Table Of Contents

What Are Depreciable Assets?

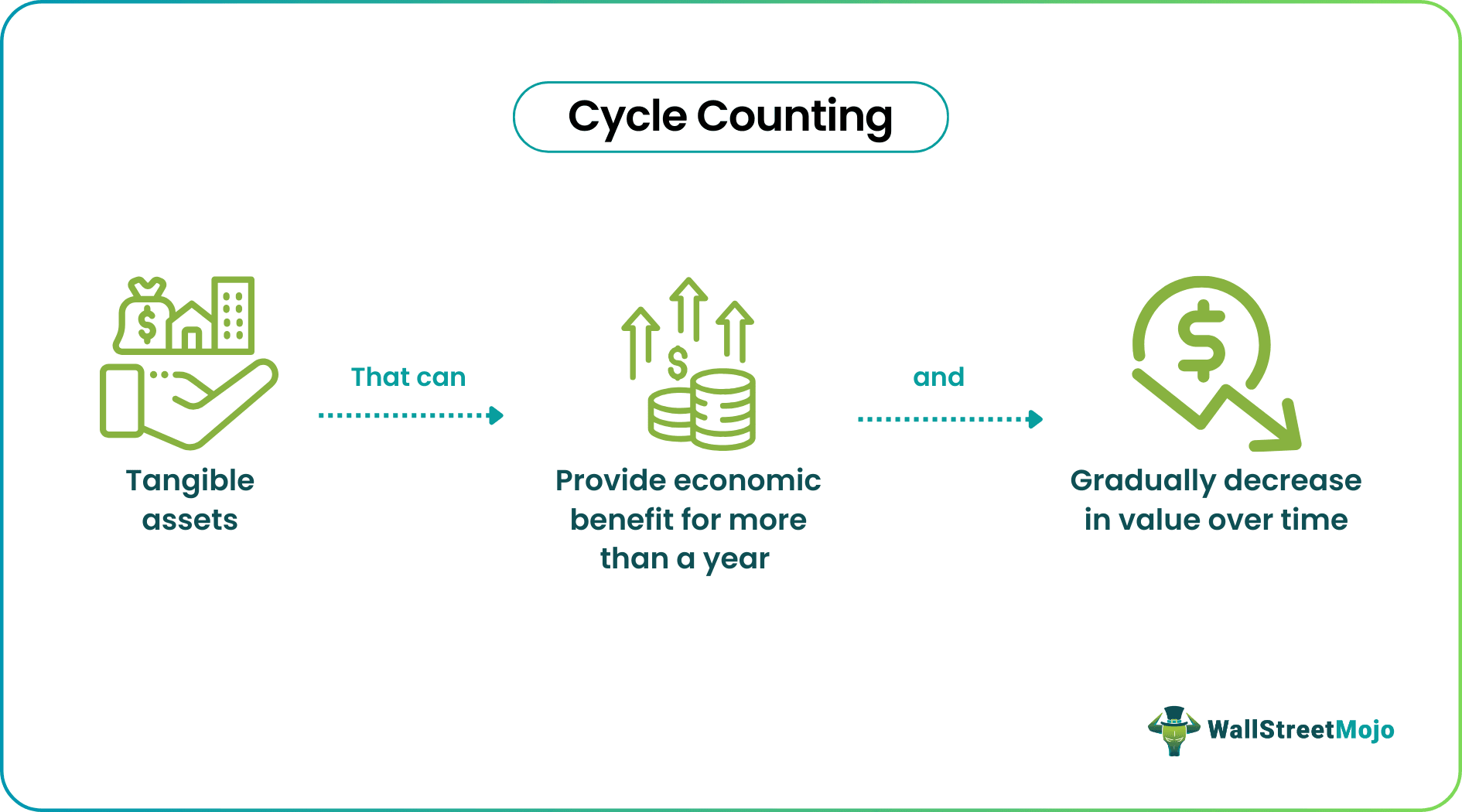

A depreciable asset is an asset used by businesses to generate income for more than a year and slowly decreases in value over time. Such an asset is eligible for depreciation treatment per tax laws aligned with the IRS or Internal Revenue Service rules. Its purpose is to provide a company with a long-term productive asset while allowing for the cost to be spread out over its useful life.

A list of depreciable assets may include tangible assets such as buildings, machinery, equipment, and furniture. Organizations purchase these assets to fulfill a particular business purpose. They can start depreciating such assets once they become available and ready to use. As these tangible assets age, they become less effective, and their value falls. Companies record the decrease in value as depreciation.

Table of contents

- What Are Depreciable Assets?

- Depreciable assets meaning refers to a tangible business asset that helps generates income for at least more than one reporting period (typically a year) but drops in value over time.

- Machinery, equipment, office furniture, building, and computers are depreciable business assets. A few tangible assets that do not make the list of depreciable assets are land, collectibles, and financial instruments like stock, bonds, etc.

- There are certain characteristics of depreciable assets. For example, they must be tangible and owned by a business. Moreover, organizations must use them in their operations.

Depreciable Assets Explained

Depreciable assets meaning refers to a property that offers an economic benefit over one reporting period. It includes any asset eligible for accounting and tax purposes to book depreciation according to the rules set by the IRS. Per the federal tax agency, the characteristics of depreciable assets are as follows:

- The asset must have the capacity to generate income, and organizations must use it in their business.

- One should be able to determine the asset's useful life.

- A depreciable business asset must have a useful life of over a year.

- The asset must be a property of the organization.

- It must not be a part of the IRS's list of properties ineligible for depreciation.

