Table Of Contents

What is Cash Budget?

Cash Budget refers to the estimation of cash inflows and outflows made by the management of the business entity over a given period where such estimations are made to evaluate whether the business has adequate cash & cash equivalents to meet its operating needs in the near future.

Accountants frequently refer to the cash budget statement to find the financial health of the organization. It shows a clear picture of the cash flow of the organization and how much funds are readily available to use without affecting the regular happenings of the business. A positive cash budget indicates surplus cash and a negative statement indicates otherwise.

Cash Budget Explained

A cash budget is the written financial plan made by the business related to their cash receipts and payments in a given period. Cash receipts include receipts from the sale of goods & services, interest, etc. and cash payments include payment against the purchase of goods & services, salaries, electricity, loans, etc. In other words, the budget is prepared to make estimations of the company’s cash position in the future.

Generally, it is prepared by the business entities for one year, but when cash flows are not stable, then the companies go for preparing the cash budgets quarterly, monthly, or even weekly so that the business can manage their cash flows as per the requirement.

Purpose

Let us understand the intent behind using a cash budget system in the daily operations of an organization through the discussion below.

- The primary objective of the cash budget is to see the future cash position of the business so that the management can evaluate when the funds are required to be arranged in the future so that the operations of the business will not be hampered.

- It is also prepared to check if the excess cash is available, then they must be invested in a productive way to maximize the business returns.

- Further, they are prepared to predict the cash surplus/deficit during the given period.

- To minimize the expenditures of the business by controlling the spending of the company.

How to Prepare?

