Table Of Contents

Demand Meaning

Demand is defined as the ability of a consumer to buy goods and services in the market. In economics, this term is associated with various elements and aspects of the business. These include product prices, customer preference, product supply, competition, production, and sales.

It reflects consumers' willingness to pay a certain price for a specific product or service. Unless customers need or want a product, there would be no supply, businesses would collapse. Therefore, demand is crucial for the continuation of business operations.

Table of contents

- Demand Meaning

- Demand refers to the consumers' ability to purchase goods and services. Customers' wants and needs are the primary determinants of supply, sales, revenue, profits, and goods production.

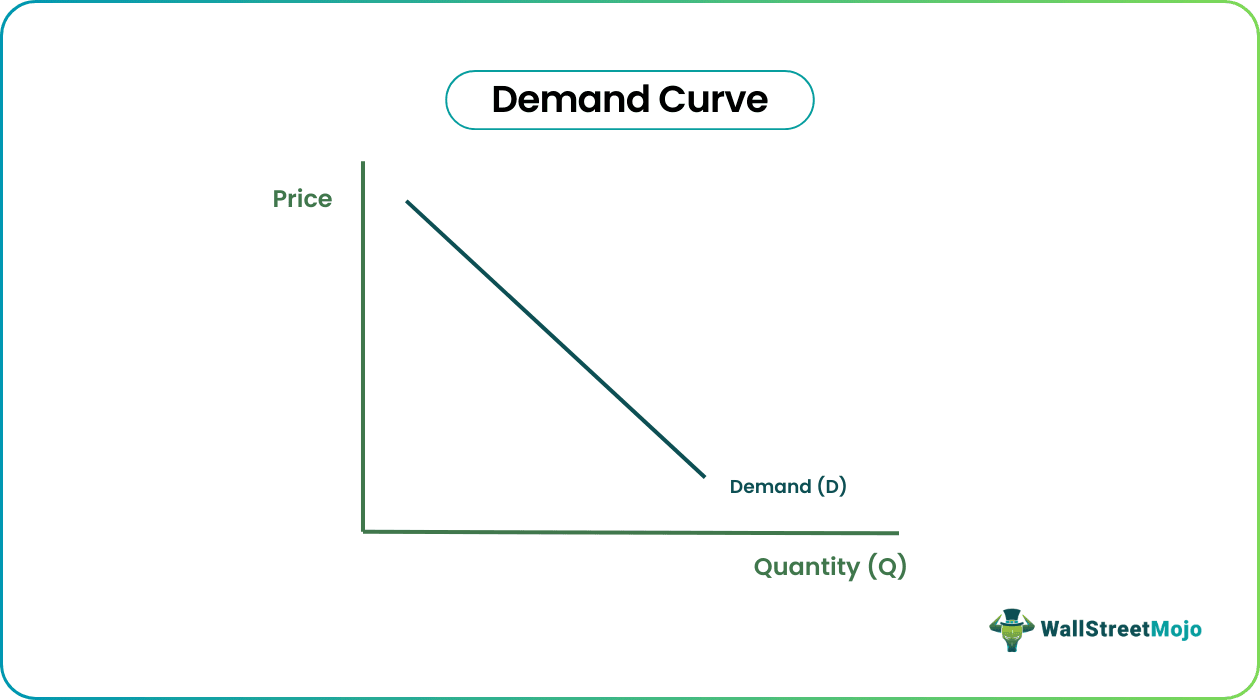

- When it is represented graphically, the demand curve showcases the relationship between a product's price and quantity.

- An increase or decrease in consumers' income is directly proportional to their ability to buy a product. Therefore, if consumers earn more, they consume more and vice versa.

- Consumers will compare and opt for the cheaper alternative if similar and equally useful products are available.

Demand Explained

Demand is a consumer's desire and willingness to buy a product at a given price. For example, if the price increases, the customer might hesitate, and the willingness to buy decreases. It is further categorized into two; market demand applies to a particular product; aggregate demand refers to the demand for all goods and services in the market.

