Table Of Contents

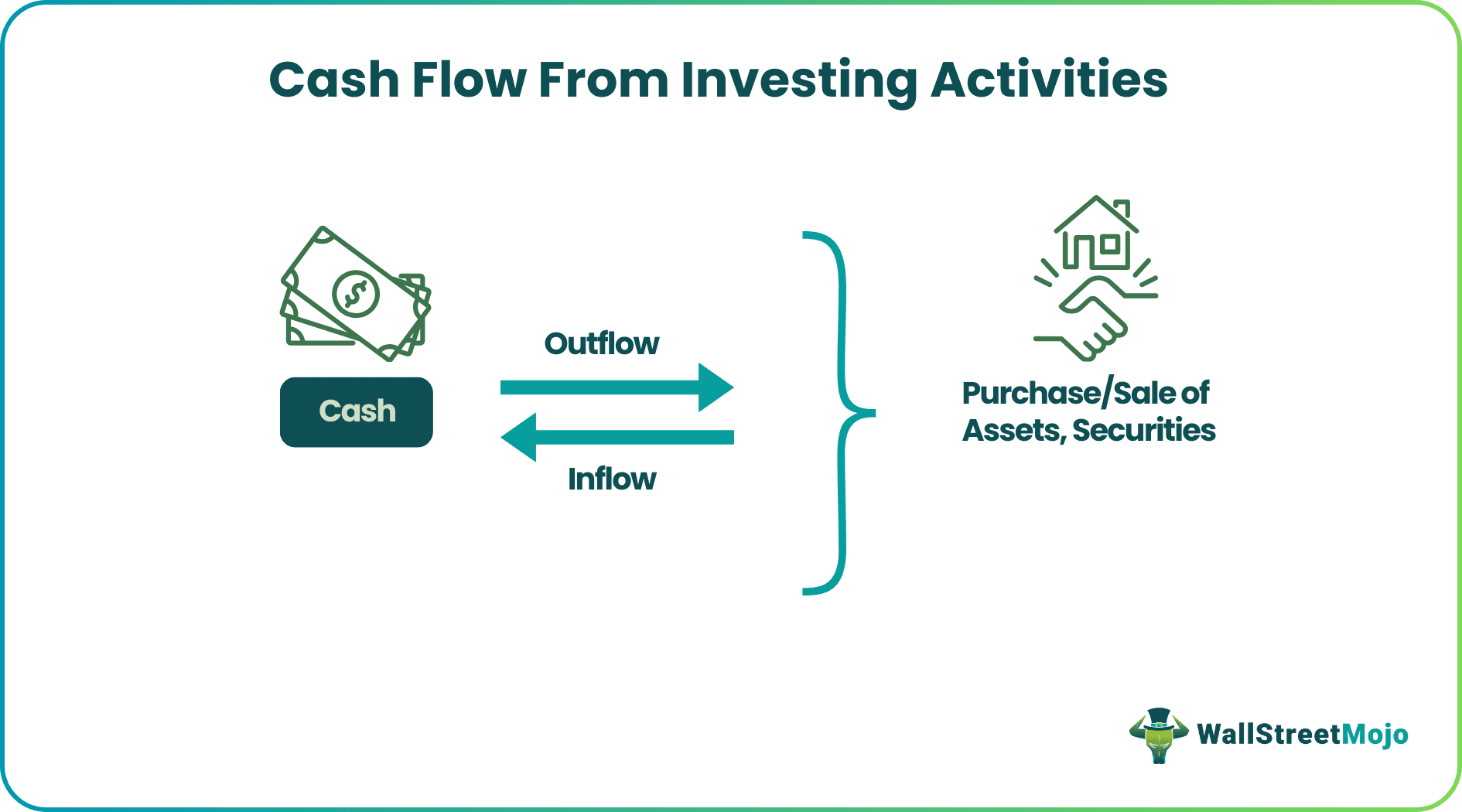

What Is Cash flow From Investing Activities?

Cash flow from investing activities refers to cash inflow and outflow of cash from investing in assets (including intangibles), purchasing of assets like property, plant and equipment, shares, debt, and from sale proceeds of assets or disposal of shares/debt or redemption of investments like a collection from loans advanced or debt issued.

It provides information on cash inflow and outflow related to purchases and sales of assets (Property, Plant & Equipment, etc.), loans made to suppliers or the ones received from the customer, and any payments related to merger & acquisitions. In a nutshell, we can say that cash flow from investing activities reports the purchase and sale of long-term investments, property, plants, and equipment.

Cash Flow From Investing Activities Explained

Cash flow from Investing Activities is the second of the three parts of the cash flow statement that shows the cash inflows and outflows from investing in an accounting year; investing activities includes cash flows from the sale of fixed asset, purchase of a fixed asset, sale and purchase of investment of business in shares or properties, etc.

