Table Of Contents

What Are Deferred Expenses?

Deferred expense is the expense the company has already paid for in one accounting year. Still, the benefits for such expenses have not been consumed in the same accounting period, and it is to be shown on the asset side of the company's balance sheet.

The dictionary meaning of "defer" is to put off to a later time or postpone. With that in mind, we can say that deferring an expense means postponing the expenses. But this activity of postponing the expense does not mean the expense is not made. Instead, the postponing is done in reporting that particular expense.

Table of contents

Deferred Expenses Examples

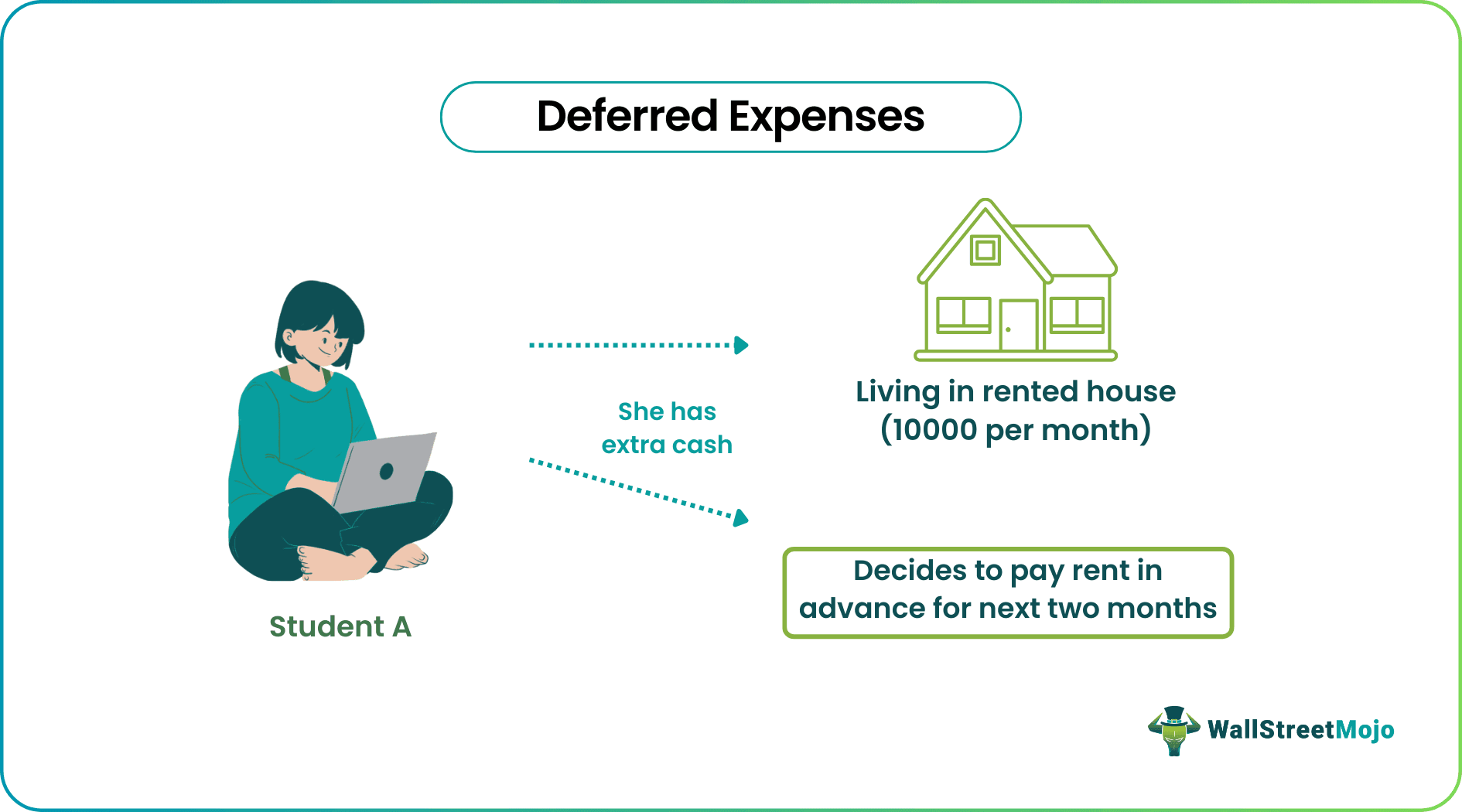

Example #1 - House Rent Expense

Let us assume that student A lives in a rented house, costing him INR 10000 per month. In June, he has extra cash of INR 20000 with him and hence, decides to pay the rent in advance for the next two months. In other words, he has already paid for the service (occupying the rented house), which he will consume (living in the house) in the coming months.

