Table of Contents

What Is Cash Forecasting?

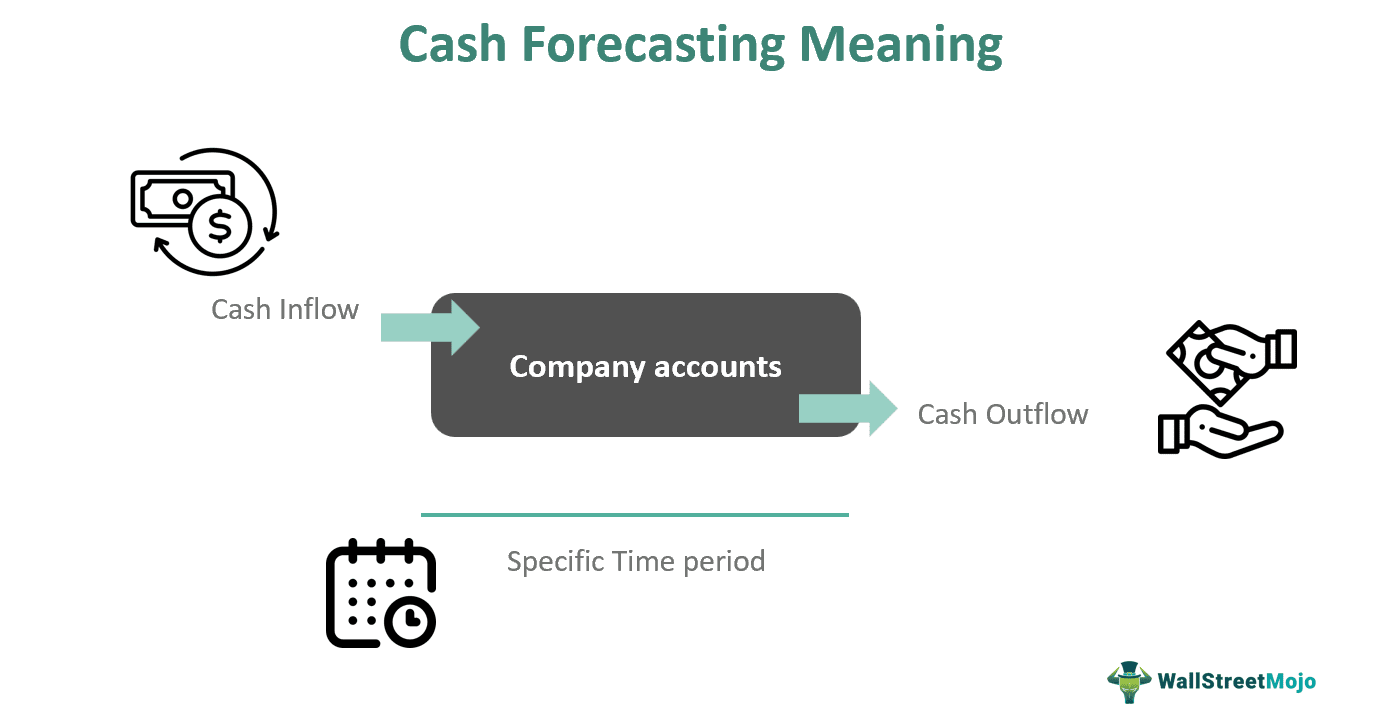

Cash forecasting is the estimation process of an enterprise's cash inflows and outflows over a specified period. It takes into account multiple data sources, such as future sales, investments, debt, expenses, new projects, market reports, and so on. It helps businesses predict future cash performance.

The whole process is conducted primarily by the finance team to inform top management about any potential risks, cash shortages, financial crises, and capital requirements, including surpluses, returns, and profit. It assists in risk aversion, growth strategy development, and recovery from debt. With new technologies and software, it is becoming an integral part of corporate financial management.

Key Takeaways

- Cash forecasting is deriving the future cash flow both in and out of the company during a specific period.

- There are mainly four main types of forecasting methods: direct, indirect, rolling cash flow, bottom-up, and top-down approaches.

- It has four main components: cash inflows, cash outflows, opening balance, and closing balance. With innovation, cash flow forecasting platforms, IT services, and software have created a market that helps enterprises.

