Table Of Contents

Down Payment Meaning

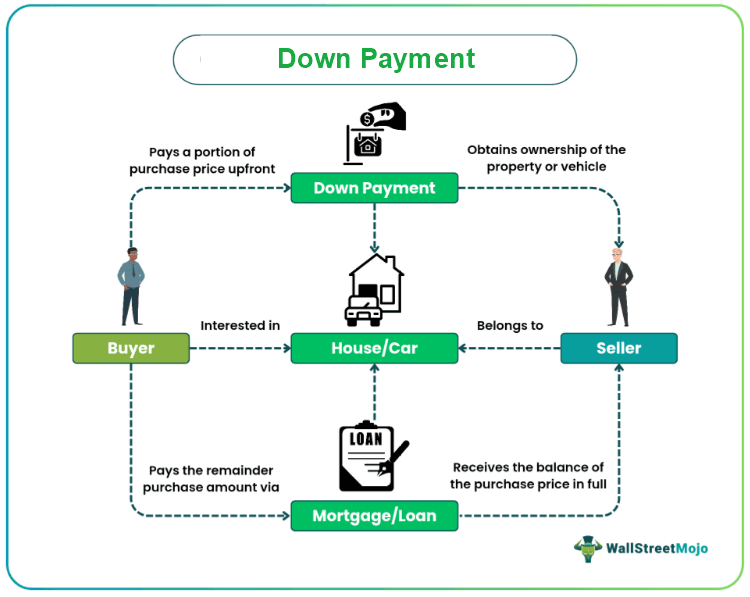

Down payment is the initial deposit made by the buyer to the seller when purchasing an expensive item, such as residential property or a car. It comprises a portion of the total purchase amount of the asset and takes place via cash, bank check, credit card, or online banking.

Aside from making the upfront payment, the buyer must pay the seller the balance of the purchase price in full. This remainder is eligible for payment in cash or through a mortgage or loan from a financial institution. A higher initial deposit allows the buyer to pay less interest or monthly installments on the money borrowed. Factors determining initial payment include asset type and value, loan form, and borrower and lender.

Table of contents

- Down Payment Meaning

- Down payment is the initial booking amount paid by the buyer to the seller for buying a high-priced asset, such as a house or car. The payment can occur in cash or via bank check, credit card, or online banking.

- In the United States, the average initial payment rate applicable for a residential property ranges from 3% to 20%. But for a vehicle, it could be 10% (used car), 20% (new car), or even higher.

- The higher the upfront payment the borrower makes for an asset, the lower the interest rate or monthly installments they will need to pay to the lender.

- Making a 20% initial payment, which is the golden standard, eliminates the need for the buyer to pay private mortgage insurance (PMI) premiums.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

How Does Down Payment Work?

Buying any high-priced asset, be it a house or an automobile, could put a burden on the buyer’s pocket. Additionally, organizing finances for the same could be time-consuming (cash payments) and add to the cost of a potential purchase (loan interests). To the buyer’s rescue, there is an option of a down or initial payment. Not only does it allow the buyer to pay only a portion of the purchase price upfront, but it also enables them to get the loan from a financial institution to pay the remainder at low-interest rates.

On average, the initial deposit for real estate or a car ranges from 3% to 20% based on their type, price, and loan opted. This wide range provides the buyer flexibility in payments. Besides, choosing to make a higher initial deposit reduces the monthly installments towards the mortgage or loan. Knowing that the borrower is less risky gives lenders a sense of security. However, financial institutions often seek collateral to secure the mortgage or loan against default to recover the loan amount.

Down Payment For A House

When making a down payment on a house, homebuyers rely on personal connections or personal savings to arrange finances. Among various factors, the initial payment rate varies based on the number of times a person buys a property. It is lesser for first-time buyers than that for repeat ones.

The National Association of Realtors, in its research, has specified that the average upfront payment remained 5% for first-time buyers for a long time. Similarly, the average median initial deposit has been 10% for repeat homebuyers.

It is worth noting that an initial deposit is not limited to 5%, 10%, or 20% of the purchase price. In rare cases, homebuyers might get rates that are even lower than 5%. For instance, it ranges from zero percent, as offered by some reputable financial lenders, to 3%, 3.5%, 5%, 15%, and 20%.

