Table Of Contents

What Is Depreciation Tax Shield?

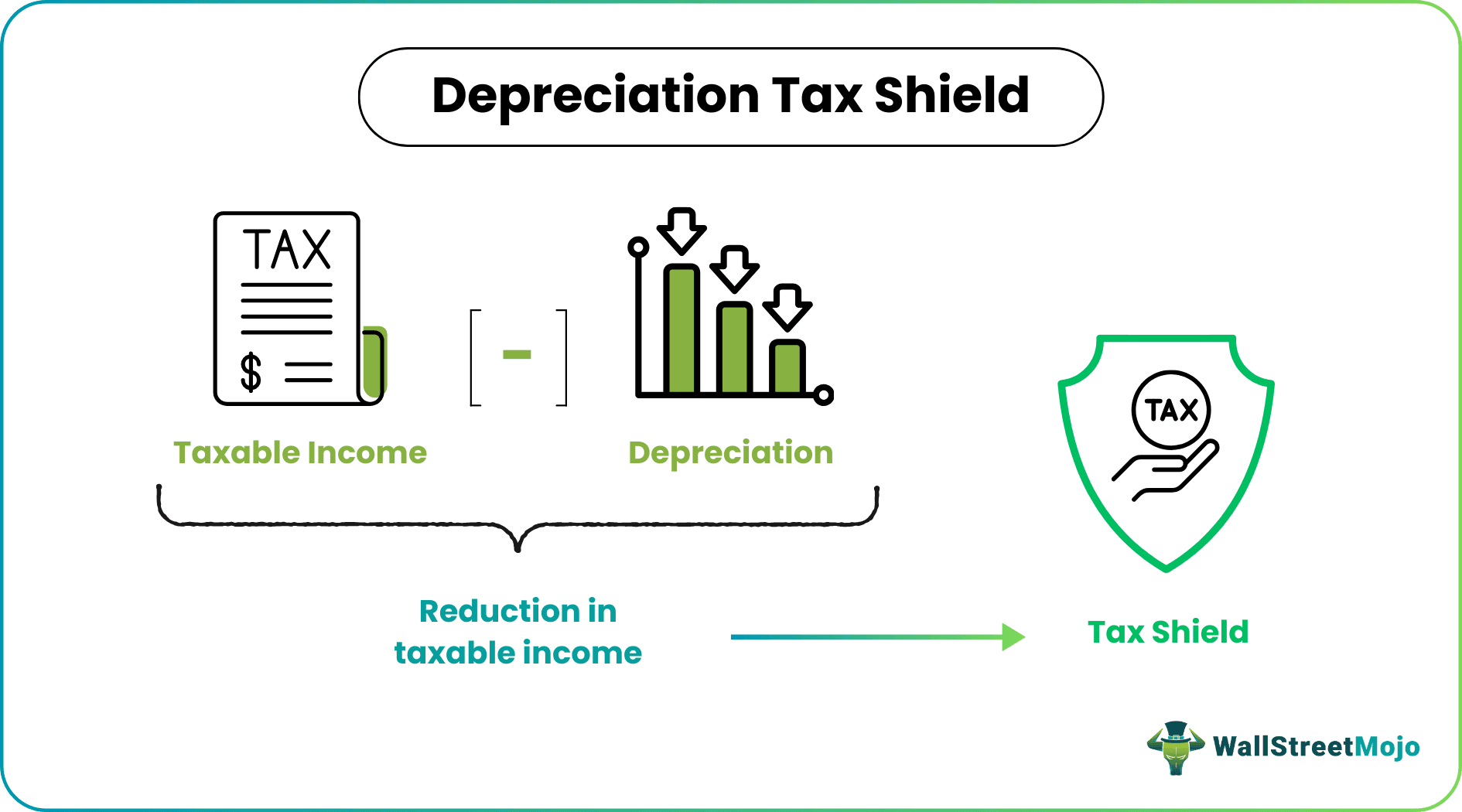

Depreciation Tax Shield is the tax saved resulting from the deduction of depreciation expense from the taxable income and can be calculated by multiplying the tax rate with the depreciation expense. Companies using accelerated depreciation methods (higher depreciation in initial years) are able to save more taxes due to higher value of tax shield.

However, the straight-line depreciation method, the depreciation shield is lower. It is to be noted that the process reduces the tax burden for the tax payer but does not eliminate it completely. A certain amount of tax obligation continues to remain with the asset. The concept is significant while making financial decisions in any capital-intensive business.