- Without such forecasting, companies will tend to lose sight of funds, new projects, investments, shortages, and surpluses.

Cash Forecasting Explained

Cash forecasting is the assessment of an organization's cash inflows and outflows for a particular period. It helps inform management about when and how much cash is expected to come in parallel to where and what expenses are going to be utilized or spent. Any company, irrespective of its size and nature, requires cash for everything from daily operations to long-term growth and expansion plans. For this, cash forecasting templates assist in elaborating the funds that the company shall receive in the form of profits, revenues, returns, investments, dividends, or simple payments and, likewise, how the collected funds shall be used. Cash outflows are typically the objective of this forecast. In simple terms, it ensures the company accounts always have sufficient cash and the right amount of money is spent in the right direction.

The four main components of the cash forecasting model are cash inflows, cash outflows, opening balance, and closing balance. It generally includes the process of gathering historical data, identifying and projecting cash flows, estimating and planning cash outflows, and incorporating noncash items. Although it has its limitations, businesses strive to refine data accuracy, indulge in scenario planning, improve cash flow management, and monitor cash flow drivers to make better forecasts.

With innovation and technology, cash forecasting software is introduced to minimize the time and effort required for the complex data analysis and manual work needed for excellent and efficient forecasting. Companies tend to outsource such assessments to many third-party online platforms, IT solutions, and advisory firms that are skilled and have specialized teams assigned to assist in this forecasting using unique market and analytical tools.

How To Do Cash Forecasting?

The main steps to perform in this forecasting are as follows:

- Setting Objectives - The very first step is to determine the goal of this forecasting; it can be conducted for various reasons like risk management, debt reduction, expansion planning, and so on. The more precise the objectives are, the better outcomes can be achieved.

- Determining Forecast Period - A cash forecast can be performed for any particular period. A short period offers less data at the same time, and a long time frame can have inaccuracies. Hence, setting a suitable forecasting period is essential.

- Selection Of Forecasting Method - Again, a more important part of forecasting is to choose the right method. It can be a direct forecasting method or an indirect forecasting method. Both have their advantages and disadvantages, and they should be selected based on the forecasting objective.

- Forecasting Cash Inflows - The finance team must look at multiple sources of data representing sales, profit, and revenue and try to seek a pattern or trend, including the variable factors, to predict the sales and make an income estimation.

- Estimating Cash Outflows - Conversely, the team is responsible for covering all types of expenses, capital requirements, and debts to measure the cash outflow. Both the inflow and outflow must be calculated for the set period only.

- Data Compilation - All the data from cash inflows and outflows are compiled together to derive insights and information and define sensible outcomes that are used to create the analysis report for understanding financial stability.

- Review And Revisit The Forecast Report - The report is checked and revisited several times; it is not a one-time process. In fact, an old forecast report can also help with a new forecasting analysis. At the same time, new data can be introduced to update the report and improve its accuracy.

Cash flow forecasting is a crucial part of financial modeling. If individuals wish to develop a practical understanding of this process, they may consider enrolling in the Financial Modeling 2-Day Bootcamp. The course aims to provide one with detailed knowledge of how to create a financial model from scratch.

Cash Forecasting Methods

There are various cash flow forecasting techniques that one can use. That said, some popular ones are as follows:

- Direct Cash Flow Forecasting Technique: This method involves estimating cash outflows and inflows by closely monitoring the actual movement of cash out of and into the organization.

- Indirect Cash Flow Forecasting Technique: This technique involves deducing cash flows by beginning with net income and subsequently making adjustments for depreciation and other non-cash items.

- Rolling Cash Flow Forecasting Method: This technique involves updating cash flow estimates on a regular basis via the addition or dropping of periods over time.

- Qualitative Forecasting: This method involves using a combination of expert opinion, research, and historical data analysis. Hence, it is an ideal choice for organizations that have resources to accumulate and analyze substantial data.

- Automated Forecasting: This latest cash flow forecasting approach is dependent on application programming interfaces or APIs to accumulate cash-related data from banks directly. After data collection, this method involves forecast generation via the application of artificial intelligence or AI technology. In addition, this approach involves using machine learning or ML algorithms to spot and integrate trends concerning historical data into projections, thus enhancing accuracy.

