Table Of Contents

What Are Demand Deposits?

Demand Deposit is the money deposited with a bank or financial institution that can be withdrawn without giving any prior notice, and usually, it does not pay any interest or a notional amount of interest due to the shorter lock-in period as compared to a time deposit which is made for a specific lock-in period and pays a fixed amount of higher interest.

- A demand deposit means money from a bank or financial institution. It can be withdrawn without giving any prior notice. Due to the shorter lock-in term compared to a time deposit for a certain lock-in period, it does not pay interest or a notional sum. It gives a fixed higher interest rate instead.

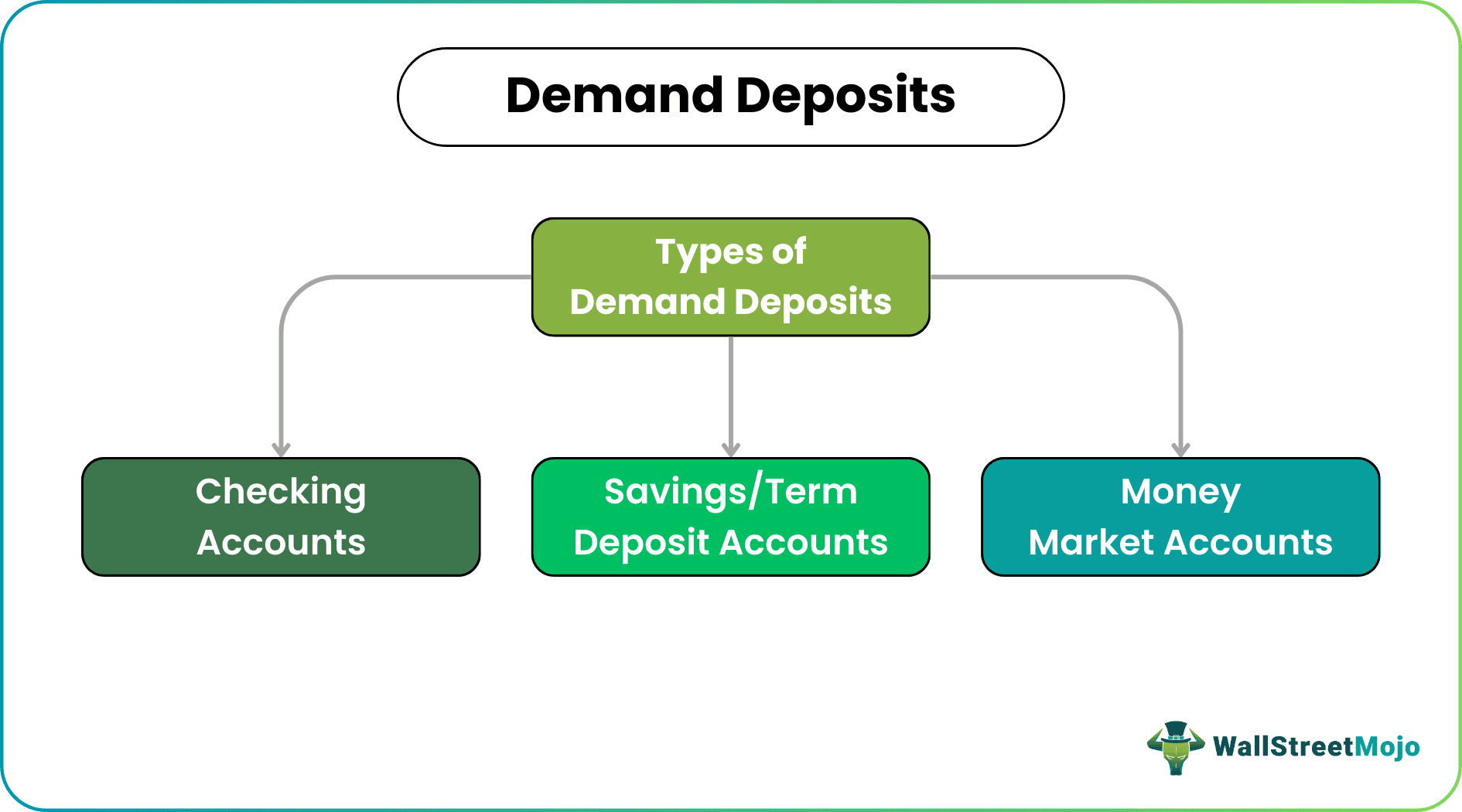

- Checking accounts, saving/term deposit accounts, and money market accounts are demand deposit types.

- The two crucial suppliers of demand deposits to commercial banks are households and non-financial businesses. Households have 35% of total private demand balances, while non-financial companies own 50% in the United States of America.

Demand Deposits Explained

Bank demand deposits offer higher liquidity than any other deposit products offer. It’s a readily available source of cash for individuals and businesses. Though the rate of return is lower, it offers a risk-free return. Also the fee to maintain and operate these deposits is much lower when compared to other exotic investment products available in the market.

Demand deposits are money deposited in any bank account that has the facility of withdrawal at any time. They mostly pay no interest to the depositor but the money can be used at any point of time for urgent purpose.

It is not necessary to inform the bank or the financial institution about the withdrawal of money, which means that the fund is immediately available for usage. There is no lock in period for the deposit and it does not require any minimum eligibility for opening the account.

