Table Of Contents

Cash Generating Unit Meaning

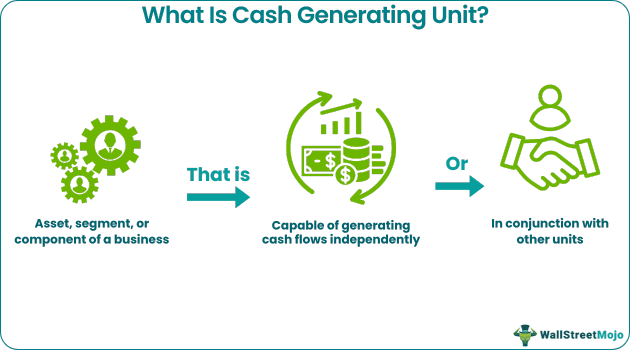

A Cash Generating Unit (CGU) is a fundamental concept in International Financial Reporting Standards (IFRS) used for asset impairment accounting. It represents the smallest group of assets within a business or organization that primarily generates cash flows independent of other assets or groups of assets.

Identifying CGUs is crucial for allocating cash flows related to goodwill and other corporate assets that do not generate their cash inflows. While determining CGUs can be intricate and requires careful judgment, it's essential to note that CGUs are not limited to assets that directly produce cash. They can encompass assets that contribute indirectly to cash generation.

Key Takeaways

- The Cash generating unit refers to a group of identifiable assets that yield cash inflow for a business independent of other asset groups.

- CGUs are instrumental in financial reporting and valuation ensure accurate goodwill allocation by International Financial Reporting Standards (IFRS) and International Accounting Standards (IAS) 36.

- The importance of defining CGUs can be seen in asset impairment cases and situations where goodwill accounting is to be done.

Cash Generating Unit Explained

Cash generating units (CGUs) are pivotal in accounting, particularly concerning asset impairment and goodwill valuation. Asset impairment assessments determine whether an asset's carrying amount exceeds its recoverable amount, ensuring that assets are correctly valued. On the other hand, goodwill represents the intangible value of a business entity that cannot be precisely quantified in monetary terms. The IFRS cash generating units concept, as defined in International Accounting Standards (IAS) 36, addresses these complexities and inefficiencies in accounting.

Identifying CGUs is a fundamental step in this accounting process. Two primary criteria aid in this identification. Firstly, CGUs should have the capacity to generate substantial cash flows independently. The unit is only classified as a CGU if this criterion is met. Secondly, CGUs should operate in markets where their output has a tangible presence and active demand. Only under these conditions can a unit be designated as a CGU. Proper identification is essential, serving as the initial phase in the accounting treatment of CGUs.

To illustrate this concept, consider the example of a mall. Certain areas within the mall, like a decorative fountain or a recreation space, though integral to the ambiance, do not directly contribute to cash inflow. In contrast, the cafeteria is a prime example of a CGU. Here, it is possible to pinpoint the specific shops and enterprises that contribute to the cash flow of this particular CGU.

Apart from cash flow allocation, CGUs facilitate cash flow management. Once a group of cash-generating assets is identified, their cash flow over the years can be analyzed to realize a pattern. Based on this, appropriate measures can be taken to maintain and even improve the inflows from these CGUs. Structural changes can also be introduced after the analysis. Moreover, this identification and analysis need to be done periodically.

Examples

Here are a few examples of CGUs.

Example #1

XYZ is a book manufacturer. The company has 100 units of inventory, which ensures future cash inflow. XYZ's inventory is a CGU. The company also uses trucks to distribute the books. While these trucks are assets, they are not CGUs because there is no active market for their output. The same goes for office furniture like tables, chairs, stationeries, etc.

Example #2

London-based cloud services provider Gamma Communications PLC informed that its revenue in 2022 was up 8.2% from GBP 447.7 million in 2021 to GBP 484.6 million in 2022. However, the pretax profit had dropped by 3.4% from a year ago. This drop in profit is attributed to the non-cash exceptional items associated with the impairment of its Spanish CGU.

Impairment Of Cash Generating Unit

Impairment refers to the situation where the carrying cost of a CGU exceeds its recoverable amount. The value by which the carrying cost exceeds is a loss for the firm. The carrying amount refers to the value of an asset after deducting depreciation and other losses.

The carrying amount should always be at least the recoverable amount, else an asset is impaired if the estimated cash flows exceed the book value. This difference can be attributed to goodwill, market rates, obsolescence, etc. The same concept is also applicable to intangible assets because intangible assets such as goodwill also contribute to future cash flows. When the goodwill improves, the customer base also increases.

Let us understand how CGUs are recorded. Once the impairment is recognized, the carrying amount shall be reduced to the recoverable cost, and the impairment loss will be accounted for in financial statements. Also, the depreciation charges of such a CGU can be adjusted to future periods spanning its helpful life to allocate the revised carrying amount.

The company's goodwill shall be allocated to assets or CGUs from the lowest level of the entity's assets. This is because goodwill can't be attributed to a single group of assets and should be assigned uniformly. Sometimes, the goodwill is only allocated to CGUs and not non-cash-generating assets.