Table of contents

Depreciation Tax Shield Explained

The concept of depreciation tax shield deals with the process in which there is a reduction in the tax amount to be paid on the income earned from the business due to depreciation. In the process, the amount of depreciation is used to reduce the income on which tax will be charged, thus bringing down the amount of tax payment. Here we see that depreciation acts as a shield against tax, a cash outflow for the business.

In this context, it is important to understand what depreciation is. It is the method companies use to allocate the cost of an asset, which may be machinery, building, etc., throughout its useful life. This is done because every asset is subject to a fall in value during usage due to continuous wear and tear. The cost allocation in the form of depreciation will ultimately ensure that the final value of the asset appearing in the financial statement will reflect its true and fair current value.

In the above context, depreciation acts as a tax shield due to the fact that the fall in asset value, which is recorded in the financial statement in the form of depreciation, is expensed in the profit and loss statement. This amount in the profit and loss statement brings down the total revenue earned by the business, thus successfully leading to lower tax payments.

However, when we calculate depreciation tax shield, even though the tax amount is reduced due to depreciation, the company may eventually sell the asset at a profit. This will again partly offset the income saved from previous tax reductions.

Video Explanation of Tax Shield

Formula

The concept of annual depreciation tax shield is identified as an important factor during financial decision-making by the management in case the business is highly capital-intensive. The business operation will involve the use of assets of larger value resulting in a substantial amount of depreciation being deducted from the taxable income. Therefore, it is important to understand the formula used to calculate depreciation tax shield, as given below.