Investors used to look into the income statement and balance sheet for clues about the company's situation. However, over the years, investors have now also started looking at each of these statements alongside the conjunction of cash flow statements. This helps in getting the whole picture and also helps to take a much more calculated investment decision.

As we will see further in the article elaborated below, when we calculate cash flow from investing activities, this cash flow is a great indicator of the core investing activity of the company. It shows or represents the amount of cash that the business is able to generate form investing its funds into transactions related to fixed assets, securities, real estate, etc. Even change in the cash position due to activities like acquisition, merger etc, will also be considered in this.

Every business always tries to maintain a cash flow level that is positive, which means inflow is more than outflow. This typically means the return is more than the amount invested by the business. However, it is also to be noted that many big and well-established companies also have a negative investing cash flow, mainly because of heavy investments done, whose return will take some time. However, we will study the details further in the article below.

Video Explanation Of Cash Flow From Investing Activities

List Of Items Included

The net cash flow from investing activities includes all the transactions involving acquiring and selling long-term investments, property, plants, and equipment.

These items are found in the non-current portion of the balance sheet.

- Purchase of property, plant, and equipment (cash outflow)

- Sales of property, plant, and equipment (cash inflow)

- Investment in joint ventures and affiliates (cash outflow)

- Payments for business acquired (cash outflow)

- Proceeds from sales of assets (cash inflow)

- Investments in marketable securities (cash outflow)

It is always easier to understand when we create and answer some questions before we calculate cash flow from investing activities. So here are a few questions that, when answered, would help us understand the topic more easily.

1. What happens to the cash account of the company that has purchased land?

2. What happens to the cash account of the company that sold land?

Answer to Question 1: In this case, the cash account would decrease, as the company would need to pay cash for the land purchased. The double-entry accounting system would lead to an increase in asset accounts. In this case, the, asset account under consideration is Property, Plant & Equipment.

Answer to Question 2: In this case, the cash account would increase, as the company would get cash for the land sold. The double-entry accounting system would lead to a decrease in asset accounts. In this case, the asset account under consideration is Property, Plant & Equipment.

How To Calculate?

This part of the cash flow statement is extremely important for every business since it gives the management a proper idea about the cash position of the company related to investment activities. However, it is also important to understand how to calculate it accurately.

- The first step for net cash flow from investing activities is to gather the necessary data for the calculation. The best place to look for such information is the income statement and the balance sheet of the business. It is also necessary to track any financial transaction related to investing from any documents, notes, etc which are commonly maintained by the management. This gives better clarity and prevents any omission of records from calculation.

- The next step is to make a list in detail regarding the various sources and outflow of cash related to investments. The list will be similar to the one given under the previous subhead.

- Then comes the calculation in cash flow from investing activities format, where the total outflow will be deducted from the value of total inflow to get the net cash flow from investment. The resultant figure may be a positive or a negative value, depending on the business activities related to investments.

- Finally, the value calculated in the above step will be transferred to the cash flow statement. However, the cash flow statement will also include the values calculated form operating and financing activities. All three of them combined will reflect the total cash flow statement.

Examples

Let us understand the concept and cash flow from investing activities format with the help of some suitable examples.

Example #1

Let us assume that Mr. X has started a new business and has planned that he will prepare his financial statements like income statement, balance sheet, and cash flow statement at the end of the month.

1st month: There was no revenue in the first month and no such operating expense; hence, the income statement will result in zero net income. In cash flow from investing activities, there was no activity, too. Hence it will remain at zero.

| Cash from Investing activities (for the first month) | |

| Investing Activities | $ - |

2nd Month: The Company made some investments in land and property during the month, amounting to $100000. It is cash outflow and hence negative.

| CFI (at the end of the second month) | |

| Investing Activities | $ - 100000 |

If you are new to accounting, you can learn accounting in 1 hour from this finance for non-finance training.

Example #2

Let’s calculate CFI when we have the balance sheet data.

Also, assume that the gain on the sale of land is $20,000

As we already know that CFI is related to non-current asset portions of the balance sheet. There are two main items in non-current assets – Land and Property, Plant and Equipment.

- Cash inflow from sale of Land = Decrease in Land (BS) + Gain from Sale of Land = $80,000 - $70,000 + $20,000 = $30,000

- Cash outflow from purchase of property plant and equipment (PPE) = $120,000 - $170,000 = -$50,000

- Cash flow from Investments formula = Cash inflow from Sale of Land + Cash outflow from PPE = $30,000 - $50,000 = -$20,000

CFI is an outflow of $20,000

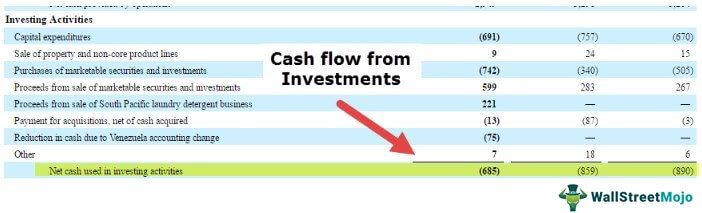

Example #3

Now let us have a look at a few more sophisticated cash flow statements for companies that are listed entities on NYSE.

source: Apple 10K Filings

- Apple’s cash flow from investment activities was an outflow of $45.977 bn.

