Table Of Contents

What Is Chapter 7 Bankruptcy?

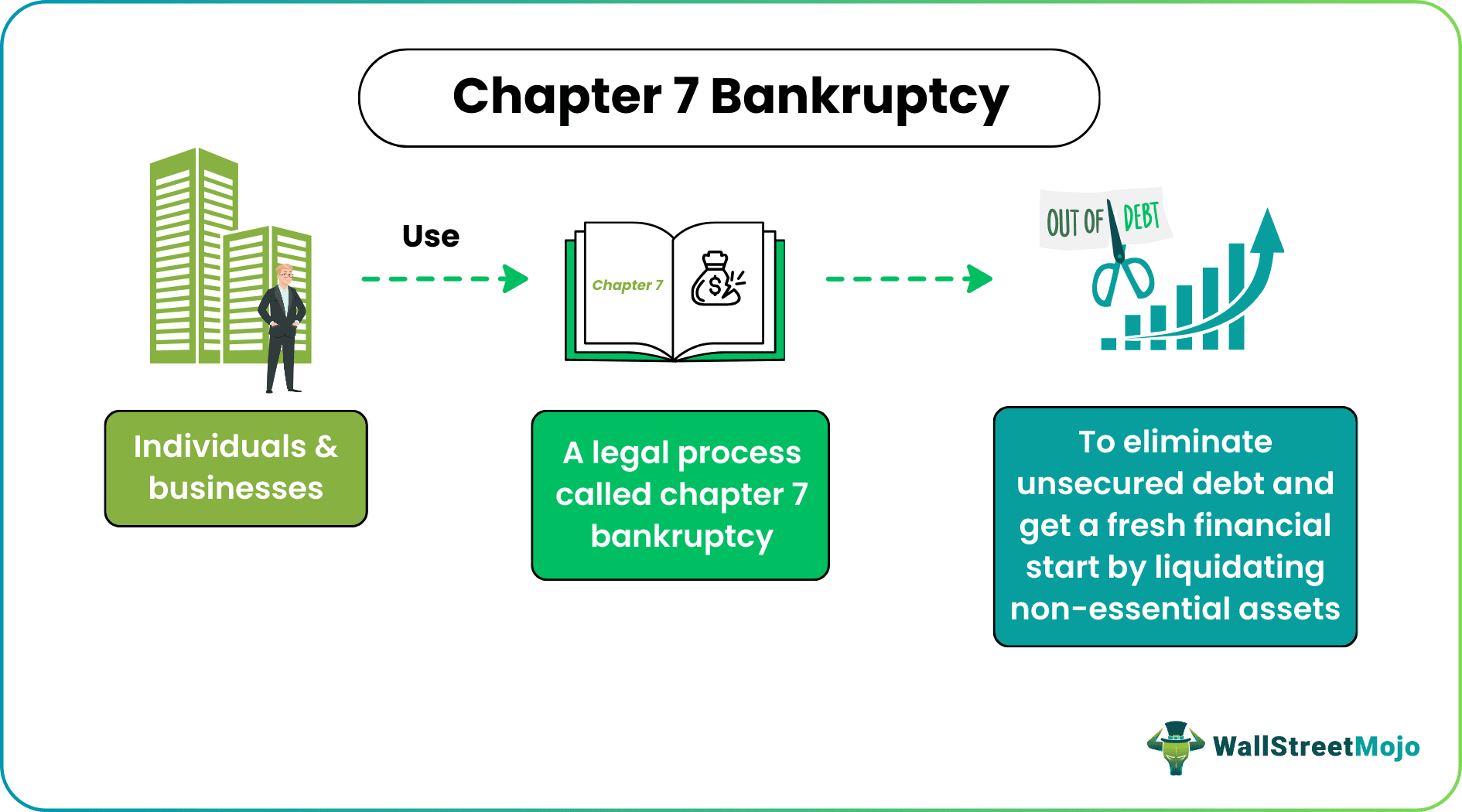

Chapter 7 bankruptcy, also known as liquidation bankruptcy, is a legal mechanism designed to offer a renewed financial beginning for individuals and businesses grappling with substantial debts. The primary objective is to absolve or discharge a vast majority of their unsecured financial obligations, such as medical expenses, personal loans, and credit card debts.

