Table Of Contents

What Is A Correspondent Bank?

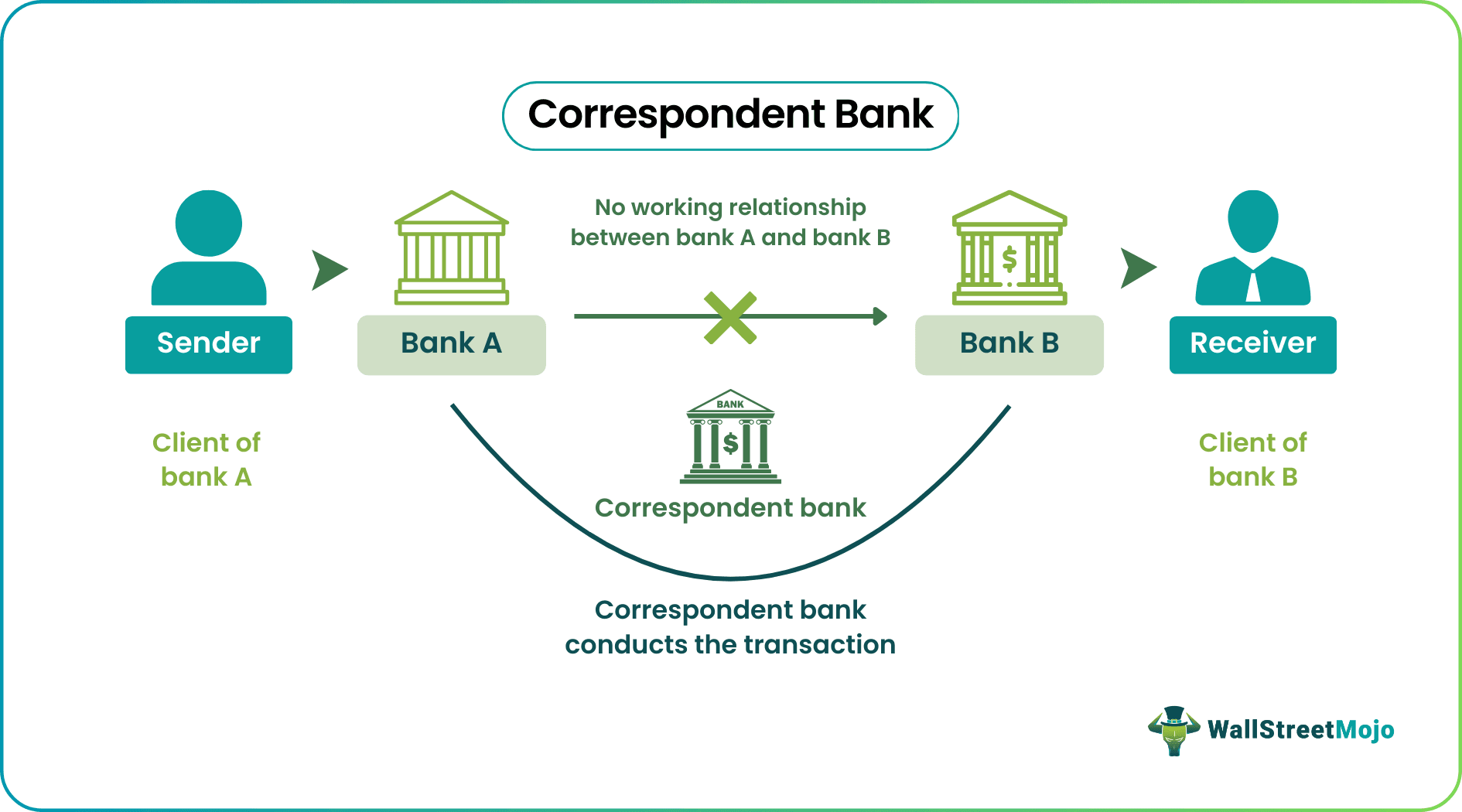

A correspondent bank is a financial institution that acts as a middleman to accomplish transactions on behalf of another financial institution. Correspondent bank account provides services like international fund transfers, cheque-clearing services, foreign exchange, treasury management, trade finance, and liquidity management. Bilateral agreements between two banks establish the correspondent accounts.

A country’s central bank decides and qualifies suitable financial institutions to function as an intermediary. The correspondent bank’s banking and other financial services depend on the related banking regulations set by the governing bodies. Hence the services it can provide varies between countries. Correspondent bank charges a fee from the sender before the transaction is wired to the destination account.

Table of contents

- What Is A Correspondent Bank?

- Correspondent banks’ definitions portray them as a middleman connecting unrelated financial institutions. Their functioning as a go-between assists another financial institution in performing transactions involving an unconnected entity as the receiver’s bank.

- The system helps the respondent banks have vast benefits like increased client base revenue and competitive advantage.

- Some of the services provided by these companies include international fund transfers, wire transfers, transaction settlements, collecting documents, and accepting deposits.

