Table Of Contents

Cash-Out Refinance Meaning

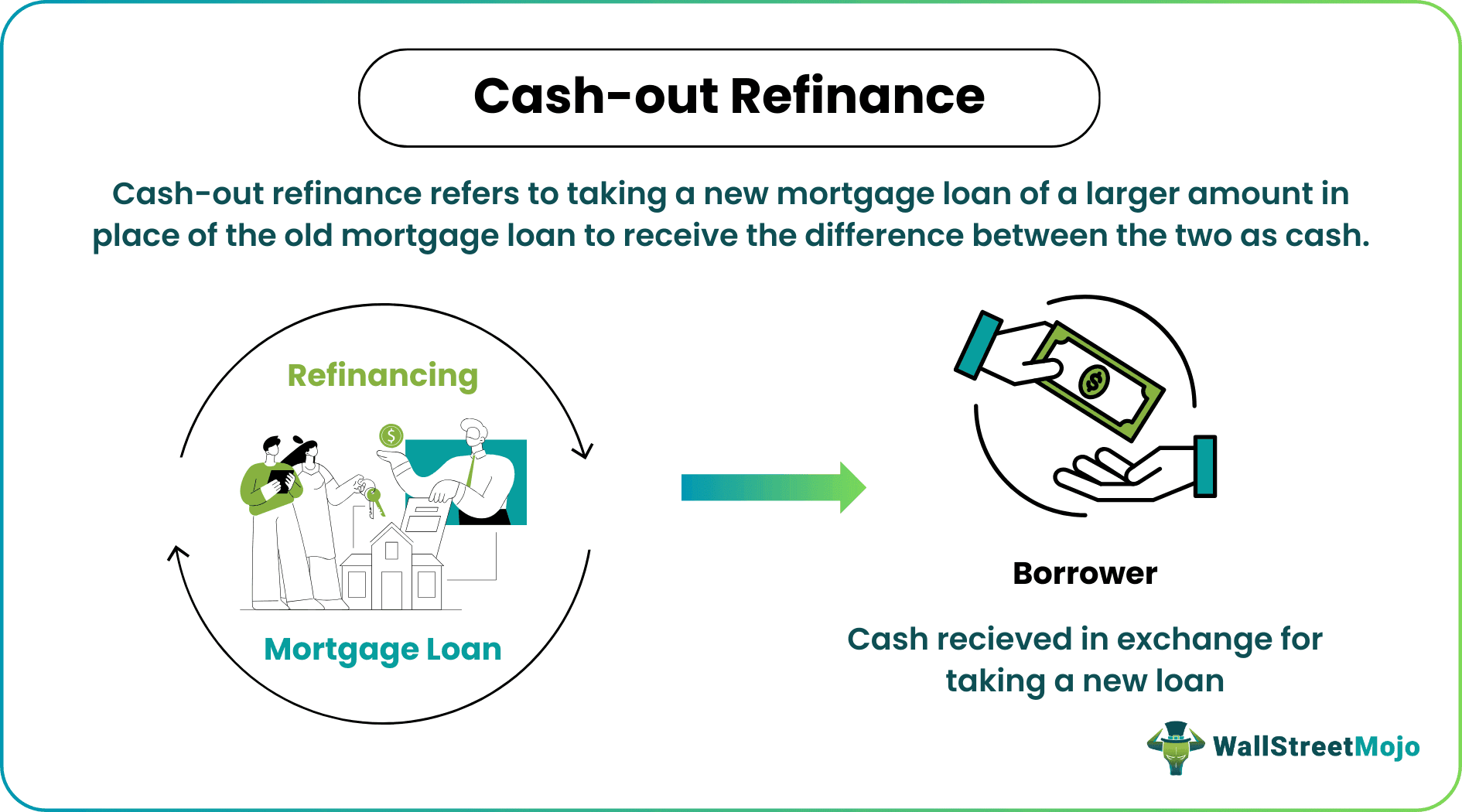

Cash-out refinance (COR) means taking a new mortgage loan of higher value to close the old mortgage loan and receiving the difference as cash. This refinancing option enables borrowers to utilize the equity on their property to borrow more and use the money obtained to serve their personal needs.