Rates Interpretation

- 0% - The United States Department of Veteran Affairs and the U.S. Department of Agriculture offer 0% initial payment scheme to veterans and rural area homebuyers, respectively.

- 3% - This down payment for a conventional loan is for those who fall into a specific income level of the area under the HomeReady and Home Possible programs.

- 3.5% - The Federal Housing Administration allows an upfront payment of 3.5% for first-time and repeat homebuyers or those with a credit score of 580 or higher.

- 5% - It is a conventional loan amount expected to be paid by homebuyers when their income limit exceeds the fixed level of an area.

- 15% - For investment properties, it usually is 15%.

- 20% - It is the golden standard as it frees the buyer from the private mortgage insurance (PMI) liability. However, charging PMI to the homebuyer ensures that the lender can cover the loss if the borrower defaults on the loan.

Although opting for a 20% down can make loan payment easier with lower interest rates and monthly installments, rising home prices across the United States have made it nearly impossible for homebuyers, especially the first-timers, to go with this option.

Down Payment For A Car

The initial payment for a used vehicle is usually 10%, while for a new automobile, it is 20%. Even though a 0% down payment on a car offered by some dealers will favor the buyer, it will also result in a higher interest rate. Buyers should consider making a higher initial deposit to keep the interest rate and monthly installments low. Also, buyers with a good credit score and hefty upfront payment are considered less risky borrowers. Hence, trusting them with the loan amount becomes easier for lenders.

How To Calculate Down Payment?

The Interest rate on a mortgage or loan is directly proportional to the initial deposit made. A buyer can use one of the various mortgage calculators available online to figure out how much they will have to pay in monthly installments. Here is an example with calculation to provide better down payment assistance to potential homebuyers:

Ashley came across a residential property and decided to buy it. The cost of it was $500,000. The property seller asked her to put 3.5% as an initial payment for the property, which she agreed to. After that, she applied for a mortgage at a bank to pay the remaining purchasing amount.

Based on the initial deposit that she agreed to pay, the bank offered her a mortgage at a 4% interest rate for 30 years. However, Ashley also wanted to keep the monthly installment as low as possible. So, she paid 20% of the purchase price as an upfront payment. To choose between the two options, she made her monthly installment calculation using the online mortgage calculator.

Scenario 1

- Property Value = $500,000

- Down/Initial Payment = 3.5% = 3.5% * 500,000 = $17,500

- Remaining amount = $500,000 - $17,500 = $482,500

- Loan term = 30 years

- Interest rate = 4%

The monthly payment, when calculated using the online mortgage calculator, was $2,304. It excluded property taxes and homeowners insurance premiums.

Scenario 2

- Property Value = $500,000

- Down/Initial Payment = 20% = 20% * 500,000 = $100,000

- Remaining amount = $500,000 - $100,000 = $400,000

- Loan term = 30 years

- Interest rate = 4%

The monthly payment, when calculated using the online mortgage calculator, was $1,910. It excluded property taxes and homeowners insurance premiums.

Thus, the difference in the monthly payment was:

$2,304 - $1,910 = $394, which came to $4,728 a year and $141,840 in 30 years.

Hence, Ashley decided to make a 20% initial deposit and save whatever she could in the deal.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

The down or initial payment is a portion of the purchase price of an asset that the buyer makes to the seller. It is more common in the buying of residential properties or automobiles. The mode of payment can be cash or bank check, credit card, or online banking.

The initial deposit rate ranges from 3% to 20% for buying a house. However, this initial payment could be 10% for a used car or 20% for a new car. The variation in rates depends on the property of the asset in question, its market value, buyer’s borrowing history, loan opted, and the lending institution.

By putting 20% down to the seller, the buyer does not require to pay private mortgage insurance premiums. Also, it proves them to be a less risky borrower in the eyes of the lender.

Recommended Articles

This article has been a guide to Down Payment and its meaning. Here we discuss down payment for house, car along with rate interpretation and how to calculate it?. You may also have a look at the following articles -