- Some of the services provided by these companies include international fund transfers, wire transfers, transaction settlements, collecting documents, and accepting deposits.

How Does Correspondent Bank Work?

Correspondent banks based on the underlying bilateral agreement connect financial institutions enabling domestic and cross-border money movement and related services. They provide various services to respondent banks, including deposit accounts. Communication between these banks frequently entails the transmission of messages for conducting transactions.

In some instances, banks require to connect with another bank which is generally a foreign entity, due to a lack of prior relationships with them or a lack of resources. As a result, they pay third-party institutions to participate in their transactions. It benefits the correspondent entity. They generate a portion of their revenue from earning correspondent bank charges for serving as an intermediary between two unconnected banks.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Services

The major services provided by in exchange for correspondent bank charges include:

- Wire transfers

- Transaction settlements

- Trade finance

- Currency exchange

- Treasury services

- Check clearing

- Managing international investments

- Collecting documents internationally.

These institutions often transfer funds, and accounts handling the fund transfer are called Nostro and Vostro. The respondent mentions their account with the correspondent entity as Nostro (ours), and the correspondent entity says the account for a respondent entity with them as Vostro (Yours).

One of the major networks used to expedite this system is the SWIFT network. SWIFT is one of the primary services focused on international remittances globally. The SWIFT network reveals relevant correspondent bank lists apt for accomplishing the transaction. However, countries such as China, India, and Russia are currently pushing forward new alternatives to SWIFT, which may diminish SWIFT's dominance over time.

Examples

Let us understand the ebbs and flows of a correspondent bank account with the help of a couple of examples.

Example #1

Let’s say that Roy, who runs a high-end car workshop, needs particular parts to repair one of his client’s cars. Unfortunately, the car is a Japanese model and, at the moment, he can only get the parts from Japan.

So, he decides to use a wire transfer to pay the Japanese manufacturer for the parts. He goes to the bank and deposits the money plus fees. The other company receives it in Japan and sends the parts.

To make the wire transfer, Roy’s bank, a local U. S.-based institution, sends the money using the Society for Worldwide Interbank Financial Telecommunication (SWIFT). The correspondents in the SWIFT network connect both sides for a fee using the system. It receives the money and then transfers it to the other bank, connecting each side and completing the transaction.

Example #2

Late in 2022, Iraq started experiencing an extremely strong financial crisis which ultimately resulted in the depreciation of its currency. Their currency dropped from 1,475 Dinars for a Dollar in September 2022 to 1,580 Dinars in January 2023.

Therefore, the Central Bank of Iraq had to follow the regulations of the U.S. correspondent banks to be able to continue accepting transfers.

Correspondent Bank Relationship

A correspondent banking relationship enables the respondent to shop for services from the correspondent entity. This effective cross-banking relationship allows the respondent to provide their clients with services requiring connection with a specific region where the respondent entity doesn’t have a branch or presence and accomplish the need through local correspondent banks. This banking relationship benefit comes in many ways, such as:

- Increase in clients

- Increase in revenue

- Gain competitive advantage

- Reduce the cost of geographical extension of the banking organization

Using the service of a correspondent financial institution is far cheaper than opening branches in foreign countries. So, unless a bank is interested in starting operations there, outsourcing international payments or other banking services is a handy way not to lose their customers when they require international operations.

Correspondent Bank vs Intermediary Bank

There’s a lot of confusion between the concepts of correspondent and intermediary. Often it is difficult to segregate the difference between them. For starters, some countries are intermediaries facilitating transactions between two or more financial institutions. In other countries, they are differentiated based on slight differences in their functionality.

For example, In the U. S., an intermediary bank is often an institution that will represent a local bank abroad. It can conduct wire transfers, accept deposits, and even obtain documents for its clients, just like a correspondent financial institution would. The main limitation of intermediaries is that they will not handle transactions in various currencies, unlike correspondents.

In conclusion, both are third-party banks assisting in completing financial transactions between banks that do not have a working relationship. The names will mean something quite similar, but specificities of the country may necessitate doing more research to understand the limitations of both sides.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Ask Questions (FAQs)

The prime purpose is to act as an intermediary or intermediary between two banks which does not have a working relationship. Being a middleman, they predominantly accomplish domestic and cross-border payments.

The terms indicate different entities. The correspondent connects the issuing or sender’s bank to the receiving bank. They perform services on behalf of another bank, acting as a go-between for the issuing and receiving banks.

Most people use both terms interchangeably. Both are third-party entities supporting activities like international fund transfer and transaction settlements. In some countries, the evaluation of functionalities indicates them as the same concept. At the same time, there are different concepts in other countries based on slight differences. For example, an intermediary provides services in only limited currencies; conversely, correspondents usually offer several currencies.

Recommended Articles

This has been a guide to Correspondent Bank and its Meaning. Here we discuss its relationship, compared it with intermediary banks, examples, and services. You may learn more about our articles below on accounting –