The following table lists the differences between credit and cash transactions occurring in the due course of business:

Table of Contents

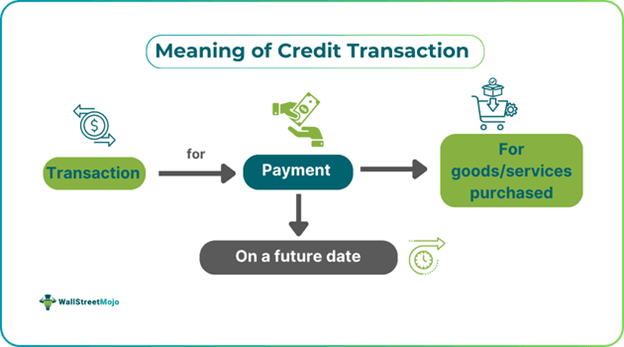

Credit transactions are types of transactions in which a customer receives goods (or services) before and makes payment later. The sole purpose of this transaction is to use the product first and then enable payment of goods at a future date.

Credit transactions offer advantages for both businesses and credit card issuers. Here, the supplier may provide their goods to businesses under a hire-purchase agreement and facilitate receipt of the supplied goods in the future. As a result, customers can also experience the product without worrying about the payment. However, there are certain limitations to this transaction for the creditor.

Key Takeaways

A credit transaction is a business transaction where the payment (receipt), goods, or services do not happen on the day of purchase or sale. Instead, it happens on a future date, which can extend to weeks or months. It provides comfort for the buyer to enjoy the goods at their ease. So, if a person had bought electronic goods from a wholesaler, the former receives a credit discount on the purchase. The retailer can later make the payment within a stipulated period. However, any delay in payment after the credit period can lead to interest charges.

In businesses, consumer credit transactions occur on a usual basis. Such transactions are enabled when procuring raw materials from suppliers or selling finished goods at credit. In exchange, the creditor (business or company) may supply a bill of exchange or note receivable. It details the amount owed, credit period, and interest charges applicable, if any. Within the credit period, the buyer (of goods or services) must make the due payment to the concerned creditor (or seller). Similarly, individuals also use consumer credit transactions for personal lending to friends, family, or household needs. Here, the debtor (consumer) may repay the amount due in installments.

Furthermore, these original credit transactions are also a significant component of credit cards like Visa and Mastercard. OCTs enable fund transfers from the company's business account to the credit card holder's account. They experience convenience in making purchases on online channels. Also, there is no risk of losing money in this entire process. As a result, the original credit transaction is a tool for loading money and letting borrowers spend whenever needed.

Let us look at some examples of how businesses utilize the advantages of credit transactions:

Suppose John is a business owner who sells maple juice to many customers. He has a wholesale business that allows large corporations to use his product as a raw material for other products. To date, he has maintained around 15 clients who deal in large quantities. Also, to boost his client relationships, John enables credit transactions where clients can purchase maple syrup orders and later make payments. After 20 days, most clients typically make their payments. If a payment is missed, John issues a reminder to ensure timely collection.

According to news published in November 2024, the Bastrop County Sheriff's Office reported many fraudulent credit and debit transactions at the hardware stores. There were multiple reports registered by people living on the outskirts pertaining to such transactions. When store employees asked for customer proof, the latter gave fake IDs, which eventually allowed them to make large purchases and steal financial information. As a result, the Sheriff advised stores to avoid over-the-phone payments for large purchases and implement in-person verification to mitigate risk to its maximum.

The following table lists the differences between credit and cash transactions occurring in the due course of business:

| Basis | Credit Transactions | Cash Transactions |

|---|---|---|

| 1. Meaning | It refers to all those transactions where payment (or receipt) is made after receiving goods and services. | These transactions enable immediate payment (cash) to the seller at the time of purchase. |

| 2. Timing of payment | It is delayed, most often made after weeks or months. | Here, payment is made immediately to the supplier. |

| 3. Accounting effect | Such transactions act as a liability (accounts receivables) for the business until recovered. | These transactions are directly recorded as cash sales for the business. |

| 4. Risk | Here, customers may default on payment, causing potential risk to the seller. | There is no such risk here. |

| 5. Interest charges | After the credit period, interest is charged to the due amount to the customer. | Since payment happens immediately, there is no chance of an interest penalty. |

Let us look at the pointers that explain the differences between credit and debit transactions below the provided table:

| Basis | Credit Transactions | Debit Transactions |

|---|---|---|

| 1. Meaning | It refers to transactions where payments occur in the later stage. | Debit transactions enable immediate deduction in the cash lying in the account. |

| 2. Balance sheet effect | Such transactions increase the liabilities of a company or individual. | These transactions often cause a deduction in the cash balance. |

| 3. Accounting treatment | They appear on the right side of the Profit & Loss (P&L) account. | They reside on the left side of the P&L account. |

| 4. Purchases | There is no urgent cash required to make purchases. | Entities must own enough cash to make relevant purchases, or else they may fall. |