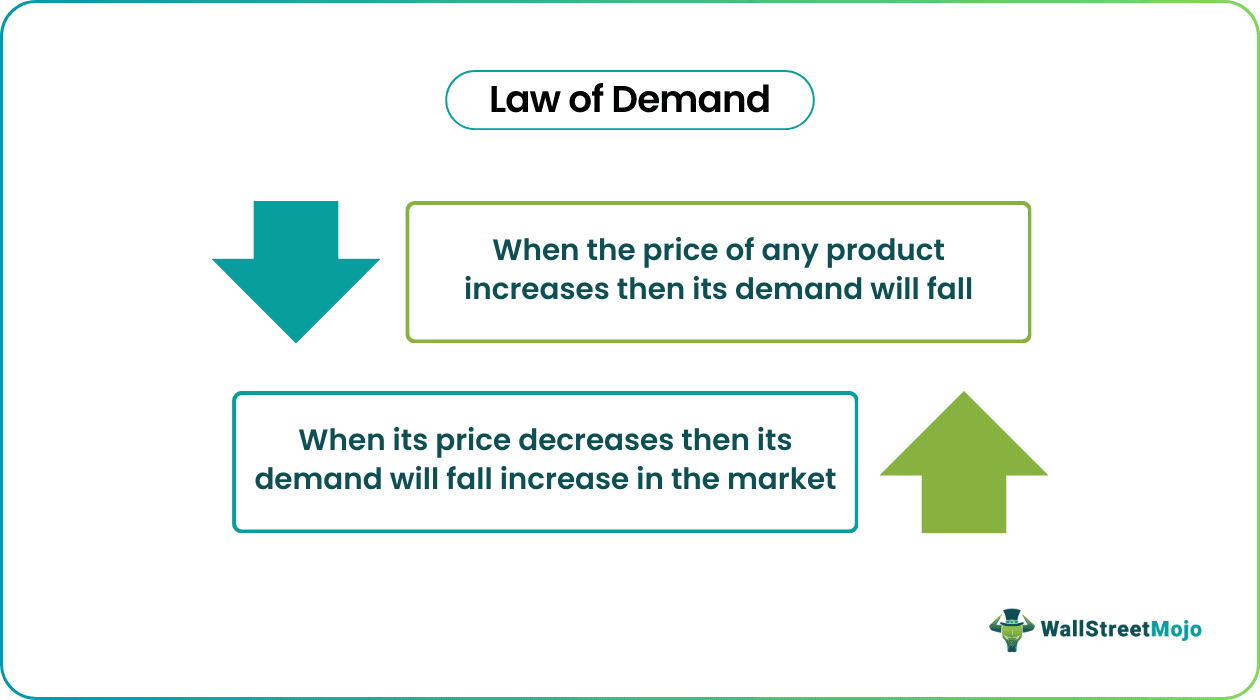

When consumers are interested in a product and are ready to purchase it at a specific price, it showcases a healthy demand for a product or service. English economist Charles Davenant introduced the famous law of demand in "Probable Methods of Making People Gainers in the Balance of Trade" in 1699.

The law states that the demand is inversely proportionate to the price of a good or service. This law states if the price is low, the customers' willingness to purchase increases and vice versa. However, several other factors determine the need for a product.

Demand definition also elaborates its importance for manufacturing and business operations. How much customers want a product or service determines its success or failure. By forecasting customers’ affinity to a product, businesses can make important manufacturing, supply, and distribution decisions. Sometimes this could even mean the need to discontinue production.

When it is represented graphically, the demand curve showcases the relationship between a product's price and quantity. Apart from commodity price, various other factors affect the curve—change in consumer income, the rise or fall in the price of substitute, a shift in consumer preference towards the competitor’s product, an increase or decrease in the product supply, and consumer expectations.

Some products defy basic laws that govern free markets. Yet, customers keep buying these products irrespective of the price. Apple’s iPhone is one such product, where its brand image, recognition, fan base, and goodwill are so strong that consumers buy it every year despite high prices.

When economists study two products and analyze the change in the purchased quantity of product A due to price changes in product B, it is referred to as elasticity.

Demand Determinants

Primarily, there are five determinants.

#1 - Price

When a consumer makes a purchase, the product's price is usually the first thing that affects the customer’s willingness to buy. An increase in prices reduces customers' wants and needs for a product.

