Table Of Contents

What Is A Collateral Assignment?

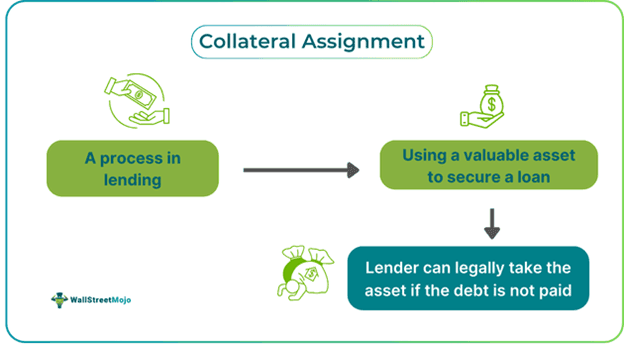

A collateral assignment is a financing method that involves using a valuable asset to secure a loan. When collateral is assigned, the lender has the legal right to take possession of the asset if the borrower fails to repay the loan amount. In a collateral assignment of life insurance, a life insurance policy is used as collateral for a loan.

You are free to use this image on your website, templates, etc.. Please provide us with an attribution link.

In this scenario, the collateral is the face value of the life insurance policy, which can be utilized to repay the amount owed if the borrower passes away while carrying the debt. It is a standard element in business financing.

Key Takeaways

- A collateral assignment is a type of financing when a loan is obtained by providing a valuable asset as collateral. If collateral is assigned, the lender is legally entitled to take ownership of the asset in case the borrower defaults on the loan.

- Collateral assignment of life insurance is the process of providing a lender with collateral when applying for a business loan.

- The assignment agreement requires the policy owner to acquire life insurance. In this arrangement, the life insurance company will charge premiums in addition to the loan installments.

How Does Collateral Assignment Of Life Insurance Work?

Collateral assignment of life insurance is an approach for offering a financier collateral when an individual applies for a financial loan. This assignment is an extension of the life insurance policy that grants a lender the first claim to the life insurance payout. However, it also allows individuals to choose the beneficiaries who will receive any remaining funds after the loan is repaid.

This an easy process. Following the completion of the application and underwriting procedures, an individual will have to wait to receive the offer. Once all the documentation is complete, the assignment will be put up. The lender will provide a written release once the debt has been paid off. The collateral condition on the insurance policy expires. However, the policy owner can keep the life insurance active if they want to.

How To Apply?

The steps to apply or set up for Collateral Assignment include the following:

- Assessing the lender's criteria: One can find out if the lender accepts life insurance as collateral for an assignment. If they do, one must find out what is needed for this arrangement from them.

- Setting up life insurance coverage: If their insurer accepts the assignment, individuals may utilize their existing life insurance. However, they might have to get another policy if they do not have life insurance or if the death benefit is not adequate.

- Submitting the forms for the assignments: Individuals may obtain an assignment form by contacting their life insurance provider. This form includes details regarding the loan, including the amount, the lender, and the repayment plan.

- Completing the loan setup process: With collateral in place, the borrower and the lender may complete the loan application procedure. Once authorized, the lender will send the loan money, which is guaranteed by the life insurance.

Examples

Let us study the following examples to understand the process:

Example #1

Let us assume that Jenny wants to start a business and needs to borrow a loan of $100,000. As collateral, she decided to use her life insurance policy, which gave her a death benefit of $300,000. Using the policy as collateral made it easier for her to secure a loan at favorable interest rates. This is an example of collateral assignment of life insurance.

Example #2

Suppose Sam wants to borrow $50,000 to upgrade the equipment in his company. He approaches a bank that agrees to pay him the sum if he uses his life insurance policy as collateral against the loan amount. His insurance policy offers a death benefit of $200,000. However, Sam ends up defaulting on the loan. In this scenario, the bank uses his life insurance policy to recover the loan amount. This is another example of collateral assignment of life insurance.

Alternatives

Some of the alternatives for Collateral Assignment are as follows:

- Applying for an unsecured loan: Individuals may evaluate the cost of borrowing money without providing collateral. However, the loan might have a higher interest rate. If there are other circumstances in which an individual does not need life insurance, it might be less expensive to borrow money through an unsecured loan.

- Utilizing other resources: One may use a property, vehicle, or investment account as collateral in place of life insurance. If there is a home equity line of credit and the individual has paid off a portion of the mortgage, they can use it to borrow money.

Benefits

Some benefits of Collateral Assignment include the following:

- Collateral may increase the possibility of loan approval: If the applicant has life insurance as collateral, it can make a difference in the approval process. Collateral can solve specific problems, such as a low credit score or an insufficient down payment.

- It may lower the interest rate on the loan: The lender's financial risk is decreased when there is collateral. It guarantees them a backup plan in case they fail to pay loan installments. The lender might provide a cheaper interest rate in return.

Drawbacks

The drawbacks of Collateral Assignment are:

- It lowers the benefits of life insurance: The lender has priority in collecting life insurance in this assignment. The terms of the insurance policy may limit the ability to use it until the policyholder settles the debt if it has a cash value. The death benefit will be used first to settle the debt if the policy owner passes away before making the last payment.

- It results in increased insurance expenses: The policy owner needs to obtain life insurance to comply with the assignment arrangement. The life insurance provider will charge premiums, which are an additional expense on top of the loan's installments.

Collateral Assignment Vs. Absolute Assignment

Collateral Assignment

- It functions similarly to a regular loan.

- The insurance policy serves as collateral for a loan. Until the loan is repaid, the individual or entity that makes the loan payments is the temporary beneficiary of the policy's death benefits.

- The policy is assumed on a conditional basis, indicating that the entity assuming it lacks the power to alter it, sell it, or withdraw any of its monetary value.

Absolute Assignment

- Absolute assignment in insurance involves transferring the whole policy to another individual or organization.

- The assignee is the individual or group that gets the insurance policy, while the assignor sells or gives it as a gift.

- The insurance becomes entirely owned by the assignee, who also assumes responsibility for any premium payments and acquires the autonomy to modify or add beneficiaries.