Table Of Contents

What is Cost Plus Pricing?

Cost-plus pricing is a methodology in which the selling price of a product is determined, based on unit costing, by adding a mark-up or profit premium to the cost of the product.

In simple words, it is a strategy of pricing a product in the market by adding a specific margin to the cost of that product. This margin, better known as mark-up, is the entrepreneur’s profit.

Selling Price = Cost * (1 + Profit Margin)

Or

Selling Price = Cost/ (1 – Profit Margin)

Thus, a stepwise approach is:

Step #1: Obtain details of all costs and units/resources involved in the production.

Step #2: Segregate them into groups, say fixed cost, labor cost, direct cost, direct material cost.

Step #3: Calculate unit cost based on the number of units involved in the production.

Step #4: Either determine the total unit cost of production and multiply it by mark-up or premium percentage or determine the total cost by multiplying unit cost and the number of units of each cost type.

How Does it Work?

- The most commonly used method is variable cost-plus pricing. In this, the mark-up or profit margin is added to the product's variable costs. Thus, the selling price equals the sum of variable costs and desired mark-up. Another method to determine price through a cost-plus strategy is target costing, where the selling price is fixed, and costs are worked upon to increase efficiency in the system, thereby increasing profit margin.

- Thus, profit equals the fixed selling price, minus the total of all costs. There are different variable costs associated with the manufacturing of a product. Some of them are direct labor, selling and marketing expenses, and material and packaging costs. It should be noted that different cost-plus pricing strategies apply to different scenarios. Take, for example, the one described above – variable cost-plus pricing. This strategy is used when markets are competitive, and producers can lower variable costs to gain profits.

- This strategy can also be used for contract bidding, where the specifics of a product are based on the variable costs, and thus, the lowest bidder is the beneficiary. A key demerit is that this strategy of pricing excludes opportunity costs. Opportunity cost is determined by the next best use of an asset or resource. If management can use its resources more profitably, it should include such assumptions and facts in its worksheet. Reliance on cost-plus pricing for such inclusions can be delusional.

Example of Cost Plus Pricing

Let's take an example.

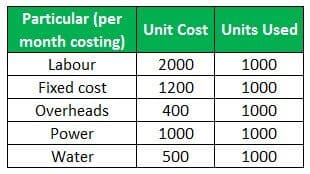

Suppose a power generation plant in a small city of Florida supplies electricity to the state electricity grid. The plant manager has agreed to be paid a 12% premium on the unit cost of electricity. He has employed a 1,000-strong workforce for his power plant. The items above are based on monthly costing; for convenience of calculation, 1,000 units are assumed to be produced per month. How should the manager decide the price per unit of electricity generated in his plant?

The manager lays out the unit cost of each of the expenses that his plant incurs and tabulates it as follows:

Solution:

- All figures in US$ except units;

- The manager calculated the total unit cost as the sum of fixed and variable costs and found it to be $5100.

- The selling price can be determined based on unit cost since the schedule here is activity-based costing. Or else, the manager can use the total cost price to determine his profit.

Note that in both scenarios, his profit and profit margin will be the same.

Profits are:

Selling Price = 12% Premium on Unit Cost Price of $5100 - Cost Price Itself = $612

- Hence his total profit will be $612 times units sold = $612,000.

- The profit margin will be 612/5100 or simply 12%, which was his premium on the cost price.

Now, the efficient operation and management of the plant can lead to cost reductions, in either fixed or variable costs, or both, thereby increasing the profit and profit margin for the manager.

Advantages of Cost Plus Pricing

- Helpful in competitive markets to participate in price wars.

- Easy to apply in situations where the unit product is specific and non-uniform.

- Helpful in measuring accounting profits and working on ways to improve efficiencies.

Disadvantages

- Difficulty in applying the strategy in most situations due to lack of efficiency;

- Cost-plus pricing may not encourage management to strategize consistently to keep up with the pace of competition because it always acknowledges price with profit and does not give incentives to reduce costs.

- The method is unjustifiable when a business deals with innovation and design. In such cases, the incentives to improve are overridden by market demand, and customer satisfaction takes priority.

Conclusion

Cost-plus pricing is one of the most used and simplest pricing strategies in businesses. The method has its advantages and disadvantages. For example, it often becomes difficult for the manufacturing businesses to equate production and demand such that the production schedule is profitable.

The primary disadvantage of this pricing strategy is that it ignores the competitor's profit margins and only considers the mark-up that the business/company/manufacturer focuses on. To tackle such situations, costing departments should always include competition and various aspects of sustainability and profitability in the mark-up or premium above cost price. Nevertheless, cost-plus pricing can help take deeper insights into businesses and develop consistencies and profits.