- The difference between the asset's cost and salvage value is methodically allocated to depreciation expense over its useful life.

One must note that one cannot depreciate tangible assets meant for personal use and assets or inventory held for investment. Also, organizations cannot depreciate an asset that does not lose its value over time, is unavailable, or is not ready to be used in the business. Let us look at a few examples of tangible assets that are not included in a list of depreciable assets:

- Personal property, for example, clothing, personal vehicle, and residence.

- Buildings not generating any rental income.

- Land

- Collectibles, for example, coins, art, etc.

As noted above, companies must begin depreciating assets once they place them into service. One must remember that the business does not have to use the asset, but the property cannot sit idle inside an unopened box. For example, if the tangible asset is a computer, it becomes ready to use once the organization sets it up and checks if it works. Once the set-up is complete, businesses must begin depreciating the asset regardless of whether they use it regularly.

Businesses stop depreciating an asset when any of the following events occur:

- First, the organization sells the asset.

- Second, the asset reaches its useful life's end.

The length of an asset's useful life depends on the class for depreciation treatment, and In this case, the IRS sets limits. For example, tractors and livestock have a useful life of three years. In contrast, the lifespan of office furniture is seven years.

Examples

Let us look at a few depreciable asset examples to understand the concept better.

Example #1

Suppose Panther Tees, a t-shirt manufacturer, listed its equipment, machinery, and building under a PP&E account in the financial year (FY) 2012. In the case of straight-line depreciation, the useful life of the building, machinery, and equipment was 20-35, 7-12, and 8-10, respectively.

In FY2022. The business recorded accumulated depreciation worth $35 million.

Example #2

Johnson & Johnson has plans to transition into offering corn-based talcum powered. Because of this, the company may even reorganize its business procedures. As a result, the company's decision to opt for a slump sale is a wise move.

Experts believe that a slum sale is better than an itemized one. The reason behind this is that organizations are required to pay GST at a NIL rate on slump sales. In contrast, they are liable to pay taxes if they sell the business via the usual methods.

Moreover, when a business sells one asset at a time, a short-term gain of 30% applies to the sale. On the other hand, the sale of assets via a slump sale is subject to a short-term gain of 20%, provided the company has carried out operations for over three years.

Depreciable Assets Capital Gain

Section 1231 of the U.S. Internal Revenue Code defines depreciable or real business assets held for over one year as Section 1231 property. The gain earned from the sale of such assets is subject to taxation at the lower capital gains tax rate against the rate applicable to ordinary income. One must note that Section 1231 gains do not apply to depreciable or real assets held for less than a year.

If gains on Section 1231 properties exceed the adjusted basis and the depreciation amount, the earnings are capital gains. Such gains are subject to a tax rate below ordinary income. That said, if losses are recorded on such a property whereby the loss is ordinary, it is fully deductible against the income.

If income qualifies as capital gains, so would a loss. That said, it can be deductible only up to $3,000 for that tax year, and one can arrive at losses above that figure next year.

Sale And Disposal Of A Depreciable Asset

Disposal of an asset eliminating an asset from an organization's accounting records. Businesses may decide to dispose of an asset if they sell it, in case of theft, or if the asset depreciates fully.

Individuals can record the disposal of an asset by following these steps:

- Compute the decrepitation amount.

- Record the asset's sale amount.

- Credit the asset.

- Eliminate all instances of the tangible asset from all records.

- Check if the work done is accurate.

Eliminating every trace of an asset from the balance sheet requires a business to record the losses and gains associated with the disposal.

Let us look at an example to understand how businesses can record the disposal.

Suppose Amacon, a manufacturer, purchased a machine for $80,000 and recognized depreciation worth $8,000 yearly for ten years. Once the machine depreciated fully, Amacon gave it away and recorded this entry:

| Debit ($) | Credit ($) | |

| Accumulated Depreciation — Machinery | 80,000 | |

| Machinery | 80,000 |

Besides disposal, individuals must know how to record the sale of a depreciable business asset. One can follow these steps to compute the gains or losses generated upon the sale of an asset.

- Determine the asset's initial value.

- Compute the depreciation using techniques like the straight-line or book value method.

- Negotiate the asset's sale price.

- Compute the gain or loss.

- Record the gain or loss.

Let us look at an example of an asset sold for a gain.

Suppose Yolex, a watch manufacturing company, sold a machine for cash worth $10,000. The original cost of the machine was $100,000. The accumulated depreciation complied was $75,000. The entry passed by Yolex was as follows:

| Debit ($) | Credit ($) | |

| Cash | 10,000 | |

| Accumulated Depreciation | 75,000 | |

| Gain from the sale of machine | 15,000 | |

| Machine | 100,000 |

Frequently Asked Questions (FAQs)

Tools are depreciable business assets if they meet the following criteria:

- Their useful life must exceed a year.

- A business must own the tools.

- The organization must use them in the business.

The tools will begin depreciating once the business puts them in service, i.e., once they are available to the organization and ready for use.

Once organizations complete the sale of an asset, they must credit the sale proceeds to the asset account.

One can compute the book value of a tangible business asset using the following formula:

Book Value = Overall Cost Of The Asset – Accumulated Depreciation

Let us look at this example.

Suppose a manufacturing company purchased a machine for $5,000 in FY2015, and the accumulated depreciation at the end of FY2023 is 2,000. The asset's book value is $5,000 - $2,000, i.e., $3,000.

The land is not a depreciable business asset because its useful life is infinite.

Recommended Articles

This article has been a guide to what are Depreciable Assets. Here, we explain the topic in detail with its examples, capital gains, and sale & disposal. You may also find some useful articles here -