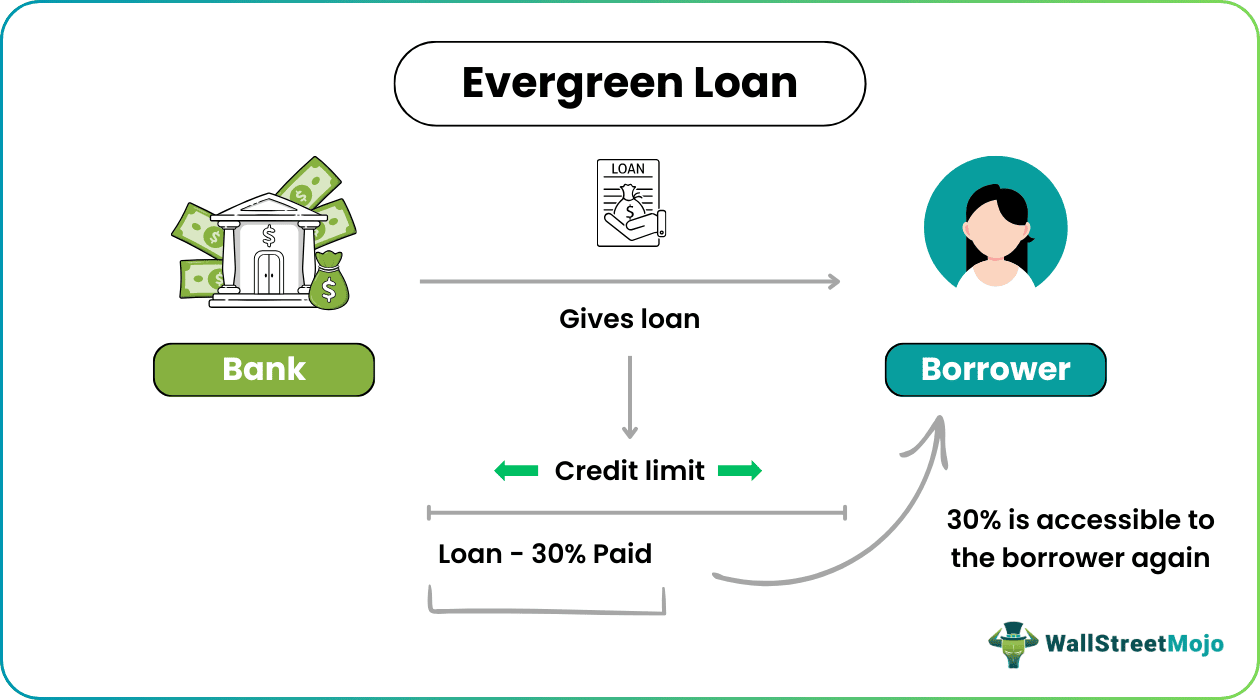

An evergreen loan, also known as revolving credit, is where the borrower receives a principal amount of the loan from the lender with a contract, interest rate, and validity for the contract. During the agreement’s sustainability, the borrower can repay the loan or retake the loan any number of times.

The borrower must pay off the interest and principal amount at the end of the agreement. Still, the benefit comes to the borrower during the contract period, where the borrower can withdraw any amount and repay the amount as per his benefit. The borrower can do this any number of times during the contract period.

Table of contents

- Evergreen Loan Meaning

- An evergreen loan is also known as revolving credit. It is a loan where the borrower obtains a principal amount from the lender with a contract, interest rate, and validity for the contract.

- The borrower can repay or retake the loan numerous times during the agreement's sustainability.

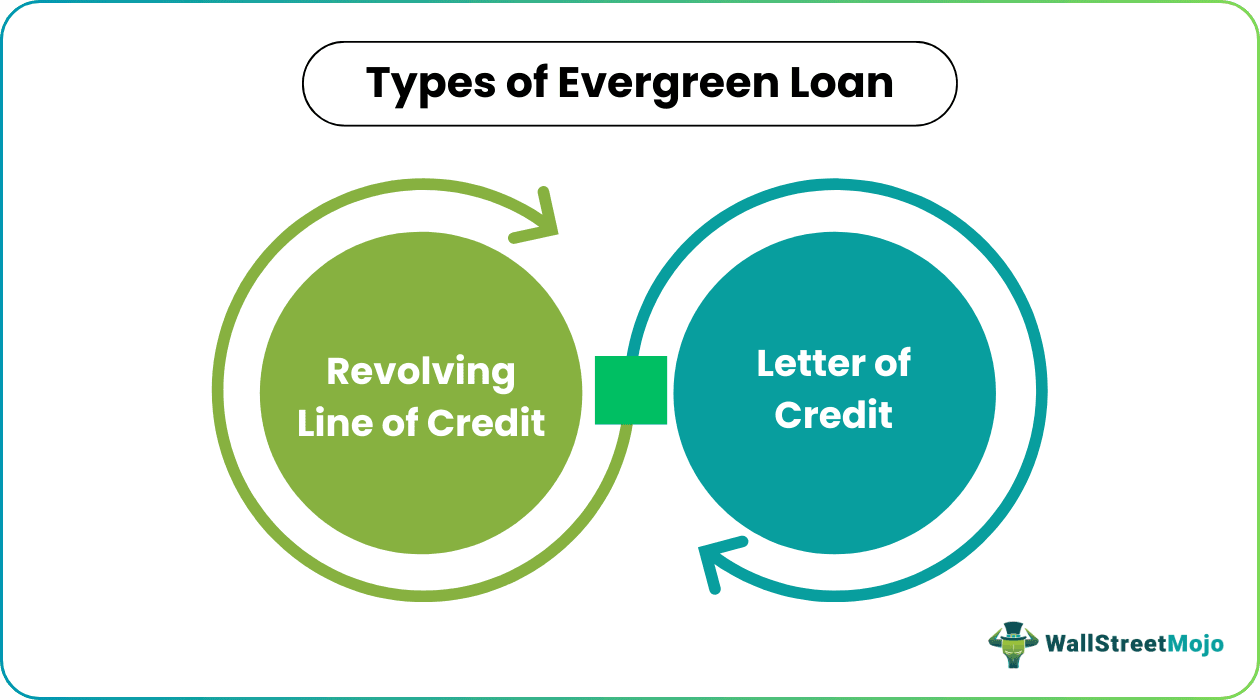

- The types of evergreen loans are revolving lines of credit and letters of credit.

