Table Of Contents

What Is Embedded Insurance?

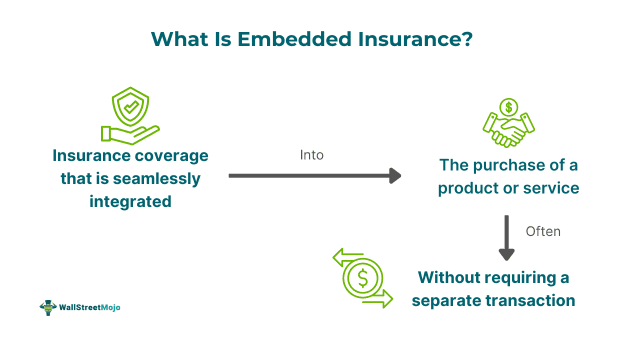

Embedded insurance is an approach where products and services that offer insurance are integrated and presented in a business offering. It provides an easy way for customers to buy insurance along with the product or service they are buying without having to approach a provider separately.

You are free to use this image on your website, templates, etc.. Please provide us with an attribution link.

It benefits both customers and insurers. For customers, it's a job made easy; they do not have to go to a provider's website separately to buy one. For insurers, it is an opportunity to make revenue with a low distribution cost. However, the provision only sometimes guarantees the best options in the market.

Key Takeaways

- Embedded insurance policies are insurance policies offered as part of another non-insurance business product offering. They are typically offered at the point of sale.

- They enhance customer experience by conveniently providing them with the option of purchasing at checkout. It makes insurance accessible to consumers.

- It reduces distribution and marketing costs for embedded insurance companies, but achieving it is challenging. These include technological integration, privacy concerns, and customer awareness.

- Various types of insurance are embedded, such as linked, integrated, and bundled.

Embedded Insurance Explained

Embedded insurance is an approach for the sale of insurance products or services as a bundle with another business product or service. It is offered in real-time or at the point of sale. Most customers may be reluctant to search for insurance products due to the time and effort required to search for and apply for one. They may feel it could be more convenient and avoid it. Contrastingly, the insurance is likely sold if they are embedded or provided alongside another product or service they purchase.

It is bundled with the purchase of non-insurance products and services. Embedded insurance products often complement business products or services. Hence, customers feel the necessity to purchase insurance as a precaution. It makes insurance more accessible for consumers.

Customers are here given a prompt to purchase, and often, it is a choice made by them. Customers feel that they are empowered to make that choice because they have already researched the product. They would have compared prices and made efforts to purchase it, and at the point of sale, when they have suggestions for coverage, they feel the offered option is a good choice. This saves them the hassle of finding a new one. Hence, they feel it is fast, convenient, and flexible.

Although embedded insurance products help insurance companies reduce distribution costs, integrating them into the technological aspects may be costly. Similarly, a lack of customer awareness can be a drawback. Privacy issues, along with regulatory issues, maybe a critical deterring factor.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

Types

Given below are some of the types of embedded insurance:

- Related embedding or bundled embedding: This is a type of offering where the insurance product is firmly embedded with the partner's ecosystem. The involvement is mandatory, such as a rider's insurance that, once taken, is inclusive of passengers as well as the rider.

- Linked embedding: It is also known as soft embedding, where partners' point-of-sale systems are transformed into insurance sales channels. In this approach, relevant insurance coverages are offered along with non-insurance products. They have relevant pricing and features without any information. The insurance purchase is voluntary, and the urgency of the moment can increase conversion rates. Examples include booking of air tickets and travel insurance.

- Bundle embedding: This is also known as hard embedding. Insurance coverage is integrated into the cost of a non-insurance product or service, which is often given as a complimentary feature. It is not voluntary, and customers are not given the option to refuse coverage. It is included in the primary purchase, such as warranty.

Examples

Let us look at some examples to understand the concept better.

Example #1

Imagine Dan is a customer who is shopping for a mobile phone. He purchased it from a famous online retailer. Dan had spent all his weekend researching the best phones available on the website and chose one that suited his preferences best. After selecting, he noticed that there was an offer provided for adding insurance for damage to the device. Since that was a popular platform, he assumed that this would be the best choice available in the market and hence bought it. This offer is known as embedded insurance.

Example #2

Mulberri, an AI-driven insurance platform, has partnered with Acronis, a cybersecurity and data protection provider, to offer embedded cyber insurance to small and medium-sized businesses (SMBs) in the U.S. This partnership enables seamless integration of cyber insurance directly through the Acronis platform, enhancing protection for businesses. The offering addresses the low adoption rate of cyber insurance among SMBs by simplifying the enrollment process and providing an affordable, entry-level policy. This collaboration aims to give businesses greater peace of mind, allowing them to focus on their operations.

Benefits

Given below are some of the benefits of these insurance policies:

- It is a convenient way of offering protection for their goods and services.

- The embedded insurance market is convenient, and it enhances the customer experience.

- the embedded insurance market makes insurance accessible to customers who otherwise would have skipped getting it because of lack of time.

- These insurances are often relevant, and hence, customers are reminded of safety even if they have forgotten it.

- It results in reduced marketing and sales costs.

- Higher profits for the embedded insurance companies and trust for the platform provider.

Embedded Insurance Vs. Non-Embedded Insurance

Given below are the differences between both concepts:

- Embedded insurance is integrated into the purchase of a non-insurance product. It is often offered at the point of sale. Non-embedded insurance policies are those that are not included in another product or service. Customers seek them independently.

- Insurance that is embedded typically is presented right before the purchase of the non-insurance product, and there is little research involved in clicking the buy option. Insurance that is non-embedded is not presented along with any other products. Hence, customers have to search for them independently. They chose the insurance product after much research and deliberation.

- Insurances that are embedded require fewer distribution charges. Insurances that are not embedded carry significantly high distribution charges.

Embedded Vs. Aggregate Insurance

Given below are the differences between both concepts:

- Embedded insurance is insurance that is embedded with another product or service purchase. Aggregate insurance covers multiple risks and policies under a single policy.

- Embedded insurance is offered as add-ons at the point of sale and also as part of a package. Aggregate insurance provides broader coverage and is hence not used as an add-on but rather as a separate inclusive item.

- Embedded insurance products deal with one or individual aspects of coverage. Aggregate insurance applies to all the claims made under the policy.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.