Collateral is a term used to describe an asset or item pledged by the borrower to the lender as security while obtaining a loan. It is a guarantee or assurance of repayment for the lender if the borrower defaults. Let us now discuss the differences between two types of collateral - cash and non-cash collateral.

Table Of Contents

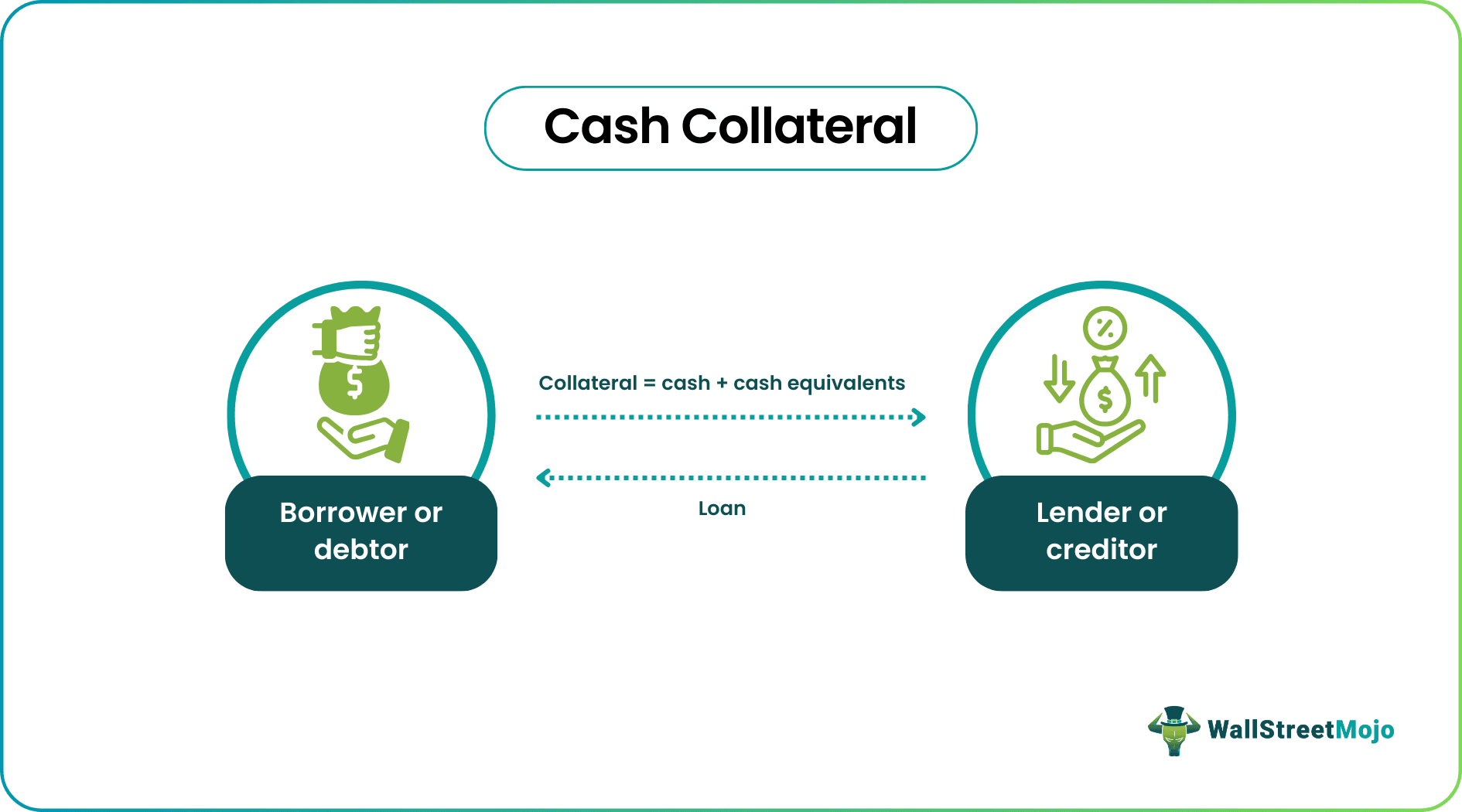

Cash Collateral Meaning

Cash collateral refers to cash or cash equivalents that a debtor grants a creditor as security for a loan or debt. The purpose of cash collateral is to protect the interests of creditors who have extended credit to the debtor company.

In Chapter 11 bankruptcy, the debtor may use cash collateral only with the creditor's consent or court approval. The creditor has the right to take possession of the cash collateral if the debtor defaults on their obligations. This helps to prevent the debtor company from using its cash and other liquid assets without the court's approval, which could harm the creditors' ability to recover their debts.

