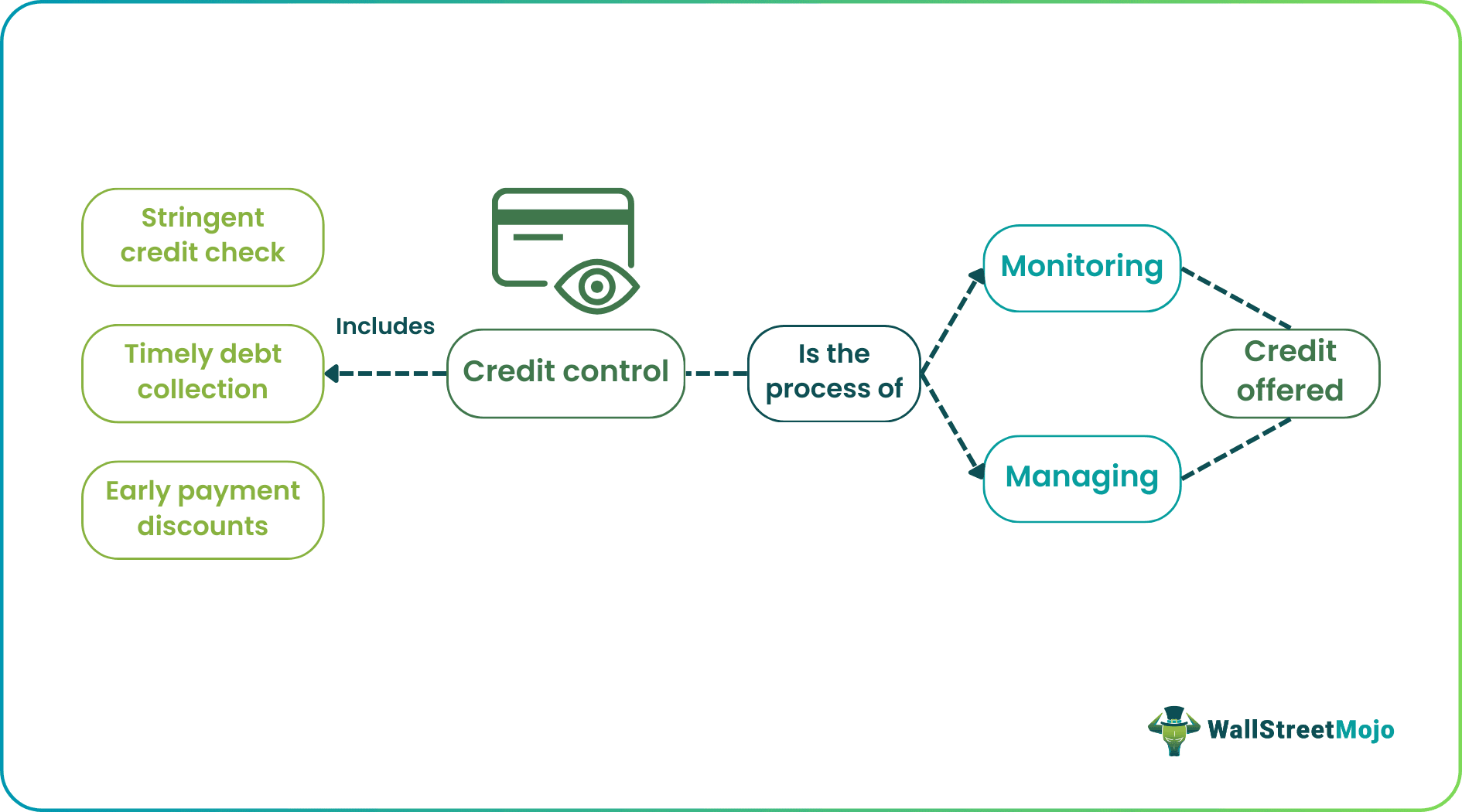

What Is Credit Control?

Credit control can be defined as a process of monitoring and managing credit offered to customers to minimize the risk of bad debt, late payments, and cash flow problems. its purpose is to ensure effective credit management as it is essential for any business to ensure a smooth flow of cash and maintain financial stability.

Credit control is used by a team who assigns a credit limit to the customer, which reflects their risk profile and ability to pay. This helps to manage credit risk and prevent potential bad debt. It is essential for managing credit risk and ensuring timely customer payment. By implementing a credit control policy, companies can reduce their exposure to bad debt and improve their financial health.

- Credit control is the process of monitoring and managing credit offered to customers to minimize the risk of bad debt and ensure timely payment.

- Effective credit control requires a robust credit management system with policies, procedures, and tools to monitor and control credit.

- Credit control methods include credit checks, setting credit limits, regular monitoring of accounts, debt collection procedures, and offering discounts for early payment.

- Credit control helps improve cash flow, reduce bad debt, and maintain financial stability. However, it may also result in reduced sales and higher.