For the next two months, the expenditure of INR 20000 made will serve as an asset to the student as it is providing him with benefits. If the student were to record this advanced rent payment transaction of INR 20000 in his accounting books, he would label it as these “expenses,” and the same will appear as an asset on his balance sheet entries.

A month later, the "deferred expenses" head will be reduced from INR 20000 to INR 10000. It is because one-month service has already been availed out of two months of advances payment made. Now the asset is available only for next month and only INR 10000. And accordingly, an entry of 10000 will be made in the "expense" head as per double-entry booking accounting standards. Hence, the reduction in these "expenses" head.

Key learnings

- We can also extend the idea of the expenses to the financial statements of companies. The core idea to remember is that anything for which a company has already paid out and is now "entitled" to receive services, therefore, is recorded as "deferred expenses" and not "expenses." It is due to the difference in the timing of consumption of that service.

- Formally, the term “deferred expenses” is used to describe a payment that has been made, but it won’t be reported as an expense until a future accounting period. These expenses are reported on the balance sheet as an asset until it expires.

Example #2 - Consultancy Fee

A corporation is into the manufacturing of handbags and shoes. They plan to install a new manufacturing unit and have hired consultants and lawyers to do due diligence and make legal contracts. The consultation and legal fees total an amount of INR 2500000. Let us assume that this new manufacturing unit's life will be ten years.

The company will make an entire payment of INR 2500000 at the beginning of the project, i.e., the beginning of year 1. But it will not enter this amount entirely in the "expenses" head. Instead, it will "defer" the INR 2500000 to balance sheet accounts such as new project costs. The company will charge INR 250000 (INR 2500000 spread over ten years) for the new project costs yearly expenses

They will be using the newly installed production unit and earning revenues from it. The total expense is recorded as "deferred expenses" because it provides better treatment for matching the total expense of INR 2500000 to each period. Each period is a year, unlike the above example, where each period was a month.

Another example can be seen in insurance premium payments.

Example #3 - Insurance Premium

The insurance premium is paid in advance for accidental coverage in the coming months or years.

For instance, Company A pays the insurance premium for its office building. Premium payment is half-yearly. The total cost of insurance is INR 80000. Payments are made in June and December every year. In June, the company will pay INR 40000 for the insurance coverage until December. Instead, it has repaid in June an amount of INR 40000 for the service (insurance protection) it will consume over the next six months until the next due date for payment approaches. In this example, the company will record deferred expenses of INR 80000 as assets in the first year and expenses in the second year of accounting.

Deferred Expenses Explained in Video

Deferred Expense vs. Prepaid Expense

- While “deferred expenses” are sometimes referred to as “prepaid expenses,” there is a subtle difference in those terms. Strictly speaking, the two terms cannot be used interchangeably.

- When the time duration of the moratorium is less than a year, i.e., when the advance payment is made for future periods falling within a year, the expense is labeled as "prepaid expense." When the future payments are for periods more extended than one year, it is labeled as “deferred expenses.” The reason for this lies in the categorization of assets.

- We have already learned that prepayment of expenses is considered an asset for reporting purposes. When the asset created is for less than a year, it is termed as the current asset and is reported as a "prepaid expense. Similarly, when the asset created is going to last for more than one year, it is termed as a noncurrent (long-lived) asset and is reported as “deferred expenses.”

Recommended Articles

This article has been a guide to what is Deferred Expenses. Here we discuss deferred expenses, examples of House Rent Expense, Consultancy Fees, and Insurance Fees. Also, we discuss the differences between prepaid expenses vs. deferred expenses. You may also learn more about accounting from the following recommended articles –