Table Of Contents

What Is Debt Collection?

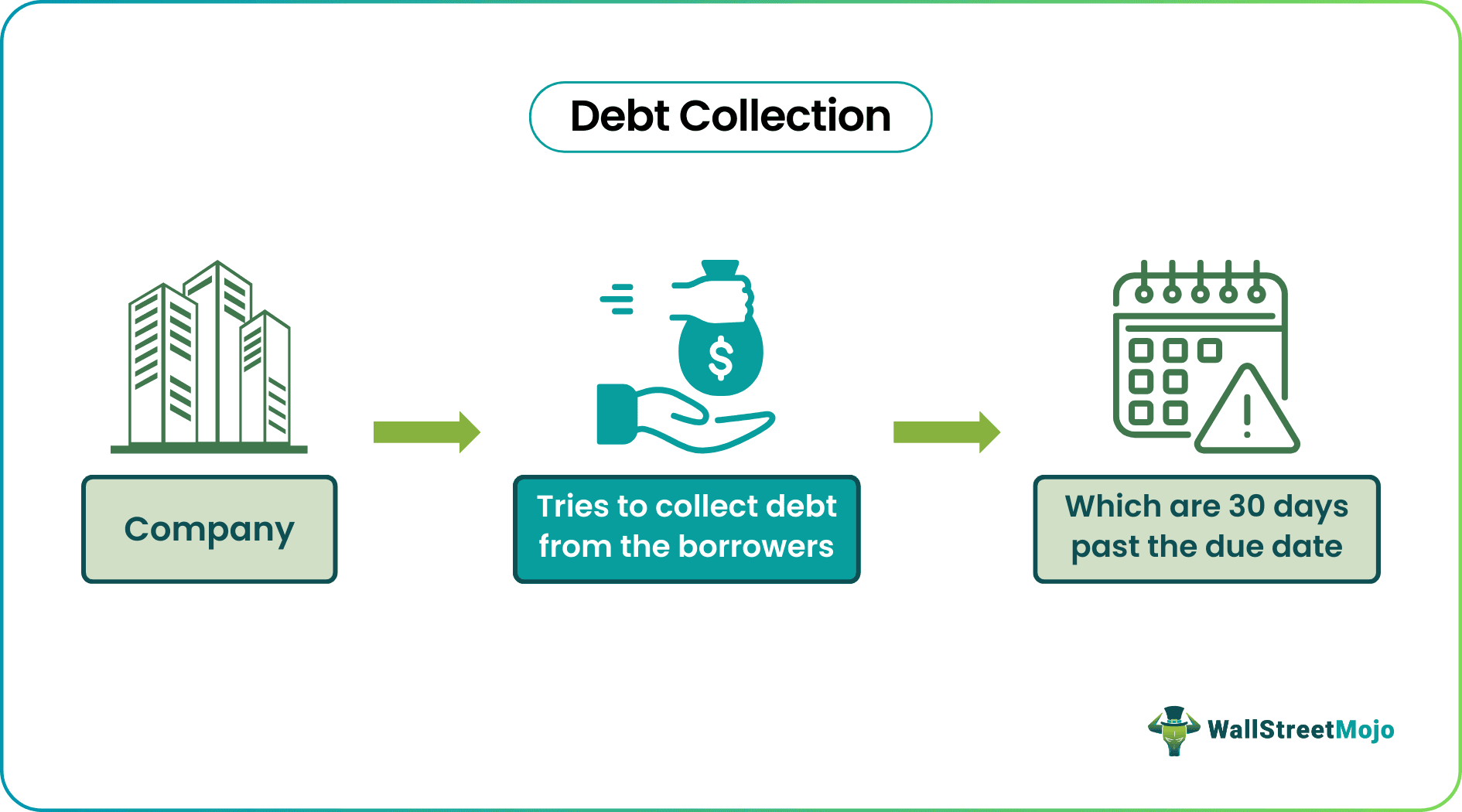

Debt collection is the practice of collecting debt from debtors and borrowers who have not made loan payments past the due date, generally after 30 days. The primary purpose of this is to recover funds owed to a creditor by an individual or business.

Debts can be of various types, such as credit card bills, personal loans, unpaid utility bills, student loans, car loans, etc. Unpaid debts can negatively impact the debtor's credit score. Although debt collection acts are a general procedure, many people experience it as threats and social harassment. The Fair Debt Collection Practises Act sets rules for this collection industry and shields consumers from unethical or demanding debt collectors.

Table of contents

- What Is Debt Collection?

- Debt collection is when borrowers are contacted to make loan payments by a debt collector once they are past the due date, typically after 30 days.

- It can be any debit, credit or loan from any bank or financial institution,

- A federal statute known as the Fair Debt Collection Practises Act (FDCPA) limits the activities of outside debt collectors who try to collect money owed to banks and other financial institutions.

- This process can involve various stages ranging from reminders and communication with the debtor to more formal actions, such as involving debt collection agencies or pursuing legal avenues.

Debt Collection Explained

Debt collection is a system or practice of collecting debts from the borrowers. When an individual applies for a loan, they are liable to repay the debt. They are required to repay with specific interest under guidelines. Hence, typically, it is a monthly payment system through which the borrower repays the debt in installments over the loan period.

Moreover, the loans can be of various types and natures, including home loans, education loans, personal or business loans, car loans, credit card bills, or utility payments. When a borrower fails to repay the installments, the bank waits for a certain period, generally 30 days. Therefore, a debt collector from the bank's loan department contacts the borrower either by a letter, a formal notice, or an informal phone call.