Key Takeaways

- Cash collateral refers to the security offered by a debtor to the creditor by pledging highly liquid current assets such as cash, deposit accounts, negotiable instruments, securities, and title documents.

- In Chapter 11 Bankruptcy proceedings, the debtor cannot use, lease, or sell the assets kept as cash collateral for any purpose other than business activities without court approval or creditor permission.

- A cash collateral account is opened with a selected bank to hold proceeds from the sale of these assets during bankruptcy.

Cash Collateral Explained

Cash collateral guarantees repayment to the creditors of a business entity, such as suppliers or banks, in case the debtor or borrower goes bankrupt or dissolves the incorporation. To obtain a business loan or credit, a company pledges its inventory, accounts receivable, negotiable instruments, bank balance, and other assets as collateral. However, the debtor can only use, lease, or sell the underlying asset, property, or estate for regular business activities.

Under USC section 363(c), the debtor in possession is restricted from using, selling, or leasing the asset or property for any purpose other than day-to-day business operations. To do so, the debtor must file a motion of use with the bankruptcy court and state the purpose. The cash collateral budget, released by the court as Exhibit 1 with the cash collateral order, outlines the permissible uses of the collateral. The budget can be amended within the boundaries of the collateral order, and parties can file their disagreement within seven days of the amendment. If there is no disagreement, the amended budget becomes applicable.

When a company purchases new equipment or assets for cash, these assets may be considered collateral under Section 361 of the Bankruptcy Code. If the company declares bankruptcy, its current assets, such as inventory, accounts receivable, negotiable instruments, and securities, are sold. The proceeds are transferred to a cash collateral account managed by an administrative agent. The debtor cannot use this fund without the creditor's permission or the bankruptcy court's approval. Additionally, if the value of the collateral depreciates, the debtor must either make regular cash payments to the creditor or provide a replacement lien.

Examples

let's look into some examples for a better understanding of the concept

Example #1

Suppose ABC Enterprises avail a business loan of $50,000 from XYZ bank against its inventory worth $10,000, accounts receivable worth $30,000, and bank balance of $10,000. The debtor (ABC Enterprises) later bought equipment for $7000 and paid through its bank account. Thus, it has to keep this equipment as collateral with the creditor (XYZ bank).

However, after a few months, ABC Enterprises became bankrupt, and therefore a collateral account was opened. The firm sold its equipment and inventory for $15,000 and encashed accounts receivable of $30,000. Thus, $45,000 sales proceeds were deposited in the collateral account.

Example #2

Suppose company A is struggling with its financials and is at default risk on its business loan from bank B. To secure its loan and ensure repayment, bank B demands that company A provides cash security through its inventory and accounts receivable. Company A agrees to these terms and deposits the value of its inventory and accounts receivable into a collateral account managed by bank B.

Unfortunately, company A still goes bankrupt despite these efforts and cannot repay its loan. In this case, bank B would use the funds in the collateral account to recover as much of its loan as possible. However, if the value of the collateral is insufficient to cover the full amount of the loan, bank B may pursue legal action to recover the remaining balance.

Cash Collateral vs Non-Cash Collateral

| Basis | Cash Collateral | Non-Cash Collateral |

|---|---|---|

| 1. Meaning | lt is security pledged against the most liquid current assets of the company. | Non-cash security guarantees the repayment of a loan to the debtor against debt or equity instruments. |

| 2. Underlying Assets | Cash and cash equivalents include deposit accounts, negotiable instruments, securities, title documents, etc. | Debt or equity instruments like government securities, certificates of deposit, letters of credit, corporate bonds, etc. |

| 3. Advantages | Liquidity, better return on loan to the lender, no need for revaluation, no settlement risk, and low operational cost. | There is no reinvestment risk or impact on the balance sheet, and it can be reused and returned to the debtor if the value depreciates on revaluation. |

| 4. Re-Usability | It cannot be reused.

| Banks can reuse it as they transfer the same collateral received as security from a particular transaction for collateralizing another transaction. |

| 5. Lender | Banks, business loan providers, or suppliers of the company. | Banks and other financial institutions. |

| 6. Need for a collateral account | Yes | No |

| 7. Comes into role Play | During Chapter 11 Bankruptcy proceedings. | While extending a secured loan. |

| 8. Lender's fee | Generally, no such fee is charged. | The lender takes a fee from the borrower for using the amortized asset. |

Frequently Asked Questions (FAQs)

1

How to record cash collateral in accounting?

2

What is a cash-collateralized letter of credit?

3