Table of Contents

What Is Digital Insurance?

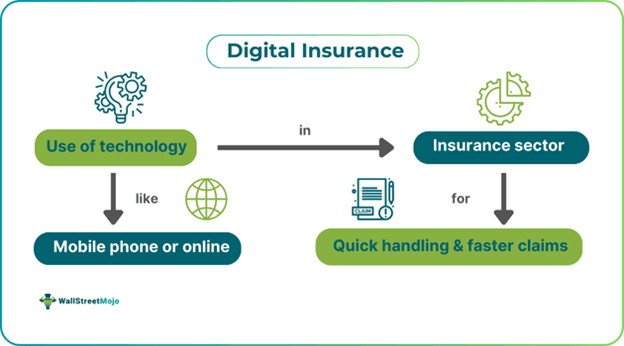

Digital insurance refers to the use of technology in digitizing the purchase and handling of insurance policies. The sole purpose of this insurance is to provide insurance and related services to customers via a digital platform without having to visit the branch.

Since the post-pandemic period, the need for digital insurance solutions has risen tremendously. It has urged insurance agencies to collaborate with service providers and cater to the growing demand for digitization in the industry. Moreover, it has helped insurance companies meet customers’ expectations and ensure proper workflow management through efficient digital platforms or channels.

Key Takeaways

- Digital insurance refers to the use of technology and digital channels for providing insurance products to customers online. It encourages AI and machine learning tools to boost this sector.

- Customers can buy policies, claim damages, and customize their policies through online means.

- Some popular trends include online purchases, personalization, leveraging artificial intelligence, big data and analytics, and telematics (or Internet of Things) systems.

- It improves efficiency, reduces operational costs, and encourages positive outcomes for the insurance company.

Digital Insurance Explained

Digital insurance is a digitalized form of providing insurance products to customers via websites or online channels. It provides insurance companies a chance to meet the industry's rising demands with the Internet and mobile phones. If a person wants to take a policy, they can surf the Internet and purchase the best option online through the provider’s website. Also, customers can file their claims online, upload documents, and track the claims' status.

The entire model of digital insurance platforms works on a customer-centric approach. It means the insurance company provides ease to the customers without them making much effort. There are various omni channels created for customers so that they can research and understand the brand better without asking any staff member. At the same time, even chatbots act as representatives on behalf of the digital insurance agency to solve all customer-related queries. As a result, artificial intelligence (AI) and advanced algorithms have struck a perfect balance between automated and personalized services.

There are certain technological pillars of such insurance agencies and their solutions. It includes AI, machine learning (ML), Internet of Things (IoT) devices, big data, analytics, and Software as a Service (SaaS) as primary tools. By leveraging ML techniques (like programmed data, shared customer data, and algorithms), it is possible to boost the claim processing process. Likewise, the shared data from customers can be further utilized to predict and prevent risks beforehand. Nonetheless, this data can further fill existing product development gaps.

Exploring insurance options can help you find coverage that fits your unique needs. For those interested in comparing a range of insurance products, resources like SuperMoney make it easier to review and select policies from top providers.

Examples

Let us look at the examples of how digitalization has taken over the limitations of traditional insurance:

Example #1

Suppose John wants to take insurance for his family and vehicle. However, with his busy schedule and work commitments, he does not have enough time to visit an insurance agent. Thus, he tries to find a digital insurance agency and gets one. John visits their website and surfs through various insurance policies available. For more clarity, he uses an AI chatbot and finally takes a joint policy. Years later, when John wanted to claim damages, ML and smart devices easily transmitted the car's information to the insurer, speeding up the claims processing process.

Example #2

According to news published in November 2024, the digital insurance platform market is supposed to reach $301.51 billion by 2031 at a compounded annual growth rate (CAGR) of 11.24% during the expected period. Some of the key drivers that can expand growth opportunities include increased consumer expectations, technological advancements, and rising operational efficiency. However, a major challenge is the privacy concerns.

Trends

Digital insurance solutions have paved the way for digitalization and customization for individuals to enter this industry. Let us look at the following trends to check how the efficient implementation of technology has improved and made online sales and purchase of policies smoother:

- Online purchase of insurance products - One of the popular trends among consumers is the purchase of insurance policies online. Since everything is accessible through the web, sitting at home and purchasing a policy for oneself has become easy. It is a hassle-free process where customers can compare different insurance products before choosing one.

- Use of AI and machine learning - The foundation of a digital insurance company depends on AI and ML algorithms. Insurers can harness AI's real power for faster claims and collecting data for developing policies. Through this technology, companies are also able to improve the efficiency of the underwriting process and investigation.

- Customized insurance - Personalization is the new normal for the latest insurance products. Nowadays, insurers try to include features catering to consumers' demands, tailoring the policies based on common individual needs. The service providers use smart devices and analytical tools to provide lower premium rates for them.

- Big data and analytics - Insurance firms collect a huge pile of data from customers. However, managing and storing them can be quite tough. With SaaS and analytical tools, insurers can gain insights into the consumer’s shared data and leverage it as a prediction and prevention strategy.

- Internet of Things (IoT) systems - Telematics and smart devices are an important bridge for gaining information from customers. It can be used to track vehicles and record and transmit information back to insurers. Likewise, the same information could be utilized for claim investigation and settlement purposes.

Benefits

There are multiple benefits of adopting digital channels in the insurance sector. Some of them are discussed below:

- It reduces operational costs for the insurance company, unlike traditional insurance firms.

- Through electronic means, the risk of loss or damage to policy is eliminated. Individuals can access information online from anywhere.

- Lower premium rates are available through customized insurance policies.

- The use of chatbots and AI technology saves the time and effort of visiting the traditional setup.

- There are positive outcomes of the data collected in the form of analytics, including efficient detection of fraud claims, improved customer experience, and more.

- The overall efficiency of the digital insurance company, along with employees, increases through digital means.

- As customers themselves have to fill out the purchase form, no false representative can mislead them. It creates a proper adherence to the regulatory compliances, thus safeguarding the customer’s interests and privacy concerns.

Digital Insurance vs Traditional Insurance

Following are some pointers that explain the differences between digital and traditional insurance. Let us look at the table detailed below:

| Basis | Digital Insurance | Traditional Insurance |

|---|---|---|

| Primary setup | It refers to the sale of insurance services via online (or digital) means. | In traditional insurance, a person has to either visit the insurance firm or meet an agent who sells insurance policies to purchase policies. |

| Claim settlement | It is customer-friendly and hassle-free through mobile phones or online platforms. | Here, there is a heavy procedure that involves heavy documentation and paperwork. |

| Pricing | There is a low operational cost involved in this insurance. | It includes a high cost comparatively due to the physical setup and executive staff. |

| Buying procedure | A person can visit the website, surf through the products, fill in the details, and purchase it. It is mostly paperless. | One has to fill out multiple forms and submit copies of documents, which makes the entire process lengthy. |

| Communication | It is easy to read the terms and conditions and research them if needed. | Here, the insurance broker or agent will act as a medium between the parties. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.