What Is The Depreciated Cost?

Depreciated Cost of an asset is its value after charging total depreciation to date that has been accrued. Thus, it represents the remaining value of an asset that has to be utilized over its remaining life.

Formula

Depreciated Cost of an Asset can be calculated using the following formula:

Depreciated Cost Formula = Original Cost – Accumulated Depreciation

How To Calculate Depreciated Cost?

To calculate the depreciated cost of an asset, we need to deduct the accumulated depreciation from the asset’s original cost.

Original cost is the cost incurred on purchasing the asset and other expenses incurred to bring it to working condition. In other words, we can say the original cost means the purchase price of an asset and includes other related expenses incurred on it, like installation expenses.

Accumulated depreciation is the total value of depreciation that has been charged on an asset to date. Depreciation is an expense that is booked against the cost of an asset to reduce the asset’s value to its estimated salvage value (residual value) throughout its estimated life. Thus by charging depreciation, a company reduces the cost of the asset year by year to ultimately reduce the value to the salvage value at the end of the life of the asset.

Examples of Depreciated Cost

Let us understand this concept using a few examples.

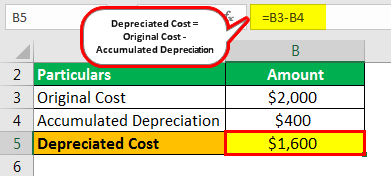

Example #1

A company had purchased a piece of equipment for $2,000 in 2012. The company charged equipment depreciation is $400 till the year ending 2018.

Solution

Calculation of Depreciated Cost

- = $2,000 – $400

- = $1,600

Here, the company had charged a total depreciation of $400 from 2012 till the year 2018. The same reflects the accumulated depreciation on the equipment. On the other hand, the company had purchased the equipment for a total cost of $2,000. Thus, at the end of 2018, depreciated value comes out to $1,600 after reducing the accumulated depreciation of $400 from the original cost of $2,000.

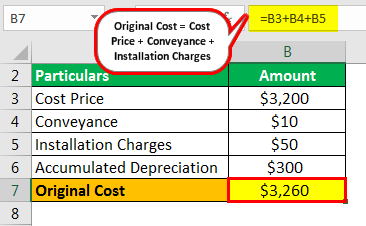

Example #2

A company had purchased a piece of machinery in 2015 and incurred the following expenses on its acquisition.

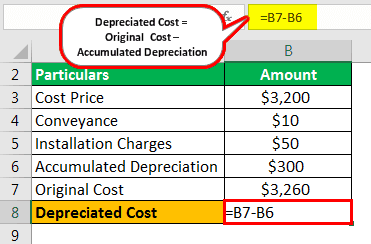

- Cost Price: $3,200

- Conveyance: $10

- Installation Charges: $50

- Depreciation charged by the company till the end of the year 2018 amounted to $300.

Now,

Let us calculate the original cost first.

Original Cost = Cost Price + Conveyance + Installation Charges

- = $3,200 + $10 + $50

- Original Cost = $3,260

Calculation of Depreciated Cost

- =$3260-$300

Here, the company had charged a total depreciation of $300 from the year 2015 till the year 2018. The same reflects the accumulated depreciation of the machinery. On the other hand, the company had incurred a total expense of $3,260 concerning the purchase of the machinery. Thus, at the end of 2018, the depreciated value comes out to be $2,960 after reducing the accumulated depreciation of $300 from the original cost of $3,260.

Relevance and Use

The depreciated cost of an asset reflects its residual value, i.e., that part of the cost that is yet to be utilized over the asset’s remaining life. It helps a company present its assets in the books of account at its current cost value. This concept allows for decreasing the asset’s cost over its useful life. It is important to note that this formula represents the book value of the asset and not the market value.

The gains on the asset sale can be calculated by comparing the selling price against the depreciated cost. The resulting difference will be a gain or loss on the asset’s sale.

Conclusion

The depreciated cost of an asset represents the remaining value of the asset that is to be amortized over its remaining life. Also, the fair value is different from the depreciated cost, and the fair value of an asset may be more than the carrying amount of an asset.

Recommended Articles

This article has been a guide to Depreciated costs. Here we discuss the calculation of depreciation costs along with practical examples and downloadable excel templates. You can learn more about finance from the following articles –