Cash Forecasting Best Practices

Some of the best practices associated with cash flow forecasting are as follows:

- Streamlining Data Categorization - Individuals must carry out extensive tagging of transactions to comprehend how expenses and income might influence cash flows in the future. In this regard, machine learning and automation can be helpful.

- Ensuring Up-To-Date and Accurate Data - Individuals can link their forecasting tools with their bank data to make sure that the models created by them have the most accurate and current data.

- Predicting Possible Market Swings - When engaging in scenario planning, one must ensure they are thinking of cash downs as well as ups, issues concerning the industry supply chain, seasonality, and specific events.

- Ensuring Team Effort - Key stakeholders, including the chief executive officer, must provide input regarding cash forecast findings. Moreover, they must collaborate to manage the finances in a way that ensures the fulfillment of long-term and short-term financial requirements.

- Focusing On Working Capital - Another one of the cash forecasting best practices involves putting focus on working capital. Without sufficient working capital, a business will fail to meet the expenses related to daily operations. Hence, cash flow forecasting must involve highlighting the key areas from which it is possible to free up cash for fulfilling such obligations.

Examples

Here are two cash flow forecasting examples: the first is hypothetical, and the second is from a world news article:

Example #1

Suppose Sylvester opens a battery company in January 2024; he has the required capital and manufactures batteries for automobiles. Since he is new in the business, he wanted to make good relationships with the market participants, vendors, and his clients. Hence, he started supplying batteries on a credit sale, meaning the buyer would pay for them in the future. Sylvester decided that he would ask for payments six months after the delivery in July.

In March 2024, Sylvester got several calls from all his small creditors from whom he had taken particular debt. Initially, he got distressed but decided to conduct a cash flow forecasting analysis. Sylvester finds out that he currently has only working capital, and all his significant payments are stuck with clients and will come in July. Sylvester smartly promises all his creditors that he will clear off his debt in August. The creditors agree and give him time.

When Sylvester received his payments in July, he used some of it for business expansion and, from the rest, cleared all his previous debts. It is a straightforward example of cash forecasting, but in the real world, there are multiple factors to be considered. Sylvester could have suffered a loss if any of his clients had postponed their payments.

Example #2

A custom-built ERP module solves the problem of cash flow forecasting. Heidrick and Struggles, a global leadership advisory services company, won the 2024 Golden Alexander Hamilton Award for technology excellence. A treasury group was handling the cash flow forecasting manually and followed a lengthy process using Excel and other set templates. The worst part was downloading, copying, pasting, and reformatting data in more than 500 files every month, increasing the degree of risk and errors.

Recently, they collaborated with Heidrick and Struggles to evaluate the organization's cash flow forecasting needs. The core project team is also associated with other areas such as finance, IT, payroll, controllership, and FP&A. Finally, the project team assessed and presented a variety of options to the treasury group and built a custom module for their ERP system.

Advantages And Disadvantages

The advantages are:

- Businesses can identify and predict cash shortage and surplus or any form of potential crisis that may come around because of it.

- With accurate forecasting, management can execute better business decisions and financial planning.

- Better use of cash inflow and proper monitoring of cash outflows and expenses.

- Stakeholders and board members are confident when this forecasting is efficient, gives them an idea, and makes it answerable to lenders, suppliers, and partners.

- With accurate forecasting, companies know when their cash is going to come, and based on that, they can negotiate in the market and build long-term relationships.

The disadvantages are:

- Although it is based on analysis and proper forecasting, it is still an estimated assumption. Hence, uncertainties always exist.

- No business or corporation can accurately forecast the cash flow; there are certain limitations under which every business operates.

- It is not only calculated on internal aspects but also largely depends on external factors.

- Although with automation and evolving technology, new tools are being developed, maintaining a proper cash flow forecast is a complex, time-consuming, and tiring process.

Direct vs Indirect Cash Flow Forecasting

The distinguishing factors between direct and indirect cash flow forecasting are -

| Direct Cash Flow Forecasting | Indirect Cash Flow Forecasting |

|---|---|

| It is mainly done for a short-term period. | This forecasting is derived for an extended period |

| Reflects the amount of cash required for working capital. | Represents funds required for strategy development, long-term growth, and capital projects. |

| It includes upcoming receipts, invoices, debtors, creditors, and payments. | It is an in-depth analysis of financial statements, balance sheets, net income, balance derivations, and so on. |