Table Of Contents

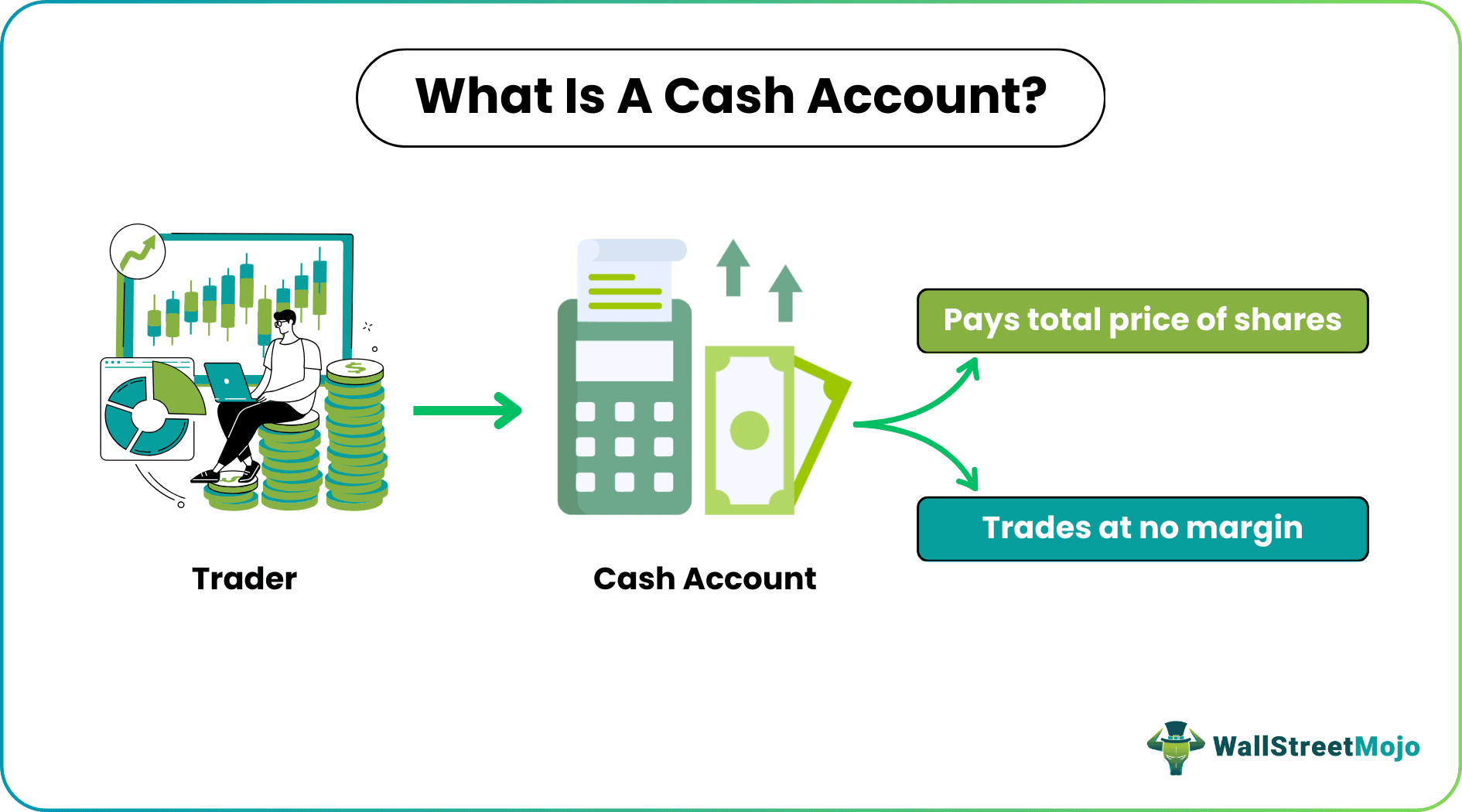

What Is A Cash Account?

A cash account is a brokerage account in which the investor is required to pay the whole purchase price for any securities they wish to acquire. It is against the rules for an investor who uses a cash account to borrow money from his or her financial adviser to cover the costs of transactions made utilizing the account.

Alternatively, it can also refer to a cash account, a type of ledger in accounting to record all cash transactions. In bookkeeping, it is also sometimes referred to as a cash book. The cash receipts diary and the cash payment journal are incorporated into the cash account.

Key Takeaways

- A cash account is one kind of brokerage account that is used for trading.

- It requires that all transactions be payable in full with accessible cash on the date that the settlement takes place.

- When purchasing stocks using a cash account, the investor must either make a cash deposit sufficient to cover the purchase cost or sell other securities on the same trading day to generate enough cash to settle the buy order.

- In contrast to margin accounts, cash accounts do not grant permission to engage in margin trading or short selling.