Although steadily declining in importance on the commercial banking system's balance sheet, such deposits remain an important source of funds. Privately owned demand deposits in the 1990s equaled over 30 percent of total deposits.

The two most important suppliers of demand deposits to commercial banks are households and non-financial businesses. Households owned 35 percent of total private demand balances, while non-financial businesses owned 50 percent in the United States of America.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Types

Let us look at the various types of bank demand deposits.

#1 - Checking Accounts

Checking accounts are the most common and easy to use. It allows easy access to cash by withdrawing it anytime from ATMs, Bank's Teller, Debit Cards, and writing checks provided by the bank. Also, checking accounts do not pay any interest in most banks due to their pure on-demand nature.

Checking accounts helps in improving the short-term liquidity for small businesses by providing easy access to cash when needed due to working capital requirements.

#2 - Savings/Term Deposit Accounts

Savings/Term Deposit accounts are for a longer duration than a checking account. One of the various demand deposit features is that they offer lesser liquidity and more interest rates than a checking account. The drawback is that they do not offer any check writing facility, but users can withdraw funds through Bank's Teller and online banking. Sometimes early withdrawal leads to some additional charges by many banks, but there is no charge to maintain these accounts.

Account holder can easily transfer money from one deposit product to another as per the standing instructions to the bank. E.g., Banks such as Barclay's issue term deposits to corporate customers known as Wholesale term deposits, whereas, when issued to retail customers, it is known as Retail Deposits. There are also sweep-in and sweep-out facilities in this product.

#3 - Money Market Accounts

Money market accounts are based on market interest rates based upon macro variable factors as determined by the country's central bank. As the interest rates fluctuate daily, it becomes unpredictable as sometimes it offers more interest than savings accounts and sometimes lesser. It also offers more or less the same demand deposit features as we discussed above for savings accounts. Banks generally do not charge any fee for maintaining this facility for their customers.

Example

John has a balance of £100,000 in his savings bank account as of August 1st. On August 15th, he received £200,000, and the proceeds of the Term Insurance policy amount matured. On August 25th, he withdrew a sum of £200,000 to renovate his house, thereby reducing his Savings Bank account balance to £100,000.

Assume that interest is calculated at 4% p.a. on his savings account on a daily product method.

- From August 1st to 14th, he will be paid interest on £100,000 for 14 days.

- From 15th to 25th, interest calculation is on £300,000 for 10 days.

- For the remaining six days, interest calculation is on £50,000

- So, the interest he earns for the month of August will be £581 (rounded).

So, every rupee one keeps in a Savings Bank account earns interest, calculated on the daily product method. For February, the days will be either 28 or 29 days.

Advantages

Some of the benefits of demand deposits are as follows.

- Ease of access: Demand Deposits such as checking accounts always provide quick and easy access to the bank's customer through various means such as ATMs, Online Banking, Bank tellers, Check writing, etc.

- Liquidity: As the name suggests, the account holder can 'demand' money for withdrawal any time they want. Hence, they have liquidity of funds for personal and business needs.

- No Extra fees: Withdrawal from such an account does not have any withdrawal charges.

Thus the above are the benefits of demand deposits.

Disadvantages

- High Fee and Lower Interest: Banks always pay a lower amount of interest than time deposits. Also, the fee charges of the banks to maintain these facilities due to their less liquid nature are always on the higher side compared to term deposit facilities.

- Low Interest on demand deposits is sometimes lower than risk-free investments such as "treasury bonds," which leads to low capital appreciation compared to the market inflation rates. There are many other investment opportunities available in the market that, once explored, offer a higher rate of returns than demand deposits.

Demand Deposits On Financial Statements

As per IFRS9 Disclosure requirements, Demand Deposits are shown as amortized cost deposits. These are categorized as current accounts and overnight deposits on ABC Bank's balance sheet. Interest income on such deposits is shown as Net Interest Income in the Profit & Loss statement for the period of a Banking Institution. This Net Interest Income is Gross Interest Income on Loans and Advances net of Interest expense on Demand Deposits and other deposits taken by the bank from the customers.

ABC bank's disclosure notes also require industrial sectorial bifurcation, geographical distribution, and product classification. Resident and Non-resident distribution of deposits are also mandated in yearly disclosures.

Demand Deposit Vs Time Deposit

- The former does not have any lock in period whereas the latter has a lock in period.

- Due to the above clause, the former does not have any maturity date but the latter have.

- The banks do not offer or give low amount of interest on demand deposits whereas the latter offers interest on the deposited fund.

- Demand deposit is fund available in liquid form whereas the time deposit is not.

- The former does not charge any penalty for withdrawing any amount whereas is any fund is taken out from term deposit before maturity, there is penalty.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

Demand deposits are considered money because they can be removed anytime. Sometimes, they behave in addition to cash and cheque payments, a kind of money in the bank.

Demand deposits can be disapproved as a payment medium. Therefore, it is a non-legal tender. Legal tender refers to a form of payment recognized by the law to settle a debt.

Demand deposits are demand and fixed deposit accounts combined where a balance in the Savings account over a limit is auto-swept to generate a fixed deposit. If the balance is below the limit, a fixed deposit part is converted into cash to return the set limit balance.

Recommended Articles

This article has been a guide to what are Demand Deposit. We explain them with example, types, differences with time deposits, advantages & disadvantages. You can learn more from the following articles –