#2 - Preference

Product sale is highly affected by consumer preference. If the product does not interest the consumer, they will not pay for it, irrespective of features or quality.

#3 - Income

For the willingness to pay, a consumer must earn or have an income. Therefore, an expensive product will not appeal to a customer with a low income. Simply put, low income reduces customers’ willingness to buy a certain category of products.

#4 - Substitutes

If similar and equally useful products are available, consumers will compare products and opt for the cheaper alternative. This phenomenon is fundamental to customer behavior.

#5 - Expectations

Consumers have certain expectations with each product—it solves a problem or offers satisfaction. Consumers would not buy the product again if said expectations were not met the first time. It will drastically affect customers’ willingness to buy that particular product in the long run. Therefore, customer retention is crucial.

Types of Demand

It is a fundamental economic concept and is further subdivided into seven types.

#1 - Price Demand

Companies cannot sell a product at an unrealistic price. There is a particular price point beyond which customers will lose interest in the product. The product is considered expensive, and customers start looking for substitutes.

#2 - Income Demand

An increase or decrease in consumers' income is directly proportional to their ability to buy a product. Therefore, if consumers earn more, they consume more and vice versa.

#3 - Composite Demand

It is associated with the types of products that have multiple uses. For example, milk derives multiple products like cheese, cream, butter, cottage cheese, etc. Therefore, any variation in these goods affects the overall demand and may eventually lead to a supply shortage.

#4 - Competitive Demand

This subtype refers to products in the same category. When substitute products are available, consumers explore their options. If the regular brand is out of stock or inflated in price, the substitute products will observe a rise in sales.

#5 - Joint Demand

Certain products are used in a set, and the sale of one influences the sale of the other. The two products are linked. Some examples are bread and butter, milk and cereals, shoes, and socks. It does not mean that these products are less useful on their own. The concept only highlights that the sales trends for set products resemble each other.

#6 - Direct Demand

It is related to products' independent usage. This is usually applicable to finished goods. They are also called derived demand products because their usage evokes the necessity for other related products. For example, if mobile usage is the immediate need, behind the scenes, it triggers the need for an internet service provider, sim card manufacturing, etc.

#7 - Short and Long-Run Demand

Both are based on consumers' behavior and reaction toward a price change. Almost all consumers accept the new price in the long run. For example, if the products' price declines, but the manufacturing cost stays high, the company has to incur losses. But, in the long run, businesses try to find new ways to cut production costs.

Example

Catelyn lives in a small village. Farmers in her village faced trouble procuring fertilizer; they had to travel to the city. In response, Catelyn starts manufacturing one at home.

At first, she sells it at a low price of $1 for a can of fertilizer. Catelyn was skeptical about the product, but the results were astonishing, and in just two weeks, farmers started asking for more.

Looking at the positive customer response, Catelyn ramps up production. She quits other sources of livelihood and goes all in. Unfortunately, supply is barely keeping up with the sales, so Catelyn raises the price of a can to $3.

Even at $3 per unit, the product attracted farmers from nearby villages. At this price, the product was cheap for the farmers. Therefore, during peak season, Catelyn further hiked the price to $5 for a fertilizer unit. Despite the price hikes, sales climbed steadily.

In this example, farmers ‘willingness to buy fertilizer is the demand. The product introduced by Catelyn showcases an urgent need and defines both buying behavior and the farmers' ability to pay for it.

Frequently Asked Questions (FAQs)

The law states that the requirement for a product is inversely proportional to the price and therefore varies depending on fluctuations. So, if the product's price is high, customers' willingness to buy the product will reduce, and vice versa.

Some products and services do not follow laws governing free markets. They have an elasticity associated with the product's requirement. Elasticity measures the change in product sales concerning price change. The product exhibits perfect elasticity of demand when the formula creates a value greater than 1. Customers do not reduce the purchase of elastic products even when the price rises.

The curve elucidates the relationship between the product price and product quantity. It is generally a downward slope on a graph where the quantity is on the y-axis and the price is on the x-axis. In this relation, price is the independent variable, and the product is the dependent variable.

Recommended Articles

This has been a guide to Demand and its meaning. We explain its determinants, types, and an example. You can learn more about it from the following articles -