Table Of Contents

Differential Cost Definition

Differential cost is a technique of decision-making in which the cost between various alternatives is compared and contrasted with choosing between the most competing alternative. It is useful when you want to understand a) Whether to process the product further or not and b) Whether to accept an additional order at a lower current price.

It differs from the marginal cost because marginal cost includes labor, direct expenses, and variable overheads, whereas differential cost includes both fixed and variable costs.

Examples of Differential Cost

The following are examples to understand this concept in a better manner.

Example #1

ABC Ltd is a company that produces card boxes. Its monthly cost statistics are as follows:

- Units made and sold: 800 units per month

- Maximum production and sales capacity: 1200 units per month

- Selling price: $30

The bifurcation of cost is as given below:

| Activity | Variable Cost per Unit | Fixed Cost per Unit |

|---|---|---|

| Manufacturing | 17 | 3060 |

| Marketing & Administrative | 5 | 1740 |

| Total | 22 | 4800 |

They have an alternative to increasing the production of up to 900 by reducing the selling price to 28.

Please evaluate the feasibility of the option.

Solution

Option 1: Present situation: selling price 30

Hence, the entity is earning a profit of $5,600 per month.

Option 2: Alternative to increase the production

Based on the two options, the cost of both the options can be evaluated as given below:

From the above analysis, we can observe that with the change in the alternative, an entity will have to incur an additional cost of $1,000. Hence, an increase in production is not advisable.

Example #2

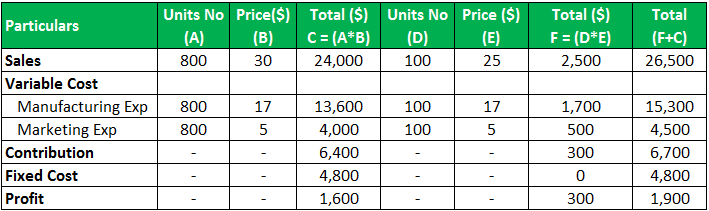

Continuing the above example, ABC Ltd. has an opportunity for a one-time-only special order to sell 100 units at $25 each. Should they accept the special order?

Solution

Option 1: Present Situation

Option 2: Accepting one-time order

The differential analysis of both the options are as given below:

Thus, we can observe an increase in profit after accepting the order. Hence, ABC Ltd. should accept the order and should enhance their profit.

Usage of Differential Cost Analysis

- Getting Prices of Products: The optimum price quoted can be won.

- Accepting or Rejecting Special Orders: Whether to work out in any additional specific order in business.

- Adding or Eliminating Products, Segments, or Customers: Whether to continue or diversify from any specific business segment or not.

- Processing or Selling Joint Products: Whether to co-produce or co-sell the products or jointly market the products;

- Deciding whether to Make Products or Buy them: Whether to manufacture the product or leverage the production facility of others.

Accounting Treatment of Differential Costing

The differential costs can be fixed, variable, or semi-variable costs. Users leverage the costs to evaluate options to make strategic decisions positively impacting the company. Hence, no accounting entry is needed for this cost as no actual transactions are undertaken, and this is the only evaluation of alternatives. Also, no accounting standards can guide the treatment of differential costing.

Conclusion

Thus, differential cost includes fixed and semi-variable expenses. It is the difference between the total cost of the two alternatives. Therefore, its analysis focuses on cash flows, whether it is getting enhanced or not. Therefore, all variable costs are not part of the differential cost and are considered only on a case-to-case basis.