Generally, loanees use the cash-out refinance to escape the burden of credit card debts, education loans, or renovation. However, it is available at a higher interest rate than other refinancing options due to the higher credit risk involved. In addition, it comes with hidden charges like closure costs, appraisal cum processing charges, etc. But the cash payout under COR is not taxable in the hands of the borrower. This makes it an attractive refinancing option.

Key Takeaways

- Cash-out refinance (COR) involves replacing the old mortgage loan with a new one of a larger amount so as to receive the difference between the two as cash.

- The borrower can use the cash received from cash-out refinance for refurbishment, paying off higher interest debts, or any other personal needs.

- It is the best and the cheapest option to get some cash as its interest rates are less than personal or credit card loans.

- It involves a complex underwriting process and involves other costs. In addition, it charges a higher rate of interest than other refinances.

- Both cash-out refinance and a home equity loan enable borrowers to access the equity in their homes. However, the former closes the existing loan and provides cash, while the latter offers a new separate loan with equity as collateral.

Understanding Cash-Out Refinance

Cash-out refinance is a mortgage refinancing option that enables borrowers to obtain cash in exchange for taking a new loan that is higher in value than the existing loan. This cash is provided against their property's equity. Equity means the portion of the property for which the mortgage payment has been made.

Under cash-out refinance, the existing loan is closed before the new loan is initiated. The new loan amount includes the old loan balance and the cash paid out to the borrower. Now, the borrower has a new loan of higher value to be repaid to the lender. Nevertheless, the cash received through COR compensates the borrower for the increase in mortgage balance.

Borrowers can use the cash thus obtained in a number of ways like paying high-rate credit card loans, settling student loans, or home improvements. Note that the money received is tax-free in the hands of the borrower. Hence, it is a popular refinancing tool.

Furthermore, it is similar to the rate and term refinance, in which a loanee modifies the terms and conditions (like interest rate or loan term) of the existing loan to reduce mortgage payment. Like the rate and term refinance (RTR), cash-out refinance allows the borrower to benefit from a lower interest rate or shorter-term loan when opting for a new loan.

However, unlike RTR, the borrower usually pays a higher interest rate and other costs to compensate the lender for the additional risk of default. Therefore, among refinancing options, RTR is ideal for taking advantage of lower interest rates. At the same time, COR is suitable for drawing cash from the property's equity to meet personal needs.

How Does Cash-Out Refinance Work?

A borrower who needs cash to fund the renovation of a property or pay back debt must determine the following:

- Amount of cash required

- Existing mortgage loan balance

- Current valuation of the mortgaged property

- Rate of interest

- Alternative refinancing options available

- Charges of loan closure

- Amount receivable as cash through the cash-out refinance calculator

Now, suppose the borrower finds that the current valuation of the property has increased substantially to cover the existing loan upon closure, and the interest rates have been reduced. In that case, COR is the perfect option as it is advantageous in terms of getting cash at lower rates than through credit cards and home equity loans. Therefore, the borrower searches for a suitable lender that offers:

- Lower cash-out refinance rates

- Lower appraisal fees

- Lower processing fees

- Faster approval

- Appropriate mortgage loan amount

- Enough cash after COR

As a result, the borrower applies with the chosen lender for cash-out refinance, closes the old mortgage loan, and gets cash to satisfy his needs. Then, proceeds to make payments on the new loan as per the agreed terms.

Examples

Every finance concept has a real-life bearing on the financial well-being of an individual. Hence, it is more apt to understand the idea of cash-out refinance examples below and then use it in personal life.

Example #1

Let us assume that consumer X has already taken a mortgage loan of $300,000 on his property of the same value. X is now left with $100,000 as a balance for the home mortgage. Thus, the equity in the home is $200,000.