In case the debtor fails to repay the contract. The calls and letters become frequent, leading to warnings of repayment. Hence, if the borrower communicates well, negotiates, or tries to settle the debt, it starts getting back to normal. However, in the worst-case scenario, the bank has the right to sue the debtor and take legal action against them, taking them to court.

Furthermore, in modern banking scenarios, banks appoint third-party debt collection agencies. Once the bank sells a borrower's account to these companies, the firm starts operating on behalf of the bank. However, they do so in their ways, which are harsh, insulting, and may embarrass the borrower. Sometimes, borrowers appoint debt collection lawyers to deal with these third-party agencies. If the collection agency successfully retrieves the debt, it is offered a commission, which is a percentage of the loan amount. Additionally, a borrower must ensure they are creditworthy to pay and make sure to settle debts to avoid any consequences, especially when it concerns the financial aspect.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Examples

Let us understand the concept better with the help of examples. -

Example #1

Imagine Arthur, who has accumulated credit card debt over several months due to unexpected medical expenses. Despite initially managing the minimum payments, he eventually faces financial hardship and finds it challenging to meet the monthly obligations. As a result, the credit card account becomes delinquent, triggering this process. The credit card issuer, in an attempt to recover the outstanding amount, may start by sending reminder notices and making phone calls to the debtor.

If these efforts prove unsuccessful, the credit card company might decide to enlist the services of a professional collection agency. This agency, acting on behalf of the creditor, would then intensify efforts to communicate with the debtor, employing various strategies to secure repayment. While this serves the purpose of recovering funds owed to creditors, such processes need to adhere to legal and ethical guidelines to ensure fair treatment of the debtor. Additionally, the impact on the individual's credit history highlights the broader consequences of unresolved debts in personal finance.

Example #2

The Consumer Financial Protection Bureau (CFPB) issued a report indicating that American households face enormous challenges when debt collectors pursue them for allegedly unpaid medical bills. Over 8,500 complaints were filed in 2022 alone by servicemembers, adults, and other consumers regarding medical debt collection.

In order to shield small companies from unfair and dishonest practices, the CFPB reports to Congress on the Fair Debt Collection Practises Act. This report includes updates on these markets and includes information from other agencies like the Federal Trade Commission. Because the practice is so widespread, debt collection organizations pursue tens of millions of people for unpaid medical bills, even though the bills are actually erroneous.

How To Deal?

Tips for dealing with debt collection are –

- The first step or tip for dealing with these processes or agencies is always to communicate and remain calm.

- Request written validation of the debt from the collection agency. Hence, this should include details such as the original creditor, the amount owed, and the verification process.

- Never avoid debt collection letters, notices, warnings, or phone calls; doing so will cause the collector to assume the debt is bad.

- A customer must always know their rights and shall know how to use them at times.

- When starting to settle debt, an individual may still need to get the total debt amount ready but should always try to minimize it.

- Read and collect information regarding the debt collection process, understanding the fees, charges, and interest rates the bank has included in the debt.

- Moreover, the borrower can try negotiating with the banks to come up with a proper repayment plan that they can oblige to.

- A debtor may send a cease and desist letter to the banks asking them to stop contacting them; it is a provision under FDCPA.

Importance

The importance of debt collection is -

- It works as a tool to collect the debt from the borrowers that they are legally liable to pay back.

- The whole system ensures that banks and financial institutions that help people with funds can receive their money back with all the charges and fines.

- Here, the process involves record keeping, communication, recovery, and legal compliance and obligations, including the data analysis of borrowers.

- Not every borrower needs to repay and have loyalty toward their financial liabilities; this process helps in identifying them and recovering funds.

- Without the debt collection process, there is no guarantee that the borrower will repay and the funds will be recovered.

- Debt collection works for both lenders and borrowers and allows them certain rights.

- Without collecting debt, a bank or lending institution may incur a loss with no proper timeline for recovery.

Difference Between Debt Collection and Debt Recovery

The main distinguishing factors between debt collection and debt recovery are -

- Debt collection is the in-house process of banks and lending institutions to collect debts from their customers. In contrast, debt recovery is when a bank, after sufficient tries, is unable to retrieve the debt and appoints a third party for the collection.

- Most banks have debt collection departments with proper employees and staff. In comparison, debt recovery is done by debt collection agencies that work independently; some may also be attorneys.

- In-house banks only offer salaries to their employees in the debt collection department. Still, in the case of debt recovery, the collection agencies charge a commission, particularly a certain percentage of the debt amount they collect.

- This has its time frame and a polite modus operandi since it is in-house, but when it leads to debt recovery, the collection agencies harshly deal with borrowers.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

Yes, if the debtor consistently resists the calls and visits of the debt collector or, for some reason, is unable to make payments, the debt collector has the right to sue them. It is the worst-case scenario, followed by a formal legal notice, and the borrower will be summoned to the court.

Yes, once a bank or financial institution sells the debtor's loan account to a debt collection agency, it can be reported separately on the individual's credit report, significantly affecting their credit score. The collection starts to appear on the report from different unsecured accounts, and the debtor can only remove it in two ways: waiting for seven years in case the information is valid or filing a dispute if the information is inaccurate.

In general, debt collection fees are not tax-deductible for individuals. Personal debts, such as credit card balances or personal loans, are considered personal expenses and are typically not eligible for tax deductions. The Internal Revenue Service (IRS) does not allow deductions for fees paid to collect personal debts.

Recommended Articles

This article has been guide to what is Debt Collection. We compare it with debt recovery, and explain how to deal with it, its examples, and importance. You may also find some useful articles here -