- Apple is heavily investing in purchasing marketable securities (cash outflow). Apple purchased $142.428 bn worth of marketable securities in 2015!

- In addition, Apple generated cash inflows by selling these marketable securities (cash inflows). Apple sold its marketable securities and generated $90.536 bn as cash inflows.

- In addition, Apple invested in acquiring property, plants, and equipment to the tune of $12.73bn in 2015.

Example #4

source: Amazon SEC filings

Now let us interpret the above CFI and how indicative it is of the company's situation. Some important points on Amazon’s CFI are:

- Amazon has continuously invested in the Purchase of property and equipment, including software and web development. Amazon’s cash outflow for this was $4.590bn and $4.893 bn in 2015 and 2014, respectively.

- It would be best if you were mindful that expenses under this head could indicate where the company is heading.

- The quality of Capex can be determined by reading the management discussion & analysis. This will provide great insights into where the company plans to be in the next few years. Some important points to look at in Capex are (i) quality of Capex, (ii) business proposition of the linked Capex (iii) proportion of the maintenance CAPEX.

- Another important point about Amazon's cash outflows is that they have acquired smaller companies yearly. They made acquisitions worth $795 million in 2015.

- Amazon has been generating cash inflows by selling its marketable securities. Amazon sold $3.025bn dollars of marketable securities in 2015.

Example #5

Below is the CFI from JPMorgan Chase.

source: JPMorgan SEC Filings

Now let us interpret the above statements and how indicative it is of the company's situation. Since this entity is a bank, many line items will be completely different from what it is for others. Many line items are only applicable to banks or companies in financial services. Some important points from JPMorgan's cash flow from investing activities are:

- JPMorgan’s investing activities predominantly include loans originated to be held for investment, the investment securities portfolio, and other short-term interest-earning assets.

- Also, note that the cash flow from investments was $106.98 bn (cash inflow) in 2015, primarily because of the deposits with the bank to the tune of $144.46 bn.

- Other changes in loans resulted in a cash outflow of $108.9 bn in 2015 compared to a much lower number in prior years.

What Analyst Should Know?

Until now, we have seen three companies in three different industries and how cash means different things for them. For a product company, cash is the king. For the service company, it is a way to run a business; for a bank, it is all about cash. These three companies have different things to offer in the cash flow from Investing activities part of the cash flow statement. However, it is imperative to understand the statement should not be singled out and seen. They should always be seen in conjunction with other statements and management discussion & analysis.

Also, you should note that cash flow from investments provides a trend analysis of the companies capital expenditure (which will help us understand if the company is growing or in a steady phase). It is very useful when projecting the financial statements of the company.

Another interesting aspect to look into this CFI is the column of proceeds from the disposal of fixed assets and proceeds from the disposal of a business. If the figures are substantially high, it can help visualize why the company is disposing of assets.

Problems And Solutions

The concept has some positive and negative sides related to the business. Let us study the same in details, as follows:

Problems

- The company may have a negative cash flow related to investments. This may be due to a lot of investment activities undertaken by the business whereas the return will either take a long time to generate or the investments are not very fruitful or viable for the company which may not lead to increase cash flow from investing activities.

- Another problem that can be derived from the previous point is that it may create a negative investor sentiment. Investors, shareholders or analysts, who try to judge the financial condition of the company from its cash flow statement may have a negative idea about it and may try to stay away from it.

- If the management is not experienced enough to understand and identify profitable investment opportunities, they may end up investing in sources which will result in money remaining blocked, leading to cash constraint and underperformance of business.

- Sometimes, all investment related cash transactions may not be clearly reported in the cash flow statement leading to discrepancy and misstatement from the management.

- If the cash transactions are not properly reported, efficient forecasting and budgeting may not be possible, leading to fund mismanagement and loss of opportunity.

Solutions

- The best solution is to properly evaluate the investment option available and then put funds in them. This will not only result in increase cash flow from investing activities later on, but also help the business grow and expand.

- The management should clearly report all investment related transactions in the cash flow statement so that there is clarity and transparency regarding cash inflow and outflow.

- The company should, as far as possible, inform and communicate to the investors and other stakeholders about their various investment plans so that even though the investing cash flow is negative, it will not. result in negative sentiments.

- Any asset remaining in the business that is not generating enough return or is underperforming compared to others, should be disposed to generate cash.

Thus, the above are some problems as well as solutions to deal with cash flow related to investments.