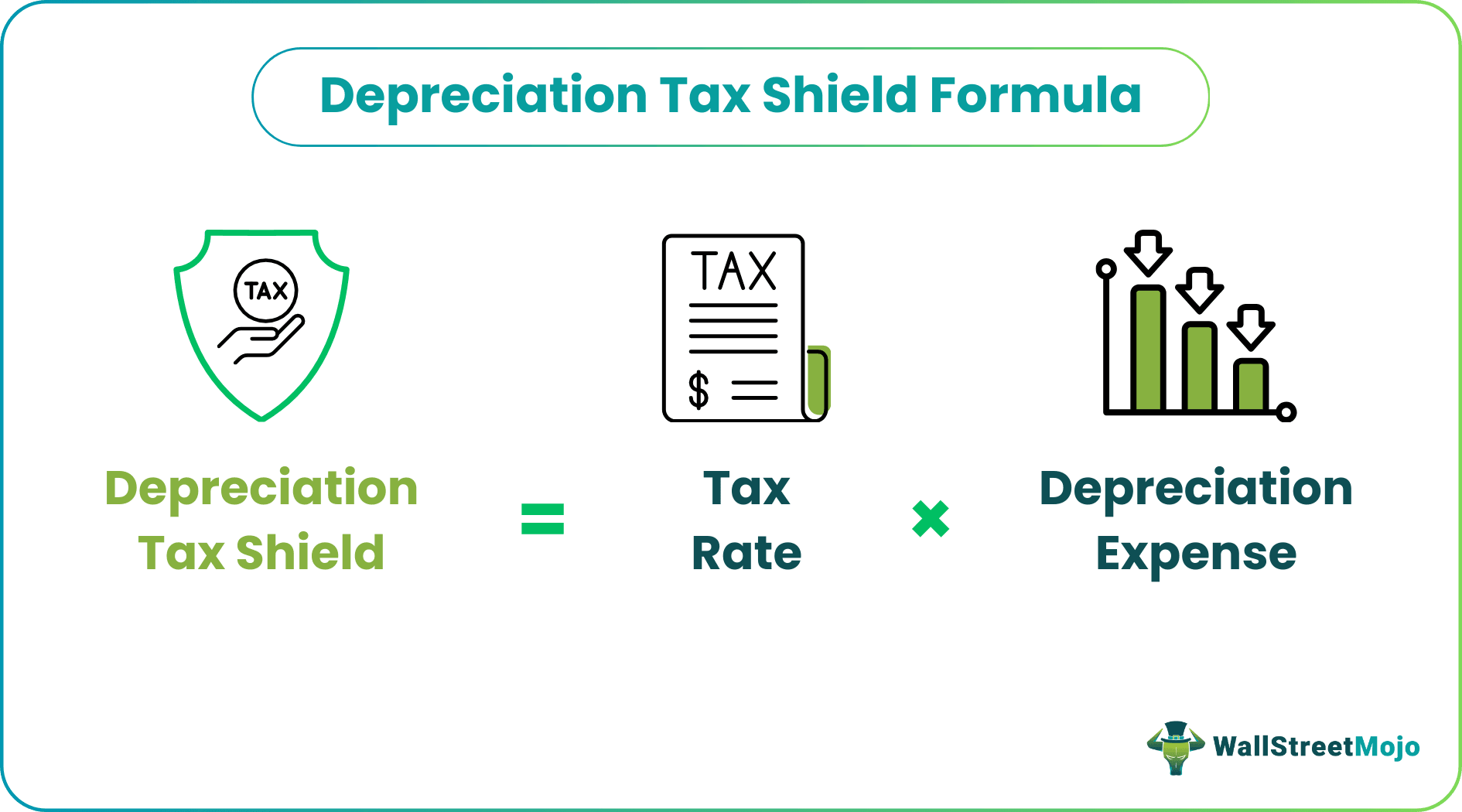

Depreciation tax shield = Tax Rate x Depreciation Expense

If company XYZ has a depreciation expense of $50,000 and the tax rate is 30%, then the calculation by using the depreciation tax shield equation will be as follows -

Depreciation tax shield = 30% x $50,000 = $15,000

Example

Let us look at a detailed example when a company prepares its tax income 1) accounting for depreciation expense and 2) not taking depreciation expense.

Case 1 - Taxable Income (with Depreciation Expense)

The tax rate considered in the example is 40%.

The Amount of Tax to be paid is calculated as -

- TAX to be Paid over Income = (Revenues- Operating Expenses-Depreciation-Interest Expenses) x tax rate

- or EBT x tax rate

We note that when depreciation expense is considered, EBT is negative, and therefore taxes paid by the company over the period of 4 years is Zero.

Case 2 - Taxable Income (not considering Depreciation Expense)

In Case we don’t take the Depreciation into account, then the Total Tax to be paid by the company is 1381 Dollar.

In the above example, we see two cases of the same business, one with depreciation and another without it. It is easy to note the difference in the tax amount payable by the business at the end of each year with and without the annual depreciation tax shield. If we add up all the taxes, the amount is substantial, which could be saved if the business had charged depreciation in the income statement.

Importance

It is necessary to understand the importance of the concept of depreciation tax shield equation in the corporate environment as a temporary benefit to save taxes. Let us identify them in details.

- It helps in reducing Tax liability. In order to promote investment, for various socio-economic development Government provides a higher Depreciation Rate.

- Allowing a higher depreciation rate attracts the investors to invest their money in a particular sector. As a result, investors get TAX benefits. The depreciation rates vary from 40% to 100%.

- In order to boost renewable energy generation and to combat climate change, the government allows incentives to the investor to lower their tax expenses by allowing them to avail of accelerated depreciation benefit for investing the money in wind power and solar power projects.

- It is also beneficial for the company due to the fact that the tax shield acts as a source of cash flow. It is a savings for the business which provides a source of funds that can be used for investment in productive projects for growth and expansion, reinvestment in the business itself for system upgradation, repayment of debt or perhaps pay dividend to shareholders on a consistent basis so as to gain their faith and confidence.

How Accelerated Depreciation Works On Tax Savings?

Assumption - For 1MW Solar Power Plant

- Project cost (capital cost) to be 1000 Dollars.

- The depreciation amount to be 90% (10 % scrap value assuming)

- Book depreciation (on fixed assets) to be 5.28 %

- Tax depreciation rate to be 80% (under benefits)

- Effective tax rate (as per government) to be 33.99%

The Life of Solar Power Plant is considered as 25 Years, but in this example, we have considered the time period for 4 years only.

The booked Depreciation Tax shield is under the Straight Line method as per the company act. The net benefit of accelerated depreciation when we compare to the straight-line method is illustrated in the table below.

| Time Period | Years | 1 | 2 | 3 | 4 |

|---|---|---|---|---|---|

| Book Depreciation | % | 5.28% | 5.28% | 5.28% | 5.28% |

| Book Depreciation Capital | Dollars | $52.08 | $52.08 | $52.08 | $52.08 |

| Opening | % | 100% | 60% | 12% | 2% |

| Allowed During the Year | % | 40% | 48% | 10% | 2% |

| Closing | % | 60% | 12% | 2% | 0% |

| Accelerated Depreciation | Dollars | $400.00 | $480.00 | $96.00 | $19.20 |

| Net Depreciation Benefit | $347.00 | $427.00 | $43.20 | $ (33.60) | |

| Tax Benefit | 33.99% | $118.01 | $145.21 | $14.68 | $ (11.42) |

We note from above that the Tax Shield has a direct impact on the profits as net income will come down if depreciation expense is increasing, resulting in less tax burden.

Recommended Articles

This has been a guide to what is Depreciation Tax Shield. We explain its formula along with example, and its importance in the business. You may learn more about accounting from the following articles –