Table Of Contents

Debt Issuance Definition

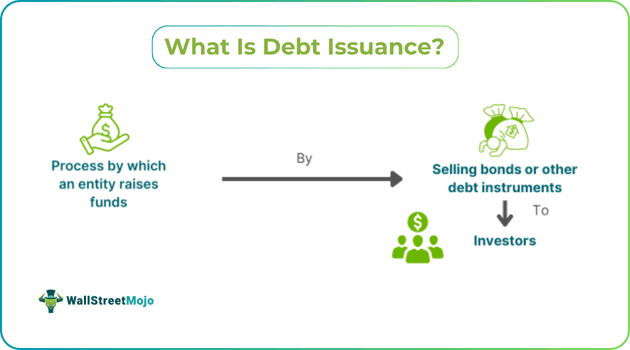

Debt issuance is the process by which governments, corporations, and other institutions secure funding for their operations and activities. It is a crucial aspect of an issuer's financing strategy and capital-raising efforts. Understanding this process provides valuable insights into the mechanics of debt financing.

Debt issuance plays a significant role in providing liquidity to the global economy and facilitating cross-border investments. It enables access to more significant amounts of funding, offers customizable terms and conditions, and helps predict the cost of capital. However, it also carries the risk of default, requiring careful consideration and management.

Key Takeaways

- The debt issuance process is the process of finding funding by organizations. These organizations may be companies or government institutions.

- The process comprises issuing debt instruments such as corporate bonds, government bonds, notes, and loans.

- They incur repayment risks but have many benefits. They provide liquidity and facilitate investments across borders.

- They help organizations expand, repay loans, and buy new assets.

- The issuance costs are amortized in accordance with the ASC standards. The process shall include the organization determining its goals, choosing the instrument

- Giving it to underwriters, creating a prospectus, credit rating, and pricing the offer.

Debt Issuance Explained

Debt issuance is the practice of companies or organizations raising funds to finance their operations or activities. This funding helps meet financial needs and obligations, supports expansion activities, facilitates the purchase of new assets, refinances existing debt, and sustains the organization during economic downturns. Debt financing is one method of funding, with equity financing being the other. Debt financing involves borrowing funds with the commitment to repay them later, typically with interest.

In exchange for the borrowed money, organizations make interest payments and eventually repay the principal amount. Before issuing debt, companies assess their financial position, seek advice from financial and legal advisors, and prepare necessary documentation. They also develop business plans, conduct due diligence, and identify and address potential risks. Developing an investment strategy is another critical step prior to debt issuance.

The type of debt issued must meet the diverse needs of both investors and issuers, varying in terms of returns, risks, and purposes. Examples include corporate bonds, government bonds, and municipal bonds. The debt issuance process involves creating, managing, and distributing these instruments. Key players in this process include issuers, investors, and underwriters who assist with advising, pricing, and marketing the securities.

Process

Given below are the steps involved in the issuance process:

- Determination of financial needs: Businesses, organizations, and governments assess their financial requirements to determine the amount of capital needed for purposes such as expansion, diversification, or repaying existing loans. This analysis considers working capital requirements, planned investments, and debt repayment obligations.

- Choosing the instrument: Institutions choose from options like bonds, commercial papers, loans, and notes based on factors such as interest rates, maturity, and risk profile. Companies may also have debt issuance programs to assist in this process.

- Selection of underwriters: Underwriters play a crucial role in structuring the offers and assisting in pricing and marketing the instruments to potential investors. They may even purchase the entire issue to resell it in the market, guaranteeing the sale of these instruments.

- Memorandum and prospectus: These documents provide essential information about the company and the instruments being offered, including issuer details, terms of the offering, risk factors, and other relevant information. This helps investors make informed decisions.

- Credit ratings: A credit rating agency rates the instruments, evaluating the associated risk based on factors such as repayment capacity, financial strength, and industry conditions.

- Pricing and marketing of the offer: Underwriters set the pricing based on rates, yields, and other factors. They then initiate a marketing campaign to attract potential investors. The pricing mechanism considers whether the issuance is short-term or long-term.

- Completion of legal requirements and issuance: Regulatory bodies impose various legal requirements, which differ by country. For example, in the U.S., the Securities and Exchange Commission (SEC) oversees compliance. Once regulatory compliance is achieved, the issuance occurs, and funds are raised. The issuer then receives the proceeds, whether for short-term or long-term debt issuance.

Examples

Let us look into some examples to understand the concept better.

Example #1

Imagine a company, ABC Ltd., a clothing company located in Nevada, USA. ABC Ltd. wants to expand to California to capture a new market and improve profits. To fund this expansion, the company decides to issue corporate bonds.

These bonds are issued at an interest rate of 8%, making them a high-yield debt issuance. Under this process, the company borrows a certain amount from bond buyers, who become creditors. ABC Ltd. pays interest to these bondholders for the duration they hold the bonds and repays the principal amount once the designated period is over.

Example #2

CPP Investments is an organization that operates globally in investment management and is part of the Canada Pension Plan Investment Board (CPPIB). It has issued green bonds to address climate change. The proceeds raised through these issuances finance investments, both equity and debt, in new or existing assets. The primary goal is to make long-term investments that accelerate the transition of energy consumption towards a lower-carbon economy.

How To Amortise Debt Issuance Cost?

An organization that issues debt incurs costs such as accounting, underwriting, and legal expenses. These expenses can be handled in accordance with ASC (Accounting Standards Codification) 340-10-S99-1 for accounting for debt issuance costs.

These costs include incremental costs and fees paid for the issuance process and those paid to third parties. However, they do not include costs paid to creditors or costs that would have occurred irrespective of the issuance.

Certain incremental costs directly attributable to the actual or proposed securities offered can be charged to the gross proceeds of the offerings. These costs can be deferred in this manner, but expenses such as administrative and general expenses and management salaries are not considered part of offering costs. Similarly, aborted costs cannot be deferred and charged against the subsequent offering's proceeds for the purpose of accounting for debt issuance costs.

Typically, issuance costs are amortized over the life of the debt instrument using the same period as the premium or discount periods. If the debt instrument is accounted for at fair value, issuance costs must be expensed immediately under ASC 825. ASC 835-30-35-2 requires the amortization of discount and premium of debt using the interest method. ASC 835-30-35-4 suggests the use of a straight-line method of amortization under certain conditions.