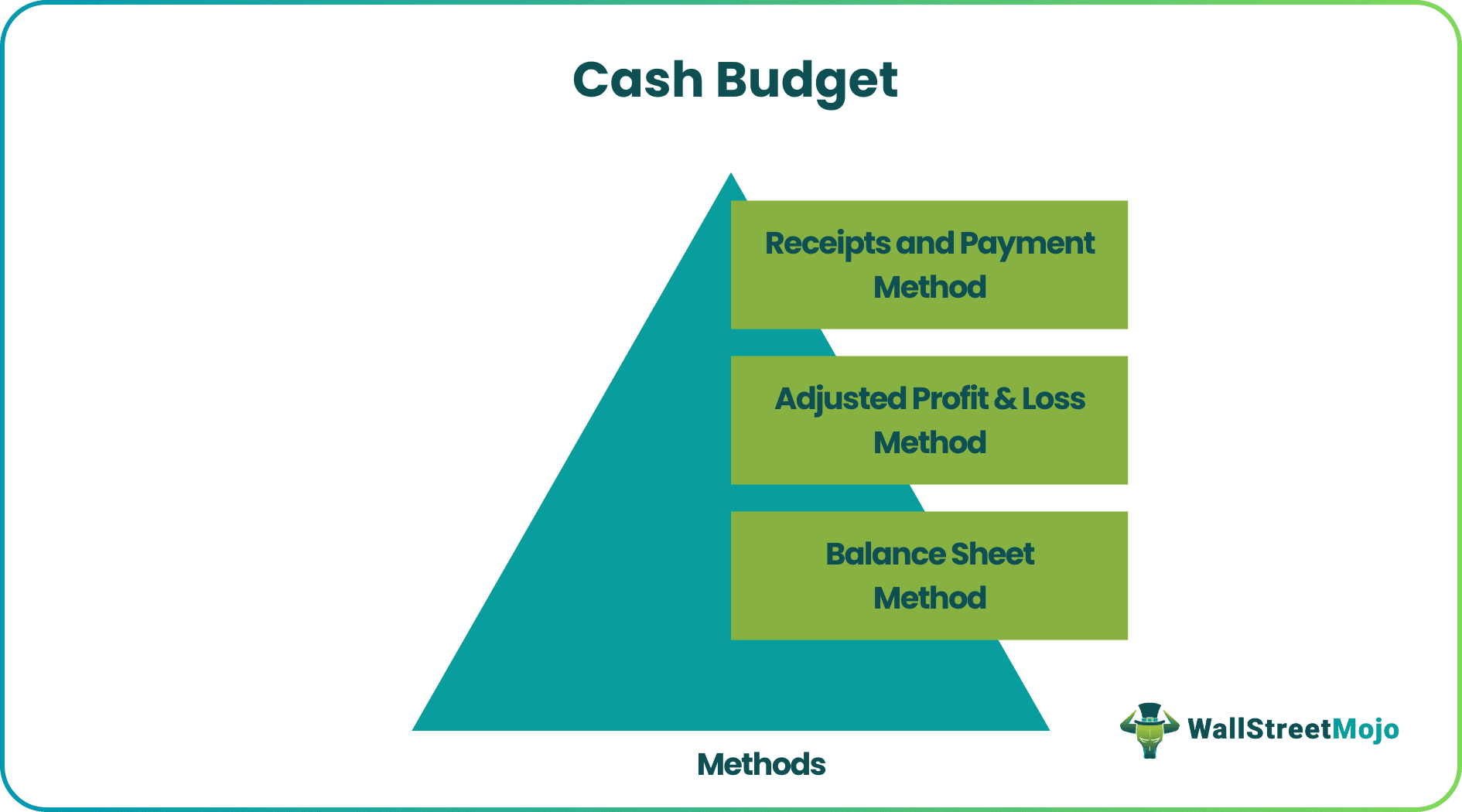

The following methods are used to prepare a cash budget statement:

#1 - Receipts and Payment Method

Receipts and payment method is the most popular and easy method of preparation of the cash budget mostly short-term budget. In the receipts and payment method, all the estimated receipts are added to the opening cash balance. Then all the estimated cash payments are deducted from the sum of opening cash balance, and the estimated receipts and the remaining balance after the above calculations are made represent the closing cash balance.

#2 - Adjusted Profit & Loss Method

This method is followed for the preparation of a long-term cash budget. The basis of preparation under this method is the profit & loss account. The assumption under this method is that all the increase and decrease in cash balance is the profit/loss of the business.

Now while preparing a profit & loss account, various expenses such as depreciation, loss on the sale of assets, goodwill are written off, etc. that do not involve actual cash payments are deducted from the income of the business. Various incomes such as profit on the sale of the fixed asset are added to the income that does not include actual cash receipts are added to calculate the net profit of the business.

So while preparing a cash budget under this method, all the non-cash expenses are added to the net profit, and all the non-cash incomes are subtracted from the same. After that, the working capital changes, capital receipts, and payments, and cash flows related to financing are adjusted, and the opening cash balance is added to the amount after adjustment, and then the result is the cash balance.

#3 - Balance Sheet Method

In the balance sheet method of a cash budget, the expected balance sheet is prepared, which will include expected assets and liabilities except for the balance of cash & cash equivalents. Now if the total of estimated liabilities is more than the estimated assets, then the balancing figure is closing cash and cash equivalents.

But if the result is the opposite, then the closing balance is termed as an overdraft.

Examples

Let us understand the cash budget system better with the help of a couple of examples.

Example #1

Elvis runs a supermarket in New Jersey. His payment schedule is quite hectic as various suppliers deliver various products to suffice the requirements of Elvis’ store. Therefore, upon receiving advice from one of the suppliers, he started implementing a cash budget statement.

In the coming week, the payments were on time as a clearer picture was painted through the statement and plans were made accordingly to ensure timely payments.

Example #2

For business organizations, especially small businesses, it is important to maintain cash budgets as it gives the owners and employees a sense of what they are collectively working towards.

Small businesses are most vulnerable to inflation and its effects. Budgeting helps them tackle inflation and other business risks with more efficiency.

However, when the business grows out of the nascent stages, it might be difficult to maintain the cash budget by the owners as they might want to concentrate on the developmental aspects of the business. Therefore, it is advised to train employees to create, maintain, and review budgets.

Format

A format to understand what we have understood so far shall help us understand the concept in better detail. Let us take a look at a cash budget statement format as given below.

Importance

Adopting a cash budget system provides ample insight into the financial well-being of the organization. A few other factors that make these budgets an important facet of businesses are discussed below.

- They help the management to know/estimate the cash position of the business well in advance relating to the different financial periods.

- The cash budget indicates the requirements of cash for capital investments.

- It helps the owners to know the surplus cash that will be available for the short term or long term investments.

- The future cash availability of the business can be known for availing discounts from the vendors on timely payment of cash.

- Planning of redemption of shares/debentures becomes easy with the estimation of cash position as the cash availability is known well in advance.

- It is also essential to maintain the liquidity of the business. It suggests the minimum level of cash that a business should maintain to meet the expected requirements and contingencies.