To be eligible for Chapter 7 bankruptcy, individuals must pass a means test, which assesses their income and expenditures. Upon satisfying this requirement, the court mandates the liquidation of non-exempt assets owned by debtors to facilitate repayment to creditors. Consequently, any remaining qualifying debts are then discharged, liberating debtors from their responsibility to repay them.

Table of contents

- What Is Chapter 7 Bankruptcy?

- Chapter 7 bankruptcy, or liquidation bankruptcy, is a legal process that aims to provide individuals and businesses burdened by substantial debts with a renewed financial beginning.

- Its primary objective is eliminating or discharging most of its unsecured obligations, including medical bills, personal loans, and credit card debts.

- To qualify, individuals must meet the following requirements: have a low income, pass the means test, complete credit counseling, provide the necessary documentation, file a petition, have an automatic stay in place, attend the 341 meetings, and potentially undergo asset liquidation.

Chapter 7 Bankruptcy Explained

Chapter 7 bankruptcy entails a legal procedure through which individuals or businesses can eliminate their unsecured debts by selling off assets exempt from the bankruptcy process. The bankruptcy trustee allocates the proceeds from these asset sales to settle determined loans. This avenue has emerged as a swifter and more secure approach to unburden oneself from unnecessary debt obligations, enabling individuals to embark on a fresh financial journey, safeguard vital assets essential for maintaining livelihoods, and cultivate new credit histories.

Chapter 7 bankruptcy involves initiating a formal bankruptcy petition within the court system, undergoing and meeting the means test criteria to ascertain eligibility, and engaging a bankruptcy trustee responsible for assessing the debtor's financial situation. This trustee then devises a strategy for resolving unsecured debts, often involving the sale of exempted assets to facilitate loan repayment, culminating in a court-sanctioned discharge of debts.

In personal finance, Chapter 7 bankruptcy offers individuals and entities a middle path to regain financial control and establish credibility within the market over the long term. Some may explore alternative debt management strategies, such as Chapter 13 bankruptcy, to restructure debt obligations.

The effectiveness of Chapter 7 bankruptcy as a practical tool for escaping overwhelming debt has been well-established. However, it is imperative to thoroughly evaluate one's financial circumstances before embarking on this route and to seek informed guidance from legal professionals or credit experts to ensure a successful outcome. Additionally, debtors may anticipate receiving tax refunds from the Internal Revenue Service (IRS) as part of this process.

Requirements

The requirements to qualify for Chapter 7 bankruptcy are the following:

- Low Income: Individuals seeking bankruptcy relief should have an income lower than the national or state average for their specific category.

- Means Test: Applicants must pass a means test evaluating their ability to repay debts. This test compares their income with the median income in their state, adjusted for family size and expenses. Failing this test qualifies them for Chapter 7 bankruptcy.

- Credit Counseling Course: After a failed means test, the debtor must complete a credit counseling course from an accredited counseling agency within six months.

- Documentation: Relevant financial documents such as income statements, asset and liability lists, tax returns, and recent financial transactions must be gathered and presented to the bankruptcy trustee. This information helps determine the debtor's financial situation and asset management.

- File Petition: Following these steps, the debtor must file a Chapter 7 bankruptcy petition with the bankruptcy court through their Chapter 7 bankruptcy attorney. This petition includes mandatory forms, schedules, and explanations of the debtor's financial status, income, expenses, and creditors.

- Automatic Stay: An automatic stay takes effect once the bankruptcy petition is filed. This stay provides immediate relief from credit payments and shields the debtor from creditor demands. It temporarily stops actions like wage garnishments, ongoing loan recovery lawsuits, and collections, offering a respite for the debtor.

- 341 Meetings: After the automatic stay, a meeting is convened involving the debtor, bankruptcy trustee, and creditors. This gathering allows creditors and the trustee to question the debtor regarding their financial matters and bankruptcy petitions.

- Asset Evaluation: Following the 341 meetings, the bankruptcy trustee assesses which assets will get the protection and decides whether to sell non-exempt assets to repay creditors.