- The market most commonly used evergreen loans are credit cards and lines of credit, including overdraft limit, export packing credit, etc.

Evergreen Loan Explained

Evergreen loan services also called revolving credit facilities is the one in which the borrower doe not have to pay the loan principle amount to the lender during the lifetime of the loan. Only the interest is paid. It can be related to many types of financial products and is very useful due to no requirement of re application.

On the application submitted by the applicant, the evergreen loan company offers different products relating to the revolving credit. Once the application is approved and the loan amount is also accepted, the lender (banks, etc.) gives the principal amount to the applicant (borrower), which is also bound by a maximum credit limit. The borrower can use this amount at his discretion.

This credit bank charges fees or amounts from the borrower and applies interest rates in case of delayed payment or overdrawn limit. The number of available credit decreases and increases as the borrower withdraws and pays back the funds during credit. In an evergreen loan agreement the borrower can pay the credit amount in multiple or single payments. Once the loan amount is paid, the lending relationship closes.

The borrower can use the funds up to the credit limit provided by the bank. However, the borrower needs to pay the minimum amount mentioned in the statement generated in the case of some evergreen loan payment comprising principal and interest amounts. As a result, the borrower’s credit score remains healthy for future purposes. Because based on the person’s credit score, the bank or financial institution provides the loan or credit to the person.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Types

- Revolving Line of Credit: Revolving line of credit is issued to the borrower for day-to-day use or can also be said to be working capital. The user can use the credit limit offered to pay in any transaction or event.

- Letter of Credit: This is a special guarantee provided by the bank to the person on behalf of its client that the bank will pay the obligation if the client defaults. The bank issues the letter of credit with a pre-decided credit limit to which the bank will take the financial guarantee. The client may provide a letter of credit to the other party to consider the transaction or contract.

Examples

Let us try to understand the concept with some examples.

Example #1

The most used evergreen loan services in the market are credit cards and lines of credit, including overdraft limit, export packing credit, etc.

- In the case of evergreen loan agreement of traditional credit cards, the borrower needs to apply, after which his background and credit scorecard is checked. Then the application is approved, and the credit limit is offered accordingly. In the case of credit cards, the credit card statement is generated every month. The credit card user can borrow funds up to the maximum available credit during the month. The user needs to pay the minimum amount mentioned in his statement. The more he pays back, the more credit limit will be available again.

- Banks or other financial institutions provide the line of credit to the borrower, who can be a company, an individual, or a government. In this case, a credit limit is also provided to the borrower, who can use the amount per his requirements. A monthly statement is generated in this case. The borrower needs to pay the minimum amount mentioned to improve his credit score and have a good credibility for the future.

Example#2

In the US, it is evident that evergreen loans provide scope for an economic turnaround after the Covid pandemic and economic downfall. Therefore, the Federal government hopes that this kind of loan will help the country stabilize in the short run while contributing to the business of less productive firms.

Renewal Criteria

- If the borrower applies for the renewal of the evergreen loan, the bank or other financial institution will determine the borrower’s financials and credit score before allowing the revival of the loan. For example, in the case of an evergreen loan company, the lender demands the financial statement, which is the latest for evaluating the company's economic conditions.

- In the case of renewal, the lender will check the income of the borrower to verify that the earnings of the borrower are enough to repay the loan amount and also cross verify the collaterals provided by the borrowers to evaluate whether, in case of default by the borrower, the collaterals provided will cover the loan amount or not (in the case where the lender has kept the collaterals). In case the balance of the borrower was always close to the credit limit of the previous evergreen loan, the lender might decide not to renew the loan.

Potential Issues

- There are areas where the evergreen loan payment can create some issues. For example, in the case of the borrower applying for renewal of such a loan, the bank can choose not to renew it upon looking up the borrower's financials if the borrower's financials are not strong enough.

- The bank may also withdraw from the relationship if the borrower maxed out the credit usage and did not pay any interest for a long period, like one year. In this case, the bank will oppose keeping the relationship going as they conclude that the borrower will not repay the loan.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

The interest on the evergreen loan is 18.99% with no added fees. However, on missing the payment, a missed payment fee will be $30. Moreover, the maximum loan term is 18 months.

Yes, the evergreen loans are legit. They are a practical financing option for businesses and individuals with ongoing funding needs, providing flexibility and convenience.

One risk of an evergreen loan is that the borrower may become overly reliant on the line of credit and accumulate too much debt. Additionally, these loans may have higher interest rates and fees than other types of loans, which can increase the overall cost of borrowing.

An evergreen loan facility does not need the repayment of the principal amount during the loan period or a specified time. Instead, in an evergreen loan, the borrower must make only interest payments during the loan period.

Recommended Articles

This article is a guide to the Evergreen Loan definition. We discuss the evergreen loan examples, types, potential issues, renewal criteria, and how it works. You can learn more about it from the following articles: -