Table Of Contents

What Is The Credit Utilization Ratio?

Credit utilization ratio or rate is the percentage of the revolving credit consumed by a borrower from their total available credit. It contributes to determining an individual's credit score by the credit bureaus. Therefore, the purpose of this rate is to provide lenders with an indication of a person's creditworthiness and ability to manage credit responsibly.

An ideal credit utilization ratio is up to 30% or lower; however, a zero rate is equally bad for a borrower's credit score. Thus, this ratio indicates the borrower's efficiency in debt management. The two prominent revolving accounts requiring this ratio evaluation are home equity lines of credit (HELOC) and credit cards. Therefore, a high credit utilization rate negatively impacts a borrower's credit score.

Table of contents

- What Is The Credit Utilization Ratio?

- The credit utilization ratio measures the rate of revolving credit exhausted from the total credit limit available to a borrower.

- It is used for ascertaining the borrower's debt management concerning revolving accounts like credit cards and home equity lines of credit (HELOCs).

- It is a significant contributor to the credit score modeling, I.e., a higher ratio may negatively impact the borrower's credit score.

- An ideal credit utilization rate is either 30% or lower; a ratio more than this may increase the borrower's cost of credit or interest rate.

Credit Utilization Ratio Explained

A credit utilization ratio meaning is a crucial contributor to the credit score analysis of a borrower. It is typically expressed as a percentage. Furthermore, lenders and credit reporting agencies use this rate as one of the factors in determining a person's credit score.

Therefore, a revolving credit utilization ratio is an account open for repetitive borrowings and payments by the holder. For instance, it is commonly applied to credit cards. The credit utilization ratio is the overall rate of revolving credit the cardholder uses from the total available limit of all the credit cards. Similarly, this ratio is also used for home equity lines of credit (HELOCs).

Besides, to maintain an ideal credit utilization ratio, a borrower can,

- Pay his bills on time

- Keep their balances low

- Avoid opening too many new credit accounts at once.

Hence, this ratio is used alongside the debt-to-equity ratio for gauging a borrower's credit score. The debt-to-equity ratio figures out a borrower's repayment ability. In contrast, a high revolving credit utilization ratio indicates a higher risk of bad debts or non-repayment of credit, which decreases the borrower's credit score.

Likewise, a higher credit utilization rate also results in the difficulty of availing of credit and increases the cost of credit for the borrowers. On the other hand, a low credit ratio implies that the person is using credit responsibly. Therefore, they are more likely to be able to make their payments on time. Thus, maintaining an optimal credit utilization ratio indicates to lenders that one is using their credit responsibly and are not relying heavily on credit.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

How To Calculate?

The credit utilization ratio is calculated by first summing the limits of all the credit cards, i.e., the total credit card limit available. Then, divide the total credit availed or debt by the total credit limit (as computed earlier) and multiply the result by 100 to convert it into a percentage value.

The formula is:

Credit Utilization Ratio = (Total Debt or Outstanding Amount / Total Available Credit Limit) * 100

Let us summarize the computation of the credit utilization rate into the following steps:

- Find the sum of all credit card balances or outstanding amounts.

- Determine the sum of all the credit cards' limits.

- Divide the total outstanding amount by the total credit limit available.

- Convert the value into a percentage by multiplying it by 100.

Examples

Let us now work out some examples of evaluating the credit utilization rate:

Example #1

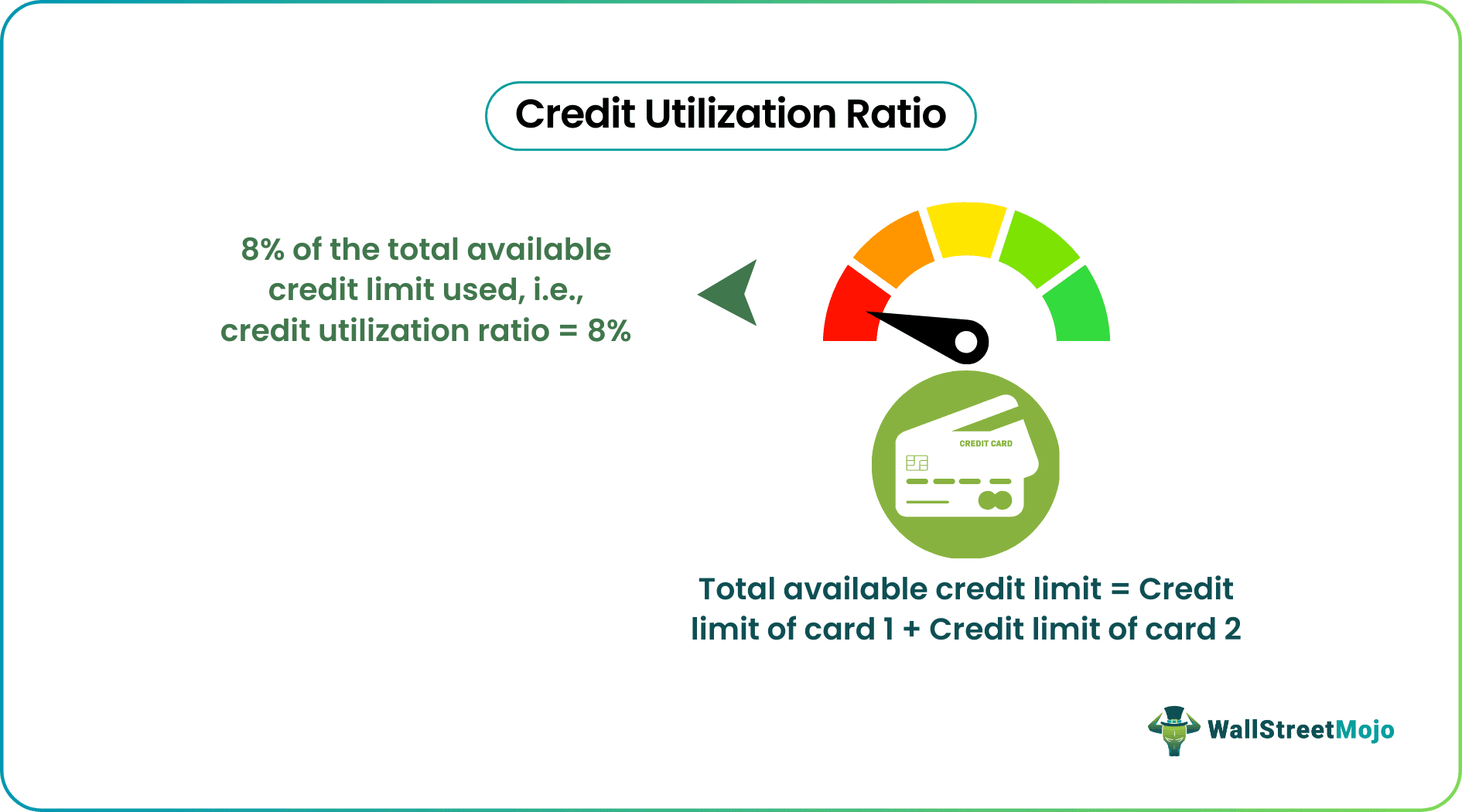

Suppose a borrower has the following credit card balances and limits:

| Credit Card | Credit Card Balance | Credit Card Limit |

|---|---|---|

| A | $100 | $1000 |

| B | $180 | $2000 |

| C | $340 | $5000 |

| D | $180 | $2000 |

| Total | $800 | $10000 |

Credit Utilization Ratio = (Total Debt or Outstanding Amount / Total Available Credit Limit) * 100

= ($800 / $10,000) * 100 = 8%

Example #2

Suppose a HELOC account holder has a total outstanding amount of $180,000 out of the total credit limit of $300,000. Find the credit utilization rate before and after the borrower makes a payment of $40,000.

Before:

Credit Utilization Ratio = (Total Debt or Outstanding Amount / Total Available Credit Limit) * 100

Credit Utilization Ratio = ($180,000/ $300,000) * 100 = 60%

After:

Total Outstanding Amount = $180,000 - $40,000 = $140,000

Credit Utilization Ratio = (Total Debt or Outstanding Amount / Total Available Credit Limit) * 100

Credit Utilization Ratio = ($140,000/ $300,000) * 100 = 46.67%

How To Lower/Improve?

Sometimes a borrower has a higher ratio than 50%, which is a warning sign that the borrower is overspending and may be charged higher interest than those with a lower percentage.

Therefore, this ratio is crucial for calculating a borrower's credit score. Even the creditors prefer lending to borrowers with a favorable credit and payment history and maintaining a good credit score.

A borrower can adopt the following measures to improve or decrease their credit utilization ratio:

- Pay off or pay down debts: Pay off the total outstanding amount or lower the dues by making partial payments. Since piling up the debts will unnecessarily increase the rate.

- Do not close revolving accounts: Closing the credit card or HELOCs account may adversely affect the borrower's credit score. So it is better to continue with these credit accounts while keeping credit utilization low.

- Use multiple credit cards: A borrower can use more than one credit card to enhance purchasing power and keep the credit utilization rate favorable.

- Request a higher credit limit: Another option is to ask the credit issuer to increase the credit limit to lower the ratio.

- Make several payments: If the borrower pays off in multiple installments during the same billing cycle, the ratio lowers significantly.

- Pay before the end of the billing cycle: Paying at the right time is equally crucial since if the dues are cleared on the closing of the billing cycle, the change will show up early in the credit utilization ratio.

- Consolidate debt with a personal loan: The borrower can also ask the credit issuer to convert their debt into a personal loan to keep the credit utilization low.

Hence, credit card companies or issuers often evaluate the credit card balance at the end of every month, I.e., at the closing of a billing cycle. Thus, it takes time for the server to show the current credit score if a borrower makes the payment at the beginning of the mid-month.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

The best credit utilization ratio is considered to be 10% but even 30% or lower rate and a ratio higher than 0% is good for the borrower's credit score. Thus, this rate should neither be too high nor be nil; however, it is advisable to keep this ratio as low as possible to strengthen the credit score.

The credit utilization rate is a crucial factor behind the credit scoring model. Thus, this ratio contributes around 30% to the borrower's credit score evaluation through Fair, Isaac, and Company (FICO).

No, these ratios are explicitly applied to revolving credit accounts, such as credit cards and lines of credit. It does not apply to installment loans like auto loans or mortgages. However, maintaining a better ratio on your revolving credit accounts is still essential for overall credit health.

Recommended Articles

This article has been a guide to what is Credit Utilization Ratio. We explain how to calculate it, how to lower/improve it, & its examples. You may also find some useful articles here -