Table Of Contents

What Is Credit Card Churning?

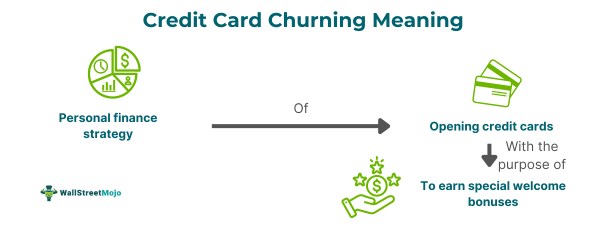

Credit card churning refers to a personal finance strategy involving continuous closing and opening of credit cards in order to earn special benefits and welcome bonuses. It helps users collect dividends like maximum miles and points every year for redeeming as hotel bills and flights.

Some customers find it lucrative because they have excellent management skills, a deep understanding of the bonus rules of every bank, exceptional money and credit habits, and its application. Card issuers find it risky and often attach red flags to it. It does not lead to bad credit scores, debt, or bankruptcy.

Investors seeking a comprehensive platform may consider Saxo Bank International for a variety of account types and investment options.

Key Takeaways

- Credit card churning means a finance strategy that involves regularly opening & closing credit cards to earn special benefits and bonuses redeemable for hotel bills and flights.

- It affects credit - negatively new card applications plus approvals due to hard inquiries and positively when credit limits increase.

- It is prevented by using Chase 5/24 rules, disqualifying past bonuses, offering single intro bonuses, limiting card usage, and using lifetime one-card rules.

- It allows you to earn significant miles and credit card points obtained by daily expenditure but tends to rack up many credit card debts due to the additional credit available.

How Does Credit Card Churning Work?

Credit card churning meaning could be understood as the strategy by intelligent people to avail of new credit card facilities in succession to earn introductory awards from banks or card issuers. Certain people have become so expert at leveraging the intro bonus system that they have earned enough rewards to fund free hotel stays, plane tickets, and shopping benefits. Although legally valid, it has become controversial, leading to repercussions for cardholders who use it by banks or card issuers.

Its entire work is based on opening numerous credit cards during the current financial year by account holders in a short period. It is done at such a speed that allows full exhaustion of the threshold to get a welcome bonus. The below circumstances come under card churning:

1st situation: Applying for exactly similar cards multiple times to collect a huge welcome bonus associated with that card and then cancel it after earning the full bonus.

2nd situation: It involves submitting a credit card application, getting it approved, fulfilling the minimum spending requirements within a certain fixed time, then receiving a huge welcome bonus, and finally canceling before the due date of the annual fee payment.

3rd situation: By using the App-o-rama process in the context of miles and points, applying for numerous fresh credit cards at once, and repeating the application procedure every few months or so. It gets repeated till new cards are in stock and the applicant meets the minimum required spending to claim the bonus on every card.

It results in earning hundreds or thousands of points or miles every year. These points or miles can be redeemed for free hotel bookings, flight ticket bookings, and sometimes shopping products.

For efficient cross-border payments, many individuals and businesses use the Wise Money Transfer UK or Wise Money Transfer US services for transparent and low-cost transfers.

Examples

Let us use a few examples to understand the topic.

Example #1

An online article published on 30 August 2022 discusses the harms of churning credit cards. This practice consists of subscribing to multiple credit cards to earn significant bonuses and then canceling these cards to bypass fees. However, with risks comes the danger of possible debt, like spending $10,000 in three months through a Citi Premier Visa card of 15,000 miles, putting huge strains on the budget.

Besides, annual fees of $4,000 over the $2,000 budget trigger a 25% interest rate charge. Therefore, the user has to face $245 interest on credit to earn $150 in miles. Furthermore, the frequent turning may even damage credit scores, leading to bank fines.

Example #2

Let us assume Josh decides to magnify his credit card rewards using card churning. He applies for the same in his bank for an Old York credit card, providing 50,000 bonus points on signup and another 50,000 bonus points on spending $10,000 on shopping. As a result, he gets his card approved, starts spending the desired level of amount and accumulates 100,000 points during the year.

However, just before the card's renewal, Josh canceled it and skipped paying its annual renewal fee. Now, he applied for the next card with a similar facility and got large bonus points to be redeemed for his hotel stay on vacation to New York City.

Effect On Credit

Every time one applies for a new credit card, it affects their credit score as follows:

- When applying for a new card, the bank must make a hard inquiry, which negatively impacts credit scores on several levels.

- On approval of a new card, it increases the total credit limit available to an applicant user.

- It also leads to changes in credit utilization, thereby increasing one's credit score.

- Avery's newly approved credit card account decreases the average age of accounts, impacting the credit score per card applied.

- If any of the approved cards miss their payment on time, then any late payment negatively impacts the credit score.

How Banks Prevent Credit Card Churning?

Over time, banks and credit card issuers have become aware of the manipulation of credit card awards by users. Hence, banks and credit card issuers have taken certain measures to prevent it, as shown below:

- New rules, such as the Chase 5/24 rule have been created concerning getting new credit cards and earning rewards.

- Certain banks have introduced one card for lifetime rule like American Express.

- Some banks disqualify the earning of the same type of bonus if it has already been received in the past.

- Others have started the rule of a single intro bonus for a new card.

- Some have applied the intro bonus in a specific time frame to a group of cards belonging to the same regards scheme.

- A few banks permit cardholders to only use two cards at a time.

Pros And Cons

Let us check out some pros and cons of the said credit card manipulation using the table below:

| Pros | Cons |

|---|---|

| It acts as a source of continuous credit card rewards flow for travel, hotel stays, and shopping. | Banks may ban users for these manipulative acts or even close the account. |

| Allows to earn significant miles and credit card points obtained by daily expenditure. | Tendency to rack many credit card debt piling up due to additional credit available. |

| Helps boost credit score through lowering of usage on properly managed. | The credit score may be affected negatively. |

| Aids in saving on credit card bills. | Debt may pile up on one’s account. |

| They may aid in flying for free. | Future loan applications may become bleaker and more complex. |

| One gets introduced to different banks. | The card issuer may take rewards back. |

| Users can get huge rewards in their banks, including free flights and hotel stays. | However, the bank may close the credit card holder's accounts. |

Want a smarter way to bank on the go? Revolut offers a user-friendly app with global access, crypto and stock trading, and innovative budgeting tools—all in one powerful platform.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.