Cash Account Explained

A cash account implies any securities and their transactions conducted with a brokerage company are required to be paid for in full from funds present in the account when the settlement occurs. Because of this, both short selling and purchasing on margin are not permitted in this kind of account. In addition, such accounts and the purchase of stocks using margin are governed by Regulation T, which the Federal Reserve issues. This legislation gives investors two full business days to make securities payments. It is sometimes referred to as T+2.

Regarding bookkeeping, a cash account is sometimes referred to as a cash book. The cash receipts diary and the cash payment journal are incorporated into the cash account.

One may use a cash or brokerage account to handle the funds users intend to utilize to buy stocks. A cash account is a brokerage account that allows one to acquire stocks by depositing dollars. The trader pays the complete investment cost using the money in this account. Because cash brokerage accounts do not permit short sells and do not allow traders to buy on leverage, investing in cash brokerage accounts is one of the most conservative investment options available.

Investors seeking a comprehensive platform may consider Saxo Bank International for a variety of account types and investment options.

Types

The following is a list of the various kinds of cash accounts:

#1 - Payroll Checking Account

Establishing a separate checking account to pay employees is common practice in businesses of all sizes, including some of the smallest ones. They tally up all of the checks and transfers used to pay the personnel, and then they take that money out of the operating fund and put it toward covering the payroll checks.

#2 - Business Checking Account

In most cases, a company would establish a particular checking, referred to as the operational account, to manage business activities such as the deposits of income and bills.

#3 - Commercial Account

If a company takes credit cards as payment, it almost always operates under its dedicated merchant account. It simply deposits funds from the merchant provider or the company, which enables the company to integrate credit card processing. However, it is common practice to withdraw from this account to meet the costs of making payments toward bills.

#4 - Account For Miscellaneous Cash

The majority of commercial enterprises are equipped with a cash box into which daily payments for expenses can be deposited. This account has a balance that is consistently the same. This name comes from the fact that anytime the cash box is opened, it should include cash or receipts, bringing the total up to the amount of the petty cash fund.

Opening a Hargreaves Lansdown Fund and Share Account provides a straightforward way to buy and manage shares online.

Examples

Let us look at the following examples to understand the concept better.

Example #1

An article by Mondaq highlights eligibility requirements for opening cash accounts for alternative investment funds based in Luxembourg. This article clarifies the categories of companies qualified to create and maintain such accounts for alternative investment funds (AIFs). It has been established that the only entities that can qualify as eligible for keeping such accounts are central banks, credit institutions authorized by the EU, and banks authorized by foreign countries. Each of these is referred to as an "Eligible Entity."

It further suggests that establishing a new sub-fund within an existing AIF is not permitted if an EMI holds the accounts of the existing AIF.

Example #2

Consider that ABC is a firm that specializes in furniture. On January 10, it sold 20 sofas to Wholesaler XYZ, and it earned $15,000 from the deal. However, the transaction is not documented as taking place until January 10. The fact that the computers were ordered by the wholesaler Company XYZ on December 5 is irrelevant, given that the company did not pay for them until January. Also, the day they were delivered.

On the other hand, under accrual accounting, the transaction for $15,000 would have been recorded by Company XYZ on December 5, even though no cash was exchanged at that time. Similarly, businesses that employ such accounting record their expenses when they pay for them rather than when they experience the costs.

Many traders use Saxo Bank International to research and invest in stocks across different markets. Its features like SAXO Stocks offer access to a wide range of global equities for investors.

Difference Between Cash Book And Cash Account

- A cash account is an account that is contained inside a general ledger, whereas a cash book is a distinct ledger that is used only to record cash transactions.

- A cash account is organized in the style of a ledger. A cash book combines the functions of a diary and a ledger.

- Money in the bank does not include any narration in the work. However, there are narrations in the cash book.

- A journal daybook is necessary for the cash account. The cash book is not connected to any of the other books.

Cash Account vs Margin Account

- The cash account lets one use the money already in their account. A margin account allows traders to borrow money to finance investments.

- Trading via margin accounts allows a trader to increase their profits on investments. However, because trading in a cash account is restricted to the funds already in the account, returns cannot be multiplied.

- When using a margin account, there is a possibility of losing more money than initially invested. However, in the cash account, this is not the case.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

A debit is an accounting item that either increases an asset or expense account or decreases a debt or equity account. A credit is a financial statement entry that increases an equity or liabilities account. It is located to the left when included in an accounting entry.

Because currency can be physically handled, it is considered to be a component of a real account. Therefore, to follow the golden laws of accounting, one must credit what is paid out and debit everything that is paid for or lost.

By restricting possible losses to the total amount invested, a cash account protects investors from experiencing losses disproportionately large to the amount they initially committed.