But X's home has grown in worth to $400,000. This means the equity has grown to $300,000 ($400,000 – $100,000). To tap into the home's equity for cash, X decides to opt for COR.

Banks usually allow 80% of the home value as a mortgage loan. So, X is entitled to receive $320,000 (80% of $400,000). Since he has to pay $100,000 to close the old loan, he can receive $220,000 as cash.

However, he currently needs only $200,000 cash. Therefore, X refinances by taking a new loan of $300,000 and receives the difference between the new loan and the old loan balance, i.e., $200,000 ($300,000-$100,000) as cash.

Thus, X has $200,000 in hand and a new mortgage of $300,000. So, from now on, X will be under a bigger mortgage loan ($300,000) than the previous one ($100,000) and may have to pay interest as per the agreement. Also, his home equity has reduced in value as $200,000 cash is paid out of it. It is now valued at only $100,000 ($300,000-$200,000).

However, he can use the cash received from COR for any personal need like revamping his property, treatment of illnesses, or wedding. Moreover, as per law, he is not required to report the money as income in his tax returns.

Example #2

Another person, Y, is in urgent need of renovating his property. Last year Y bought a home worth $300,000 from a mortgage loan. He has paid $100,000 of the home loan. But $200000 is still outstanding. Thus, his home equity value is $100,000.

Moreover, as per the property's current market, Y's house is worth $600,000. With the rise in property value, his home equity stands at $400,000 ($600,000 – $200,000). So, he decides to extract his home equity for cash.

As a result, Y searches for a suitable lender that will offer a lower interest rate, higher valuation of the property, lower processing fee, and faster appraisal and loan disbursement for the cash-out refinance.

Then, he approaches a suitable lender, and the lender agrees to pay $480,000 (80% of the home value of $600,000) as a new loan. Since the outstanding balance of the old loan is $200,000, he can receive a maximum of $280,000 ($480,000-$200,000) as cash. He agrees to it.

So, his new mortgage loan stands at $480,000 (old loan balance $200,000 plus cash out $280,000) and his home equity reduces to $120,000 ($400,000-$280,000). However, he receives $280,000 in cash for the renovation of his property.

Cash-Out Refinance vs Home Equity Loan

Here is an outline of the difference between cash-out refinance and home equity loans.

| Parameters | Cash-Out Refinance | Home Equity loan |

|---|---|---|

| Terms of loan | Converts a mortgage loan into a bigger loan and provides the difference as cash to the borrower. | Creates a second loan consisting of a new set of terms and conditions. |

| Type of mortgage | First mortgage as it closes the existing loan and replaces it with a new loan. | Second mortgage as it is separate from the original mortgage and requires additional payments. |

| Mode of loan disbursal | The amount received is first used to close the first mortgage loan, and the remaining amount is given to the applicant as cash. | Both loans have to be paid simultaneously. However, the lender of the second loan is second in line to claim payments on default. |

| Rate of interest | The rate of interest offered is either fixed-rate or floating rate. | Fixed interest rates that are lower than the original loan rates. |

| Benefits | It is costlier than a home equity loan. | It is cheaper than cash-out refinance. |

| Credit score | Higher credit score required. | Low credit score required. |

| Complicated process | More complicated due to underwriting required. | Less complicated. |

| Risk | Less risk. | More risk as there are two mortgages. |

Pros and Cons

Anyone thinking of putting his old mortgage loan must know the pros and cons of the COR first. It will be beneficial in making a good decision.

Pros

- Cash-out refinances have a lower rate of interest than a credit card.

- Borrower receives money or cash.

- COR processing is quick.

- It has no liability like a credit card on the consumer's credit score.

- Money received from COR is not reported as income and hence, tax-free.

- It improves the overall credit score of a customer.

- The amount received from COR can be used for any purpose.

- Interest paid on the new COR loan is tax-deductible.

Cons

- The value of the mortgage loan increases.

- The lender may extend the term of the new loan.

- COR has higher interest rates than other refinancing options.

- A sizable amount is goes as closure charges.

- It is not a long-term solution to debt.