Credit Control Explained

Credit control is a financial management strategy businesses use to manage credit risk and ensure timely payment from customers who purchase goods or services on credit. It involves implementing policies and procedures to evaluate customers’ creditworthiness, setting limits, and monitoring and controlling outstanding receivables.

It starts with a credit check, which is a process of evaluating a potential customer‘s creditworthiness. This involves reviewing the customer’s credit history, payment behavior, financial statements, and other relevant information to determine their ability to repay any credit.

Controlling involves setting credit limits, assessing customers’ creditworthiness, monitoring payment patterns, and taking corrective actions to reduce credit risk. Its primary goal is ensuring the business is paid on time and avoiding bad debt. Effective credit control requires a robust credit management system, which includes policies, procedures, and tools to monitor and control credit.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Methods

There are various methods of controlling credit, including:

- Credit checks and assessment of creditworthiness

- Setting credit limits and payment terms

- Regular monitoring and review of accounts

- Use of credit reference agencies

- Debt collection procedures

- Negotiating payment plans

- Offering discounts for early payment

Examples

Let us have a look at the examples to understand the concept better.

Example #1

ABC Corporation is a distributor that offers credit to its customers. To manage credit risk and ensure timely payment, the company has implemented a credit control policy that includes credit checks, credit limits, and regular reviews.

When a new customer applies for credit, the credit control team performs a credit check to evaluate their creditworthiness. Based on the results, the team assigns customers a credit limit, reflecting their risk profile and ability to pay.

During the year, ABC Corporation sells goods on credit to its customers. However, there are instances where customers exceed their credit limit or fail to make timely payments. To address these issues, the credit team reviews customer credit scores and adjusts credit limits as needed.

ABC Corporation can manage credit risk and prevent potential bad debt by implementing a policy. This helps to improve the company’s cash flow and overall financial health.

Example #2

XYZ Enterprises is a wholesale distributor that extends credit to its customers. To minimize credit risk and improve cash flow, the company has implemented a credit policy that includes credit scoring, credit limits, and periodic reviews.

At the start of the year, XYZ Enterprises has outstanding receivables of $1,000,000 from customers. Credit scoring is used to assign a score to each customer, and credit limits are set accordingly, with a maximum of $100,000. This helps to manage credit risk and prevent potential bad debt.

During the year, XYZ Enterprises sells goods on credit and collects $950,000 from customers. However, $50,000 of overdue receivables still exceed credit limits or are past due. To address this, the control team reviews customers’ scores periodically and lowers borrowing limits for high-risk customers.

At the end of the year, such a control policy has helped to mitigate risk and improve cash flow. Also, the company has reduced its exposure to bad debt and collected more outstanding receivables. Thus, the cost of implementing the control policy outweighs the benefits of lower bad debt and improved financial stability.

Advantages And Disadvantages

#1 – Advantages

- Improved cash flow and financial stability.

- Reduced risk of bad debt.

- Improved customer relationships through prompt payment.

- Increased efficiency in debt collection.

#2 – Disadvantages

- Reduced sales as a result of strict credit policies.

- Higher administrative costs associated with credit management.

- Potential damage to customer relationships due to strict credit policies.

- Difficulty in balancing credit control with sales growth.

Credit Control vs Accounts Receivable

- Credit control manages an organization’s credit to customers, including setting credit limits and collecting payments. On the other hand, accounts receivable is the total amount of money customers owe the organization at any time.

- Controlling is a proactive process before debts are incurred, while accounts receivable is a reactive process after a debt is incurred.

- Credit control manages customers’ credit terms, while accounts receivable is used to track and collect customer payments.

- The former helps mitigate debt and increase the chances of receiving payment, while accounts receivable helps businesses track debt and collect payments.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1.What is selective credit control?

Selective credit control is a method central banks use to regulate the flow of credit to specific sectors of the economy. It involves imposing credit limits or restrictions on certain industries or groups to control inflation or prevent economic instability. Selective control is often used with other monetary policies, such as interest rate adjustments or reserve requirements.

2.What is credit control area in sap?

In SAP, a credit control area is an organizational unit that manages and controls customer credit limits. A set of credit parameters, such as credit limit, risk category, and payment terms, defines it. This area is usually linked to a company code and can be used to manage credit limits for customers across different sales areas or regions.

3.What is a credit control clerk?

A credit control clerk is an administrative professional responsible for monitoring customer accounts, assessing creditworthiness, and following up on late payments. They work in a company’s finance or accounting department and play a critical role in ensuring the timely receipt of payments and minimizing bad debt. The duties of a clerk include reviewing credit applications, setting credit limits, sending reminders and collection letters, negotiating payment plans, and reporting on account status.

Recommended Articles

This has been a guide to what is Credit Control. We explain its methods, examples, advantages & disadvantages, and comparison with accounts receivable. You can learn more about accounting from the following articles –