Table Of Contents

What Is Credit Card Processing Fee?

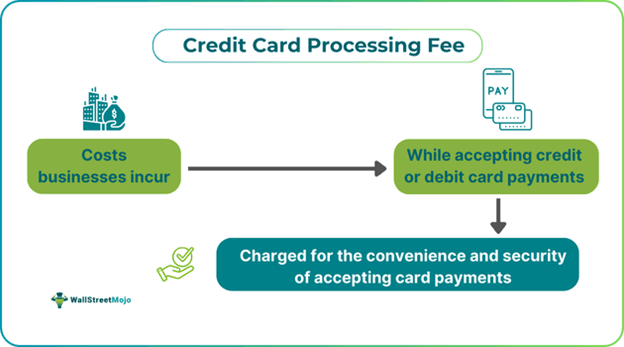

Credit card processing fees are expenses that businesses incur when they accept credit or debit card payments from their customers. The concerned entities levy this fee on businesses in exchange for the security and convenience associated with credit card transactions.

These fees are levied by the organizations participating in a transaction, such as the company that processes payments, the credit card networks, and issuing institutions. They include several kinds of expenses, like safeguarding against fraud, maintenance of the payment network, and the risk involved with lending.

Investors seeking a comprehensive platform may consider Saxo Bank International for a variety of account types and investment options.

Key Takeaways

- Credit card processing fees are the charges that businesses incur when they authorize and complete transactions using credit cards.

- Businesses must pay a fee each time a customer uses a credit card to make a purchase.

- This is a fee that the relevant entities charge businesses in return for the safety and accessibility of credit card transactions.

- The sum that a business is liable to pay will be based on several factors, including all the financial institutions involved, such as credit card issuers, banking institutions, and payment processing organizations.

Credit Card Processing Fee Explained

Credit card processing fees are the expenses that businesses pay to authorize and finish credit card transactions. Businesses are required to pay an amount every time a customer uses a credit card to make a transaction. These costs can vary depending on the type of credit card, and they consist of three distinct levels of charges:

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

- Interchange fees: These are also known as swipe fees or discount rates and are paid directly by businesses to the credit card provider.

- Payment processing fees: The payment processor may impose an extra fee for handling the transaction.

- Assessment Fees: These fees are paid to the credit card network to allow the transaction to be processed.

The amount a business owes will be based on several criteria and the different financial organizations involved in the transaction. These may include credit card providers, issuing financial institutions, and payment processing companies. However, these processing fees may substantially increase a business's overall expenses and significantly impact its earnings.

For efficient cross-border payments, many individuals and businesses use the Wise Money Transfer UK or Wise Money Transfer US services for transparent and low-cost transfers.

Types

The types of this fee are as follows:

- Tiered pricing: This type of pricing varies depending on the tier or bucket in which the transaction occurs. For instance, some qualifying transactions are subject to a reduced rate, while others necessitate a higher fee. This form of pricing is often ideal for businesses that conduct the majority of their transactions in the lowest tier.

- Flat rate pricing: In this pricing arrangement, the credit card processor charges the business a predetermined percentage of each transaction and a minimal per-transaction fee, which is generally $0.20 to $0.30 per transaction. Flat rate pricing makes it simple for businesses to forecast their credit card processing expenses in advance.

- Interchange Plus pricing: This pricing model requires businesses to pay the interchange rate for each transaction and previously established add-on charges. The extra charges may be an additional percentage or minimal fee for each transaction.

How Much Do Credit Card Networks Charge For Processing Fees?

Some major credit card networks and the processing fees they charge have been discussed below:

| Credit card network | Processing fee range |

|---|---|

| American Express | 1.43 percent + $0.10 to 3.30 percent + $0.10 |

| Discover | 1.40 percent + $0.05 to 2.40 percent + $0.10 |

| Mastercard | 1.15 percent + $0.05 to 2.50 percent + $0.10 |

| Visa | 1.15 percent + $0.05 to 2.40 percent + $0.10 |

How To Calculate?

The effective rate is the easiest approach to determining how much an organization pays for credit card processing. It is determined by dividing the total sales by the total fees for a specific cycle.

Effective rate = (Total amount deducted for processing / Total monthly sales) x 100

Examples

Let us have a look at the following examples to understand this concept:

Example #1

Let us assume that Jake owns a business and wants to calculate the credit card processing fee for one month. The net total processing fees for the month are $7000, while the overall sales of the business were $110,000.

Using the effective rate formula,

Effective rate = (Total amount deducted for processing / Total monthly sales) x 100

- = ($7000 / $110,000) x 100

- = 7%

An effective rate of around 3% for credit card processing is considered good. If a business pays around 3.5% or more, then its effective rate may be too high. In this case, the effective rate is 7%, which is considered high.

Example #2

Visa and Mastercard have reached an arrangement with retailers in the United States to reduce credit card processing fees in the near future. The arrangement will allow businesses to impose surcharges on cards with higher swipe fees. As a result, using a premium card with a high rewards program may become more costly. Some have claimed that these developments might impact credit card benefits or enable businesses to offer savings to customers.

How To Offset?

Some ways to offset these fees include the following:

- Bargaining charges with credit card processors: A higher number of transactions makes it more likely that a processor will recognize a company's worth as a merchant and wish to do business with it. If there is a higher volume of transactions each month, a business may convince the processor to decrease the charges.

- Swiping as often as possible: The more a business can reduce non-present transactions, the lower the risk it provides to the processor. Limiting the number of transactions that are paid for using physical cards and authenticating the transaction with an extra layer of security verification helps. As a result, businesses may help reduce the risk that both parties bear, which means they are likely to be charged less processing fees.

- Employing an address verification service: This process verifies the cardholder's billing information with the issuer. Many processors compensate merchants that employ such systems by offering reduced interchange fees.

Want a smarter way to bank on the go? Revolut offers a user-friendly app with global access, crypto and stock trading, and innovative budgeting tools—all in one powerful platform.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.