Process Steps

Steps involved in Chapter 7 bankruptcy:

- Consult Attorney: The applicant meets with an attorney to understand the process and explore alternatives to manage their debts.

- Complete Credit Counseling: If the attorney advises, the debtor takes a 180-day credit counseling course from an approved agency. This course imparts debt management and budgeting skills.

- Gather Financial Documents: After completing the course, the debtor collects income proofs and necessary documents for filing the bankruptcy petition.

- File Petition: The debtor files the Chapter 7 bankruptcy petition in the bankruptcy court.

- Pay Fees: A filing fee of $338 is paid, either at once, in installments, or a waiver is applied for.

- Automatic Stay Begins: Automatic Stay kicks in upon filing, shielding the debtor from creditor actions.

- Trustee Assigned: A bankruptcy trustee is appointed to oversee the case and review financial documents.

- Attend 341 Meeting: The debtor participates in a meeting with the trustee and creditor, addressing questions about their finances and the bankruptcy petition.

- Possible Asset Sale: The trustee might suggest selling non-exempt assets to repay creditors while protecting essential assets.

- Debt Discharge Order: If all requirements are met, the court issues a debt discharge order, granting relief from repayment obligations to creditors.

Examples

Let us look into some examples:

Example #1

In 2008, Artes Medical Inc., a notable manufacturer specializing in dermal fillers for cosmetic treatments, faced a pivotal juncture as it navigated through a Chapter 7 bankruptcy process, signaling its liquidation intention. A confluence of factors influences this strategic decision, including the challenging economic landscape of that time and shifts in consumer spending habits.

The company's decision to initiate Chapter 7 bankruptcy reflected a determination to address its financial obligations by liquidating assets to facilitate the repayment of creditors. Amidst this complex scenario, Artes Medical's shareholders and stakeholders grappled with the implications of this undertaking, underlining the intricate dynamics businesses encounter in times of economic uncertainty.

Example #2

Suppose John chose to pursue Chapter 7 bankruptcy to alleviate the burden of accumulating financial obligations, including credit card expenses, medical bills, and personal loans. The successful discharge of his medical and credit card debts gave him a renewed outlook, offering a clean slate for his financial journey.

Notably, his unpaid taxes and college loans remained outside the purview of the discharge. Despite the lingering responsibilities tied to these obligations, John experienced a notable sense of relief and liberation as he emerged from the bankruptcy process with the weight of his discharged debts lifted from his shoulders.

Advantages And Disadvantages

The advantages and disadvantages are as follows:

| Advantages | Disadvantages |

|---|---|

| Terminates unsecured loans, offering a fresh financial start. | Negative impact on credit score. |

| Prevents property repossession or foreclosure. | Possible loss of certain assets. |

| Halts loan collection efforts and garnishments. | Lengthy waiting period before filing again. |

| The debtor receives a court-issued discharge of debts. | Certain debts like alimony, student loans, and taxes may still require payment. |

| Cost-effective and swift method to alleviate overwhelming debts. | Qualifying means tests could add to the debtor's stress. |

| Facilitates a fresh start for debtors, enabling new job opportunities with reduced debt burden and creditor protection. | Remains on credit history for a decade, potentially affecting employability and credit approval in the future. |

Frequently Asked Questions (FAQs)

Chapter 7 bankruptcy is relevant for individuals and businesses overwhelmed by unmanageable debts. It offers a fresh financial start by discharging unsecured debts, preventing repossessions, and stopping creditor actions. While it provides relief, it also has implications for credit history and certain asset loss.

Chapter 7 bankruptcy can harm credit scores, making future borrowing more challenging. Debtors risk losing non-exempt assets, affecting their financial stability. Not all debts, including alimony, student loans, and taxes, are dischargeable. The process's public record might also affect future employability.

Chapter 7 bankruptcy is for individuals and businesses seeking debt relief through liquidation, whereas Chapter 11 is mainly for businesses aiming to reorganize debts and continue operations. Both chapters have distinct eligibility criteria and outcomes.

Recommended Articles

This has been a guide to what is Chapter 7 Bankruptcy. Here, we explain its requirements, examples, process steps, advantages, & disadvantages. You can learn more about it from the following articles –